Laser Marketplace 2014: Lasers forge 21st century innovations

The Laser Focus World annual review and forecast of the laser marketplace is conducted in conjunction with Strategies Unlimited (Mountain View, CA; a PennWell company), with additional input from Industrial Laser Solutions magazine.

Austerity; sequester; sovereign debt crisis; downsize; rightsize: the lexicon for an uncertain economic future that is becoming 'the new normal'. Shortly after the U.S. Congress ended a short government shutdown in October 2013, CBS News anchor Bob Schieffer summed up the situation—and the global economy for that matter—saying, "I suppose we should all feel relieved, like you would feel if you've been shot at and missed." In short, we survived the 2008/2009 Great Recession, but the tumult left many of us shell-shocked.

The reality is that gross domestic product (GDP) growth rates in the major economies are sluggish and developing country GDPs continue to retreat from record double-digit highs. And yet, the majority of laser manufacturers are optimistic. The "global headwinds" outflow from the recession is now calming: manufacturing has recovered, the thirst for communications bandwidth continues, and momentum keeps building for laser-based medical devices and instrumentation—even amid falling R&D and military budgets.

"We're all tired of focusing on the economy and ready to start capitalizing on the future capabilities afforded by laser technology," says Kiyomi Monro, CEO at Biophotonic Solutions (East Lansing, MI). "I believe that photons are the new 'fuel' of the 21st century. Just as steam fueled the cotton gin and the industrial revolution, and petroleum fueled Ford's Model T and the jet engine in the last century, photons are driving new efficiencies in materials processing, delivering astounding medical and materials science breakthroughs, being harvested to provide electrical energy, and lighting a communications infrastructure that is already leading to a transformative virtualization of our society."

While Monro's prediction that by 2050 the largest corporations on earth will be photonics companies is bold considering the size of our industry today, Monro's enthusiasm about the enabling power of photonics technology is shared by a pioneer in our industry. "IPG Photonics will produce a combined 20 megawatts of laser diode power this year-the equivalent of a small coal-fired power plant," says IPG Photonics (Oxford, MA) CEO Valentin Gapontsev. "Just as the automobile improved our lives and became necessary, and just as the microprocessor is the heart of the computing world, fiber lasers are becoming the workhorse of modern manufacturing."

The tremendous success of IPG and its fiber laser portfolio is one example of how a new laser technology became rooted in industrial applications. IPG will ship 40% more kilowatt-scale lasers in 2013 than it did in 2012, with record 3Q13 revenue of $172.2 million—a 10% increase for the period ended September 30, 2013 compared to the same period last year—thanks to a 19% increase in sales for materials processing applications. While fiber lasers may have displaced carbon-dioxide (CO2) lasers in many applications, the better reality is that fiber lasers have also displaced mechanical means of cutting, welding, and surface texturing.

You might think that IPG's success as a vertically integrated powerhouse in the laser world would invoke a level of disdain to competing manufacturers; but on the contrary, both fiber laser and direct-diode laser manufacturers we spoke to this year could only compliment IPG and be grateful for the path it has cleared in terms of convincing the manufacturing community that fiber lasers are a reliable, low-cost, efficient alternative to incumbent mechanical materials processing methods.

"We are grateful to IPG for its success and are even grateful for the telecommunications bubble, without which companies like IPG may have never had the means—or motivation after the bubble collapsed—to invest so heavily in a new fiber laser technology that targeted non-telecom applications," says Jian Liu, founder and CTO of PolarOnyx (San Jose, CA). "Beginning in 2008/2009, the question marks surrounding ultrafast femtosecond fiber lasers went away; already less expensive than DPSS equivalents, femtosecond lasers with energy levels to 100 μJ at 1 and 1.55 μm wavelengths are now being used in industrial applications, routinely for LASIK, and are just now out-performing Ho:YAG and other lasers for micro- and nanosurgical applications due to their bright single-mode spot and amenability to endoscopic fiber delivery."

"Carl Zeiss Meditec, Alcon Laboratories, OptiMedica, and Lutronic are just some of the companies adopting femtosecond fiber lasers for surgery, and PolarOnyx is in the game developing a 'smart surgery' tool that will image, identify using LIBS [laser-induced breakdown spectroscopy] technology, and apply the appropriate surgical energy for cutting, drilling, or ablating the hard or soft tissue—or metal implant—encountered." As Liu concluded in a recent article on his company's work, "The future of ultrafast fiber lasers is beyond our imagination and without boundary."

Last year, Laser Focus World reiterated how the laser has progressed from scientific novelty to industrial 'tool' and believes that it's time to start thinking about new application areas that could catapult some laser segments into double-digit growth territory and potentially improve upon the historic (ignoring recessions) 5–6% annual compound average growth rate (CAGR) 'slow and steady' laser market.

In 2013, worldwide laser sales reached $8.806 billion dollars, representing 1.7% growth over a revised (upward) 2012 laser market value of $8.657 billion and below the 3.5% growth that we forecast in last year's laser market review primarily due to increased weakness in the optical storage sector, but also due to our forecast weakness in lithography, R&D, and military laser sales. If these four segments are removed from the 2013 tabulation, the worldwide laser markets actually grew 7.5%.

For 2014, we forecast worldwide laser sales to increase 6.0% from 2013's figure to $9.334 billion dollars. The 2014 forecast and the forecasted market numbers to 2017 included in the Strategies Unlimited quantitative laser market report should please laser manufacturers playing in some emerging sectors.

Manufacturing innovation

"We have demonstrated that our MEMS [microelectromechanical systems]-based adaptive optics [AO] can expand the toolset for materials processing by providing on-the-fly beam shaping," says Michael Helmbrecht, president & CEO of Iris AO (Berkeley, CA). "With the ability to handle 2–3 kW/cm2 power levels, our AO systems can improve beam uniformity and improve M squared." Helmbrecht adds that programmable AO systems could allow laser manufacturers to use one fiber-optic cable or optical head to deliver countless variations of spatial beam profiles through a simple software-controlled MEMS adjustment.

Such optical innovations make it easier for a single industrial laser system to process a variety of materials—an especially important feature considering the evolution of materials development in the manufacturing sector. For example, last year we talked about the movement towards aluminum and high-strength steel (HSS) materials for automotive and aircraft assemblies; this year, a new material enters the scene: carbon fiber-reinforced plastic (CFRP).

Weighing 50% less than steel and 30% less than aluminum but with comparable (or better) strength, CFRP components are unfortunately more expensive than their alternatives. However, research groups like Fraunhofer are working to reduce CFRP costs to make them economical for mass production, with Fraunhofer citing a McKinsey Global Institute (www.mckinsey.com) study that forecasts demand for CFRP to rise 20% per year through 2030.

"It turns out that direct-diode, fiber-coupled laser systems around 3 kW fitted with our homogenizing optics work extremely well for CFRP production tasks like laser-assisted tape laying," says Wolfgang Todt, VP of U.S. operations for Laserline (Santa Clara, CA). "Laser 'brightness' is being hyped in the direct-diode laser community; the reality is that not all applications—with the exception of metal cutting—require a small m2 value. The desired power-per-area parameter can be manipulated in any materials-processing laser through custom beam-delivery optics, whether it's direct-diode, fiber, or DPSS-based," he asserts. "With our installed base of 3000 direct-diode materials processing laser systems, we've learned that the real feat is to supply a laser system that best meets the customers' need at a price point prohibitive to other laser or mechanical methods."

The emergence of alternative materials and industrial processes uniquely suited to laser machining should protect the laser industry even if the "recession" monster awakens. Whether processing aluminum, HSS, and now CFRP, or for aerospace component hole drilling and even fuel-injector hole drilling, or for processing ultrathin glasses for cell phones and tablets, lasers should enjoy brisk sales since comparable machining substitutes are nowhere in sight.

Incidentally, GT Advanced Technologies (Merrimack, NH) signed a multi-year agreement with Apple in November 2012 for sapphire material—stronger and harder than Gorilla Glass. The facility in Mesa, AZ will employ 700 people in its first year, and there is a good chance that lasers will be used for sapphire glass finishing operations.

"Lasers do not exhibit the same mechanical wear as drills and knives, resulting in higher yields and more predictable processes," said Magnus Bengtsson, director of strategic marketing at Coherent (Santa Clara, CA) in his 2013 Stanford Photonics Research Center (SPRC) Symposium presentation entitled "Lasers in Smart Phone Manufacturing—enabling the mobile revolution." Bengtsson explained how ultrathin glasses, organic films, and certain semiconductor materials, for example, can only be adequately processed using lasers, bringing the 'lasers as enablers' message full circle.

Coherent benefited from its broad portfolio of materials-processing lasers as evidenced by its 2013 revenue growth. For its fiscal year period ended September 28, 2013, Coherent saw sales of $810.1 million compared to $769.1 million for the full-year period ended September 29, 2012. In the Coherent Q4 financial press release, Coherent CEO John Ambroseo said, "And while materials processing bookings were seasonally lower, we ended the fiscal year with a new materials processing bookings record."

The phenomenon of emerging 'laser-only' or 'laser-enabled' manufacturing applications is perhaps best exemplified by 3D printing; however, it is important to remove the mainstream hype from the technological reality.

Much of the hype surrounds the availability of $1000 to $3000 heat-based, nozzle-extruded-plastic 3D printers for the student and small-business enterprise with 0.1 mm layer resolution that have nothing to do with lasers. The technological reality is that professional, sophisticated, and significantly more expensive 3D printers with micron and even better resolution that incorporate LEDs or lasers for laser additive manufacturing (LAM), laser melt deposition, or vat photopolymerization processes using metals and specialized polymers or ceramic materials may never apply to the average consumer and parts production costs must reduce dramatically before widespread commercial deployment of these systems can occur.

"The higher quality of laser sintering processes over other additive manufacturing methods is driving aggressive growth worldwide in our industry," says Andy Snow, regional director at EOS of North America (Novi, MI). "EOS' plastic laser-sintering systems feature 50 W CO2 lasers and our direct metal laser-sintering [DMLS] systems have a single, 200 W ytterbium-fiber laser with an option of 400 W for faster processing, with upcoming DMLS systems offering a multi-field, four-laser approach for the faster production times required by our growing customer base."

Any hype surrounding even non-laser 3D printers can only benefit laser manufacturers in the long run as the process gains broader acceptance and media exposure. Particularly in the U.S., which dominates 3D printer system sales that saw a worldwide 28.6% CAGR in 2012 and were valued at $2.2 billion according to a 2013 report from Wohlers Associates (Fort Collins, CO), 3D printing is viewed as somewhat of a savior to a country that has been outsourcing manufacturing for decades; in fact, the National Additive Manufacturing Innovation Institute (NAMII; http://namii.org/america-makes) changed its name in October 2013 to "America Makes".

Ubiquitous sensing and smart gadgets

In 2013, II-VI Incorporated (Saxonburg, PA)—with its HIGHYAG, VLOC, Aegis Lightwave, Marlow Industries, M Cubed, Photop, and AOFR business segments, among others—continued its acquisition spree (it had acquired LightWorks Optical Systems in late 2012) by acquiring the laser diode, micro-optic, and amplifier divisions of Oclaro (San Jose, CA). "Oclaro's sale of its gallium arsenide [GaAs] laser diode business will allow them to focus on their core telecommunications markets, while II-VI aims to leverage its GaAs-based high-power edge-emitter diode and high-speed VCSEL expertise to target growth in industrial, medical, and high-volume consumer markets," says Karlheinz Gulden, product management senior director at II-VI.

"We are excited about emerging applications in AOCs [active optical cables] for consumer devices and in gesture recognition," adds Gulden. "Apple led the charge in high-accuracy touchscreen technology, Google focused on high-quality voice recognition input, and Microsoft led on high-end gesture recognition with its advanced Xbox Kinect. These capabilities will be broadly adopted across the market, all coalescing in next-generation smart devices that will require both edge-emitters and VCSEL sources; today, the II-VI infrastructure positions us well for the high-volume ramps demanded by consumer applications—the nearest supplier is at only 10% of our existing production levels."

Adding camera-based imaging to the mix, Gulden envisions a world where our home electronics will react without touch, security doors will open automatically with badges being unnecessary, retail outlets will monitor where customers congregate and what products they favor, and touchless sensing will even improve clinical and food-handling hygiene. This move towards ever-present sensing applications and the incorporation of smart gadgets in the consumer realm will not only save time, effort, and energy, but will also improve public safety and health—especially in developing countries often without access to expensive, laboratory instruments. In short, handheld laser-based sensing devices bring technology to the masses.

"Everybody needs a flow cytometer; they just don't know it yet," says Peter Kiesel, principal scientist at Palo Alto Research Center (PARC, a Xerox company; Palo Alto, CA). "High-end flow cytometers in clinical settings continue to dominate the market and typically use DPSS or diode lasers. However, emerging technologies, like PARC's spatial modulation technology, can use either laser diodes or LEDs that enable low-cost, handheld instruments. Prototype instruments have been demonstrated that are applicable for traditional medical diagnostics, agricultural quality control such as milk processing, and monitoring water quality." Kiesel adds, "In four to five years, handheld or cell-phone-based cytometry will revolutionize point-of-care diagnostics with application-specific disposable test cartridges for real-time analysis."

In late 2012, Thorlabs (Newton, NJ) acquired CompuCyte (Cambridge, MA) and its laser-scanning cytometry portfolio, anticipating the promising future for flow cytometry instrumentation. Some manufacturers we spoke with estimate that flow cytometry could represent a $250 million industry for lasers within the next few years. If we assume that lasers comprise 5% of the nearly $3.5 billion global flow cytometry market forecast by BCC Research (Wellesley, MA) for 2013, those manufacturer estimates could be fairly accurate.

The molecular age?

Supporting the notion that photons will fuel the 21st century, some laser manufacturers that sell sources and components for the proliferating petawatt laser industry or into molecular imaging and spectroscopy applications see our current century in a complementary light. "It is a golden era for atomic and molecular photonics, wherein lasers are being used to deeply probe molecules and atoms—finally unlocking many of the mysteries that have confounded the materials and life science industries for decades," says Graeme Malcolm, CEO of M Squared Lasers (Glasgow, Scotland).

"The academic groups and scientists we sell to are redefining absolute zero, proving quantum simulation, exploring quantum cryptography techniques, helping infrared, mid-IR, and terahertz sensing, spectroscopy, and hyperspectral imaging technologies multiply, and even proving that teleportation is possible," adds Malcolm. "Our business has been doubling year-over-year for the past five years, and we are bullish that these scientific applications can sustain a number of laser and photonics companies and spawn $100-million-dollar businesses in many application areas."

Biophotonics

The biophotonics industry represents perhaps the largest growth opportunity for laser manufacturers as our population ages. Any product with the possibility of entering the consumer realm, going clinical, or finding widespread use in a field setting has the potential to boost laser sales volumes well beyond the levels recently enjoyed in the R&D health sector.

"Laser aesthetics is booming for the same reason that everyone wants to drive a BMW—we all want to look good and feel good about ourselves. Like BMW or Mercedes, we build products that are aspirational like our Forever Young BBL that has seen tremendous success this year," says Rick Mendez, senior director of global marketing at Sciton (Palo Alto, CA). "Aesthetic laser systems are also opening up new revenue streams for non-cosmetic doctors worldwide, especially as salaries and reimbursements continue to drop and they look for new sources of revenue to make up the difference."

Mendez points out that laser procedures are becoming affordable for the masses, and that some of his most successful customers are doctors in 1000-person-population towns. "Cosmetic Botox alone is a $500+ million dollar [annual] industry; if doctors can convince people to inject botulinum toxin into their faces, noninvasive efficacious laser treatments are a slam dunk," adds Mendez. "The keyword here is efficacious: Our company was founded in 1997 by our president Dan Negus and CEO Jim Hobart; Hobart also founded Coherent. More than 95% of our systems are still in use today—Sciton knows a thing or two about lasers and how they interact with human tissue."

Beyond aesthetics, in-the-field biomedical instrumentation for both clinical and consumer markets enabled by small DPSS and diode lasers (and even LEDs) is also hot: handheld 1064 nm Raman spectrometers from companies like Rigaku (Tokyo, Japan), B&W Tek (Newark, DE), StellarNet (Tampa, FL), BaySpec (San Jose, CA), and Ocean Optics (Orlando, FL) detect chemicals and explosive residues; compact breath analysis instrumentation analyzes molecules in human breath that serve as disease markers; and more than 300 teams are registered to compete for the $10 million Qualcomm Tricorder XPRIZE that seeks the Star Trek equivalent of a handheld medical diagnostic device.

Cinema and lighting

"The laser digital cinema industry is finally getting ready to launch in 2014," says Greg Niven, VP sales & marketing at Necsel (Milpitas, CA). "With 40,000 theatre screens in the U.S. and an estimated 120,000 worldwide, a $20K to $60K laser projection engine comprised of 200 W to 600 W RGB laser modules to make up to a 70,000 lumen projector—more than twice as bright as the 30,000 lumen limitation of today's Xenon projection lamps—translates to a potential billion dollar laser market assuming even 50% penetration."

Born of Novalux extended-cavity surface-emitting laser (NECSEL) technology, Necsel is fortunate in that its parent company Ushio (Tokyo, Japan) also wholly owns Christie Digital Systems (Kitchener, ON, Canada and Cypress, CA), which is estimated to control 40% of the digital cinema market with Barco (Kortrijk, Belgium), Sony, and NEC (both in Tokyo, Japan) capturing the remaining majority. "The laser projection ROI story is compelling, considering that lasers last 10 years compared to 3–6 months for Xenon lamps and consume 50% less energy. This is especially applicable for the larger screens where operating costs for the projectors can exceed $15,000 dollars per year," Niven adds.

While penetration rates for laser projectors are hotly debated and entry pricing is high, Niven believes that high brightness is critical in satisfying viewers that consistently complain that movies—and 3D movies in particular—are too dim. And although 3D movies may never enjoy a year like 2010 when just four 3D movies captured $1.2 billion or 33% of the total dollars earned in the U.S. by 127 films released up to April 2010, the younger generation—50% of whom aged 12–24 saw a 3D movie in 2012 compared to only 13% of 60+ year-olds—is expected to continue their 3D viewing habits.

Beyond laser cinema projection, Niven expects that multiwatt-level laser diode lighting (which is amenable to fiber-optic coupling to remove the heat source from sensitive areas and has significant brightness, reliability, and colorimetry advantages over legacy and even LED lighting) will play a bigger role in lighting for outdoor neon border tubing, hazardous locations like oil and gas refineries, and anywhere it is expensive to replace lamps such as for radio- and cell-tower signal lights.

Rise of the semiconductor laser diode

Just as fiber lasers continue to displace CO2 gas lasers and diode-pumped solid-state (DPSS) lasers displace argon-ion lasers at 488 and 515 nm, the visible spectrum formerly commanded by DPSS laser technology is now being squeezed by semiconductor laser diodes that continue to advance in terms of brightness and power output.

"For moderate-power life science instrumentation, DPSS technology only commands a narrow 550–600 nm window in the 400–750 nm visible range; today, you can readily source single-mode 405 nm Nichia laser diodes with 250 mW output or 150 mW single-mode red laser diodes at 635 nm," says Phil Crowley, CEO of Market Tech (Scotts Valley, CA). "These incremental changes will have a profound impact on laser-based instrumentation going forward, enabling systems to become smaller, lighter, and more energy efficient—further enabling new applications never before thought possible using large and complex gas or DPSS laser light engines," adds Crowley. "These incremental changes in laser technology trends are sometimes overlooked when you're looking for the next big laser innovation."

"From my perspective, the next decade will be a banner one for the laser industry," says Tom Baer, executive director of the Stanford Photonics Research Center at Stanford University (Stanford, CA). "The mainstream attention given the laser during its 50th anniversary in 2010, as well as the momentum behind the activities of the National Photonics Initiative [NPI] and Europe's ongoing Photonics21 activities, will undoubtedly lead to increased funding that should translate into healthy market growth for laser manufacturers." Baer adds, "It is quite ironic, given the laser's history and reputation of being power hungry and inefficient, that using lasers in next-generation datacenters is in large part being driven by tremendous pressure to improve datacenter energy efficiency. Diode lasers are now a model of efficiency, and solar-powered lasers are a prime example of the ultimate renewable energy resource; in this case, photons put to very good use."

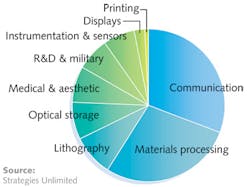

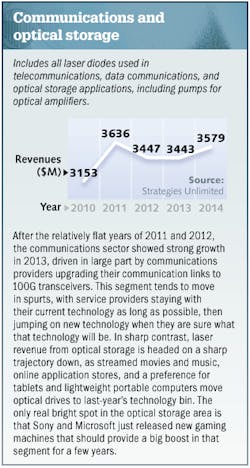

Despite the significant decline in optical storage laser sales, the communications and optical storage segment continues to be the largest in the laser industry, followed by materials processing and lithography lasers. But in 2013, sales of medical and aesthetic lasers exceeded laser sales in the scientific research and military, as well as the instrumentation and sensors category.

Communications and optical storage

Flash drives, streaming video, and the Cloud have taken their toll on laser sales for optical storage devices such as CDs, DVDs, and even Blu-ray; in fact, IHS iSuppli (El Segundo, CA) says that even NAND flash demand is decelerating from the 16% rise in 4Q12 to only 5% growth in 4Q13 due to an increase in Cloud-based services.

Stand-alone Blu-ray player sales and optical storage for games like Xbox and Playstation will peak in 2014; however, sales of desktop PCs and laptops with optical storage continue to decline. All-in-all, optical storage laser sales will see a swift decline from $967 million in 2012 to a forecasted $566 million in 2014.

Quite the opposite scenario holds for lasers used in communications; overall sales have risen from $2.481 billion dollars in 2012 to $2.734 billion in 2013, and are forecast to increase 10.2% to $3.013 billion dollars in 2014.

"Communications component suppliers like Finisar develop sophisticated technology on demanding schedules and sell devices into a fiercely competitive marketplace that keeps margins low," says Chris Cole, director of transceiver engineering at Finisar (Sunnyvale, CA). "This in turn enables customers like Google to achieve low cost when building out their datacenters. The bright spot is the high-end side of the market where products requiring photonic integration—like 100 Gbps optics for datacenter and transmission applications—are growing at a rapid pace while the rest of the fiber-optic industry is mostly flat."

Indeed, Infonetics Research (Boston, MA) forecast that 100G optical transceiver shipments would double in 2013 and again in 2014. "With port count doubling each year, we see 100G technology playing in the marketplace for another 10 years," says Ferris Lipscomb, VP of marketing at NeoPhotonics (San Jose, CA). "Coherent transmission allows you to leverage older fiber installations through digital signal processing; our customers see a practical path to terabit transmission, and we are building the components to get them there."

NeoPhotonics' 3Q13 revenue for the period ended September 30, 2013 reached a record $76.8 million, up 2.4% from the prior quarter and up 16.1% from 3Q12. And for the period ended October 27, 2013, Finisar announced record revenues of $290.7 million (the fifth consecutive quarter of revenue growth) or 9.3% over the prior quarter and even with a decent operating margin of 10.4%. Also benefiting from the 100G photonic integrated circuit (PIC) rush is Infinera (Sunnyvale, CA), whose 3Q13 GAAP revenues were $142.0 million compared to $112.2 million for the same quarter of 2012.

The momentum and longevity behind 100G implementation was reinforced by a statement from John Croteau, president and CEO of MACOM (Lowell, MA), as he commented on MACOM's announced plan to acquire Mindspeed Technologies (Newport Beach, CA): "This will position MACOM as a clear leader across all 100G segments, all physical layer products, and all requisite technologies enabling us to capitalize on the expected decade-long build out of the 100G optical market."

The communications industry is not only getting a boost from 100G demand, but bandwidth-hungry applications like streaming video and in-home high-definition TV viewing are also driving an active optical cable (AOC) boom. "There is a $100 billion dollar copper electrical interconnects market that will need to go optical, especially as TV resolution migrates from HDTV to 4K and 8K; the interfaces must drastically accelerate in speed," says Nikolay Ledentsov, CEO of VI Systems (Berlin, Germany).

"While the Thunderbolt interconnect standard started out in copper at 10 Gbps per channel [10G], Thunderbolt 2 brings the speed to 20G; no doubt good news for laser diode manufacturers as a 20G copper interconnect is heavier, costlier, and more power-hungry than an optical equivalent," adds Ledentsov. "In fact, Corning just launched a Thunderbolt and Thunderbolt 2-compatible optical interconnect to capitalize on this sizeable consumer communications market where photonics and lasers can play a dominant role and constitute a significant share of the interconnect price."

Despite falling data storage laser sales, strength in the communications sector led by 100G deployments—revenues for which exceeded 40G for the first time in 2Q13, according to Ovum (London, England)—will result in overall communications & optical storage growth of about 4% from 2013 sales of $3.443 billion to a forecasted $3.579 billion in 2014.

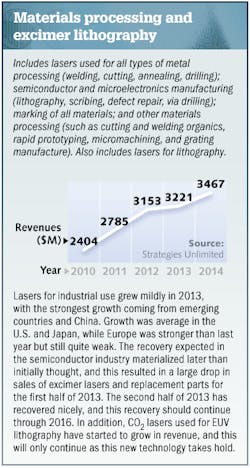

Materials processing and lithography

Comprised of marking, microprocessing (micromachining, semiconductor processing, additive manufacturing), kilowatt-scale macroprocessing (primarily metal cutting—still the largest industrial laser application), and laser lithography categories, materials processing laser sales reached $3.221 billion in 2013—a nearly 2.2% increase over the revised 2012 figure. For 2014, we forecast a healthy 7.6% increase to bring the total to $3.467 billion.

Manufacturing worldwide appears to be on the rebound after a slight dip in mid to late 2012, with the JPMorgan Global Manufacturing PMI reaching a two-and-a-half year high of 52.1 in October 2013. Sales growth in China and emerging countries led industrial laser shipments, with the U.S. following at a moderate pace, and Europe still trailing the pack. The increase is once again mostly attributed to increasing sales of fiber lasers and ultrafast or ultrashort pulse (USP) lasers for 'cold processing' micromachining applications.

"We saw revenues grow 12% for the nine-month period up to 3Q13," says Jack Chen, president of BWT Beijing (Beijing, China). "For 2014, our sales should increase 30% on 2013 total sales due to strong demand for our pump laser diodes to satisfy low-power pulsed, high-power CW, and ultrafast fiber laser requirements." For 2014, fiber lasers continue to lead in the marking sector and will even comprise one-third of all macromaterials processing laser revenues—rapidly gaining on the majority share enjoyed by CO2 lasers. For micromaterials processing, fiber laser revenues are nearly equivalent to CO2 and DPSS lasers.

In his 2013 Laser World of Photonics Munich presentation, Han's Laser (Shenzhen, China) VP and CTO Qitao Lue said that China's domestic industrial laser system sales were up 27% to $1.3 billion dollars in 2012, with the majority of systems used for marking applications. But Lue also said, according to a Laser World of Photonics 2013 conference review, that for a foreign laser company to succeed, it really needs to have a base in China.

Indeed, companies may want to consider the route taken by Spectrum Technologies (Bridgend, Wales)—an aerospace laser wire marking company—that changed its company status to become a Chinese Foreign-Invested Commercial Enterprise (FICE) and is moving to new larger offices in Shanghai. As a FICE, companies can distribute imported and locally manufactured products in China through their own wholesale, retail, and franchise systems.

In October 2013, Trumpf (Ditzingen, Germany) acquired a 72% stake in Chinese machine tool producer Jiangsu Jinfangyuan CNC, a company which Trumpf says is growing increasingly important in the laser cutting machine sector. Overall Trumpf sales for fiscal 2012/13 grew only 1%, but sales for its laser technology grew 8% to $919 million.

The China Compulsory Certification (CCC) or so-called 3C marking requirements are also forcing the need for more sophisticated ultrafast and UV lasers. "3C higher-quality marking requirements as well as hyperfine processing applications have enabled sales to double and redouble compared to last year," says Brenden Sun, marketing supervisor at Wuhan Huaray Precision Laser (Wuhan, China). "Short-term, high-volume laser deliveries are important to our customers, as well as the continuing need for shorter-pulse, shorter-wavelength lasers for flat-panel display and touchscreen processing, as well as emerging flexible displays."

"There are challenging opportunities for laser patterning in the display business," says Lars Penning, co-founder and CEO of scan-head manufacturer Next Scan Technology (Evergem, Belgium). "With fast-growing demand in Asia for large-area patterning applications, high-throughput 'cold' laser processing is able to replace operationally expensive and environmentally unfriendly wet etching and drive patterning costs down. To satisfy the growing demand in touch displays, IDTechEx says that more than 60 km2 of transparent conductive film needs to be patterned in 2013 and this amount will double in the next ten years." Penning cautions, "However, laser systems will only be accepted if power levels increase to deliver high throughput while at the same time, prices are reduced to justify changeover cost."

Laser manufacturers still waiting for the solar industry to increase adoption rates for laser processing should be encouraged by a GTM Research (Boston, MA) report that anticipates a global photovoltaic (PV) price increase of 9% next year as Japan, China, and the U.S. continue to support growing end-market demand. Rofin-Sinar (Plymouth, MI and Hamburg, Germany) recently wrote that it faced increasing demand for laser systems to enhance crystalline solar cell efficiency up to 1% through passivated emitter rear cell (PERC) and selective emitter processing. For the 12 months ended September 30, 2013, Rofin-Sinar saw net sales of $560.1 million dollars, a 4% increase over the same period last year.

In the semiconductor sector, a calendar Q3 sequential increase in sales for Newport Corporation (Irvine, CA) of $4.8 million (3.6%) was said to be driven primarily by microelectronics end market sales that increased approximately 20% to $34.7 million. And in November 2013, Newport entered into a $14 million collaborative development program for optomechanical subsystems for a "next-generation semiconductor equipment application."

Coherent CEO John Ambroseo echoed the improvement in semiconductor capital equipment in its Q4 fiscal year financial release, saying, "We received the first tranche of new ELA [excimer laser annealing] orders (greater than $15 million) and the ELA order pipeline for fiscal 2014 looks robust. There was marked demand improvement within the semiconductor capital equipment industry tied to the introduction of new wafer inspection tools."

So what about extreme ultraviolet (EUV) lithography? The calendar Q3 financial press release from ASML (Veldhoven, The Netherlands)—which acquired Cymer (San Diego, CA) in late 2012—revealed, "In the fourth quarter we expect to recognize revenue for one of the three NXE:3300B EUV systems that we expect to ship this year. The first series of such systems will not contribute to profit due to the low utilization of our EUV manufacturing infrastructure and early learning curve costs in our supply chain and, directly resulting from the Cymer acquisition, the cost of the liability to upgrade the first 11 EUV sources in the field, which is now assumed by ASML." Clearly, EUV is on its way, but it isn't here yet.

We forecast that the increased need for next-generation lithography tools will boost 2014 lithography laser sales (a subset of the overall materials processing segment) to $925 million from only $793 million in 2013—a nearly 17% increase. However, the 2013 figure represents a reasonable revenue drop compared to lithography laser sales of $817 million in 2012, reflecting late 2013 declining book-to-bill ratios for semiconductor capital equipment (stalling to < 1.0 in August and September 2013), according to SEMI (San Jose, CA).

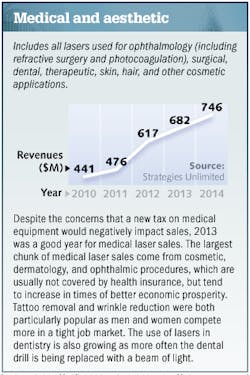

Medical and aesthetic

Even though the 2.3% U.S. medical device tax activated on January 1, 2013 has impacted some companies and new European Union RoHS II legislation will impact medical devices as of July 2014, sales of laser-based instrumentation in the medical (surgical, ophthalmic, dental, therapeutic) and aesthetic sector increased nearly 11% in 2013 to $682 million dollars. For 2014, we expect another nearly 10% increase to $746 million worldwide.

Ophthalmic laser company Iridex benefited from market acceptance for its MicroPulse tissue-sparing treatments for diabetes-related vision loss and glaucoma and saw 3Q13 revenues grow 21% to $9.5 million compared to the same period last year. The story was equally positive for the Surgical Ophthalmology business unit of Carl Zeiss Meditec (Jena, Germany), which grew 16.2% for the nine months ended June 30, 2013. In late 2013, Carl Zeiss Meditec launched its new MEL-90 excimer laser that achieves an intraoperative ablation speed of 1 diopter in only 1.3 seconds with a laser frequency of 500 Hz, reducing patient treatment times for an entire range of sphero-cylindrical corrections for the eye.

On June 24, 2013, aesthetic laser company Cynosure (Westford, MA) completed its acquisition of Palomar and saw 3Q13 revenue increase 64% for its laser and light-based product lines with particular demand in applications for skin resurfacing, wrinkle reduction, tattoo removal, body contouring, hair removal, and benign pigmented lesions. Cynosure is actively marketing its 755 nm, nominal 750 ps pulse duration and 200 mJ pulse energy PicoSure laser—the world's first picosecond laser for the removal of tattoos and benign pigmented lesions—in Europe, Canada, and the U.S., and just received Australian approval in late 2013. Before-and-after tattoo removal images speak for themselves: see www.cynosure.com/products/picosure/photos.php.

And although more clinical trials and laser cost reduction is needed for broader acceptance of lasers in dentistry, lasers are being used in 3D printing of dental implants and companies like Biolase (Irvine, CA) with its dual-wavelength iPlus WaterLase 2780 nm YSGG (yttrium-scandium-gallium-garnet) and 940 nm diode laser for nearly painless hard- and soft-tissue dental procedures are already benefiting from the growing dental laser market; Biolase saw net revenue of $41.2 million for the nine months ended September 30, 2013—an 8% increase over net revenues of $38.3 million for the same prior-year period.

Scientific research and military

The 3.7% expected growth in the 2013 Global R&D Funding Forecast from Battelle (Columbus, OH) and R&D Magazine (Rockaway, NJ) to $1.496 trillion did not take into account sequestration and attributes the largest projected share of the $53.7 billion dollar increase ($22.9 billion) to China, with U.S. and European funding projected to even fall short of the 1.9% and 1.5% inflation rates for those countries, respectively. "Larger companies with deeper reserves can somewhat withstand the lack of R&D funding for the military segment; however, smaller companies may be forced to close their doors and lose years of valuable research by senior scientists who may retire and leave these technologies as orphans without completion," says Ingrid Fuhriman, president of Stellar Photonics (Redmond, WA).

Despite proof-of-concept completion for its Plasma Acoustic Shield System (PASS) with green dazzler and proprietary Dynamic Pulse Detonation (DPD) system (wherein plasma generated by laser superheating of air in front of a target causes a bright flash of light and a loud bang), Stellar Photonics may fall victim to military laser cuts. "Work on a more-powerful eyesafe laser was two-thirds complete when funding ran out. Our warfighters are asking for nonlethal weapons and PASS is perfect for embassy, border, and mob protection," adds Fuhriman. "What a waste of taxpayer dollars."

"We see increasing competition with foreign suppliers trying to enter U.S. defense and industrial markets, with quite a few of our competitors being acquired by large multinational foreign companies as a means of gaining U.S. market share," says Michael Evans, VP of sensing and communications for SA Photonics (Los Gatos, CA). "However, our ability to introduce fundamental advances in compact and supercontinuum laser systems for oil and gas sensing and imaging, advanced helmet-mounted displays for military and medical applications, and inertial sensors for autonomous vehicles or UAVs represent diverse industries that will shield us from reduced military spending."

Evans continues, "Although several watershed technologies such as quantum defined structures in dots, wires, or tubes and new methods of device fabrication and integration are heralding a renaissance of emerging capabilities, many companies and agencies appear too ready to eat the seed corn and risk the starvation that comes from inadequate investment in laser and optical technology instead of strengthening peer review and technical exchange."

Hit especially hard by what many consider a 'manufactured crisis' in the U.S. in regards to shutdown/debt ceiling woes and by continued debt crises in Europe, global R&D and military laser funding suffered in 2013 and will continue its lackluster pace well into 2014, as evidenced by the performance and future outlook of large public companies like Newport and FLIR that are closely tied to R&D funding levels.

For its three-month period ended September 28, 2013, Newport's scientific research sales were down 6.4% and its defense and security end-market sales were down 16.7% compared to the prior-year period. And while 3Q13 revenue from FLIR Systems' (Wilsonville, OR) Commercial Systems division increased 17% from 3Q12 to $212.9 million, revenue from its Government Systems division decreased 4% from 2Q12 to $145.2 million, "…impacted negatively by weak book-and-ship order flow from the U.S. Government" according to the financial release.

Global scientific research and military laser spending reached a local peak in 2012, dropped in 2013, and only ticks up slightly for 2014 to $620 million total. Some good news is that of the 27,200 active U.S. federal opportunities listed on the Federal Business Opportunities (www.fbo.gov) website, a search with the keyword 'laser' over the 90 days prior to December 17, 2013 revealed 206 funding opportunities ranging from large-format laser cutters to turnkey diode laser systems to airborne laser mine detection systems. And in Europe, Horizon 2020—the European funding plan that succeeds Framework Programme 7 on January 1, 2014 as the primary R&D mechanism—includes a "substantial boost" for photonics programs, which are anticipated to be funded at a level of around $137 million per year through 2020.

Instrumentation and sensors

"Instrumentation OEMs in life science, analytical chemistry, and metrology still need high-power, high-performance greater than 100 mW DPSS lasers for fluorescence microscopy, Raman spectroscopy, interferometry and holography, as well as high-end flow cytometry and gene sequencing," says Phillip Amaya, president of Cobolt Inc. (San Jose, CA). "The demand for multi-wavelength modules to analyze the myriad of fluorescent fluorophores in microscopy applications, for example, continues to drive sales. We anticipate continued double-digit market growth because laser-based instruments are being used in more applications, the number of laser-based methods continues to grow, and the overall market is expanding in developing countries like China and India."

Flow cytometry represents a significant growth opportunity going forward as we detailed in our introduction, and spectroscopy continues to develop and evolve from larger, laboratory based instrumentation to smaller handheld and even numerous integrated and chip-based spectrometer options.

On the sensing front, no one can argue with the success of Microsoft's Kinect and the still-evolving list of both consumer and industrial applications that it is enabling such as visualizing biomedical holograms and improving robot vision. Apple is also betting on gesture recognition with its recent $345 million dollar acquisition of 3D sensor company PrimeSense (Tel Aviv, Israel). And IHS iSuppli forecasts that the global market for automotive proximity and gesture recognition systems will grow to more than 38 million units in 2023, up from less than a million in 2013.

In 2013, the instrumentation and sensors market for lasers grew more than 7% to $601 million dollars; our forecast calls for this trend to continue, with instrumentation and sensor laser sales reaching $646 million by 2014.

Entertainment and displays

Included in the entertainment and displays category are lasers used for light shows, head-worn displays like Google Glass, for picoprojection devices, and for laser cinema projectors.

The jury is out on whether head-worn display manufacturers will implement laser-diode-based or MEMS direct-projection systems over lower-cost LED or OLED displays. Not to mention that it's too early to tell how the public will respond to the newest headgear options.

And are picoprojectors dead? Maybe not. "While the millions of lasers forecast for picoprojectors have not yet materialized, there is a precedent for success," says Dale Zimmerman, VP of R&D at MicroVision (Redmond, WA). "Sony's Handycam with built-in picoprojector that is sold in retail with active demonstration and promotion outsells other picoprojectors passively marketed on the Internet at a rate of something like 10 to 1. Brookstone has also had success with in-store demonstrations; when people see picoprojectors in action, they are buying them."

Zimmerman says that MicroVisions' MEMS-based RGB PicoP technology is a superior 25 lumen, 720p, low-power-consumption, high-definition display. "Of course, you wouldn't want to use PicoP if you have access to a TV screen, but there are numerous situations where all you have is your cell phone or camera and want to display photos or watch video and want that larger screen, especially if you are sharing with others." Zimmerman argues that laser diode, 'video-out' devices, and optical miniaturization technologies have matured at a time when users are just beginning to understand the benefit of on-demand displays and video without the bulky tablet. "We see all these factors coming together in an ecosystem that will prove beneficial for picoprojection; companies like Nichia and Osram are investing in RGB laser diodes with the understanding that the hockey stick-shaped growth curve for picoprojection lasers could take shape soon."

Laser Focus World is also bullish on laser cinema projection per our introduction, but recognizes that significant laser sales in this category probably won't materialize for several years. However, laser pointer sales and sales of lasers into the entertainment industry for laser light shows will continue with a healthy growth pace of around 15.4% from the 2013 numbers, bringing our forecasted entertainment and display revenue to $210 million in 2014.

"2013 revenues for Pangolin and many other laser light show companies will beat 2012 figures," says Justin Perry, COO of Pangolin Laser Systems (Orlando, FL). "This year I've had the pleasure of traveling the globe, studying the laser entertainment markets in the USA, Europe, Asia, Australia, and South America. The popularity of laser shows globally continues to rise; no other light source can produce the novel and versatile effects that lasers can." Perry adds, "Thanks to our easier-to-use software and to 'pure diode' laser projectors, laser entertainment is making its way into new applications such as marketing, advertising, and even mainstream commercials including Absolut Vodka and Capital One finance."

Image recording

Fiber lasers are taking hold for micromachining of rotogravure print cylinders and for other gravure substrates, and red laser diode miniaturization is reducing the price and footprint for multifunction laser printers; however, the total laser market for laser printer and commercial laser pre-press and photofinishing revenues is neither growing nor declining. With revenue levels sitting at around $65 million dollars for the past 5 years, there is little reason to believe this segment will grow unless some new applications emerge.

FOR MORE IN-DEPTH ANALYSIS

Much more detail on the laser markets is available from Strategies Unlimited in its new report, Worldwide Market for Lasers 2014 (www.strategies-u.com). Details include forecasts to 2017 of laser units, average prices, and revenues by segment, estimates of market share, and discussion of the dynamics within each laser segment. The report is the only comprehensive report on the laser market, and the 12th in a series that includes fiber lasers and industrial lasers. Special topics reports in the series cover mid-infrared lasers and ultrafast lasers.

Strategies Unlimited specializes in photonics markets, including lasers, LEDs and lighting, and imaging. It was founded in 1979 and is located in Mountain View, CA. Strategies Unlimited is one of PennWell's many brands, which also include Laser Focus World, Industrial Laser Solutions, BioOptics World, Vision Systems Design, LEDs Magazine, and Lightwave.

ABOUT THE NUMBERS

The estimates and forecasts of laser shipments were based on both supply and demand side analyses by Strategies Unlimited, a PennWell business. Strategies Unlimited has been conducting market research in photonics products for more than 30 years, with specialties in lasers and high-brightness LEDs. The effort considered both quarterly trends and long-term historical trends; results were then compared and adjusted to correct for known errors. More information will be available from Strategies Unlimited and at the Lasers & Photonics Marketplace Seminar on Monday, February 3, 2014, held in conjunction with SPIE Photonics West in San Francisco.

About the Author

Gail Overton

Senior Editor (2004-2020)

Gail has more than 30 years of engineering, marketing, product management, and editorial experience in the photonics and optical communications industry. Before joining the staff at Laser Focus World in 2004, she held many product management and product marketing roles in the fiber-optics industry, most notably at Hughes (El Segundo, CA), GTE Labs (Waltham, MA), Corning (Corning, NY), Photon Kinetics (Beaverton, OR), and Newport Corporation (Irvine, CA). During her marketing career, Gail published articles in WDM Solutions and Sensors magazine and traveled internationally to conduct product and sales training. Gail received her BS degree in physics, with an emphasis in optics, from San Diego State University in San Diego, CA in May 1986.

Allen Nogee

President, Laser Markets Research

Allen Nogee has over 30 years' experience in the electronics and technology industry including almost 20 years in technology market research. He has held design-engineering positions at MCI Communications, GTE, and General Electric, and senior research positions at In-Stat, NPD Group, and Strategies Unlimited.

Nogee has become a well-known and respected analyst in the area of lasers and laser applications, with his research and forecasts appearing in publications such as Laser Focus World, Industrial Laser Solutions, Optics.org, and Laser Institute of America. He has also been invited to speak at conferences such as the Conference on Lasers and Electro-Optics (CLEO), Laser Focus World's Lasers & Photonics Marketplace Seminar, the European Photonics Industry Consortium Executive Laser Meeting, and SPIE Photonics West.

Nogee has a Bachelor's degree in Electrical Engineering Technology from the Rochester Institute of Technology, and a Master's of Business Administration from Arizona State University.

Conard Holton

Conard Holton has 25 years of science and technology editing and writing experience. He was formerly a staff member and consultant for government agencies such as the New York State Energy Research and Development Authority and the International Atomic Energy Agency, and engineering companies such as Bechtel. He joined Laser Focus World in 1997 as senior editor, becoming editor in chief of WDM Solutions, which he founded in 1999. In 2003 he joined Vision Systems Design as editor in chief, while continuing as contributing editor at Laser Focus World. Conard became editor in chief of Laser Focus World in August 2011, a role in which he served through August 2018. He then served as Editor at Large for Laser Focus World and Co-Chair of the Lasers & Photonics Marketplace Seminar from August 2018 through January 2022. He received his B.A. from the University of Pennsylvania, with additional studies at the Colorado School of Mines and Medill School of Journalism at Northwestern University.