Thin-film Coatings: Thin-film manufacturing considerations for semiconductor lasers

DAVID DOUGLASS

The semiconductor laser market has been growing at a phenomenal rate over the past 20 years, making up about 45% of the total $11 billion laser market.1 This has largely been driven by the fiber optics revolution. Initially, semiconductor lasers found a use as both signal lasers and pumps for telecommunication fiber amplifiers. Recently, they have found additional use as pumps for fiber lasers, which have largely replaced CO2 lasers for material processing applications such as metal cutting and welding.

While the semiconductor laser market growth is impressive, the market size is still dwarfed by the overall $350 billion semiconductor microelectronics market, with correspondingly small unit volumes. Semiconductor microelectronics manufacturers spent about $3 billion on physical vapor deposition (PVD) capital equipment in 2017, while semiconductor laser manufacturers spent about $200 million for similar tools.

In addition to the difference in market size between these industries, there is also a major growth strategy difference. To prevent duplicate effort and investment in microelectronics, there is an industry-wide roadmap for production technologies. Meanwhile, semiconductor laser fabs all use different toolsets and processes to achieve similar aims, and process information is tightly held as trade secrets.

Given the large differences in roadmap technology sharing and scale, it would initially seem unlikely that the laser industry would benefit from microelectronic equipment practices. In fact, many of its practices are directly relevant and are already being adopted by leading semiconductor laser equipment vendors. These suppliers are large enough to have developed proprietary platforms and control systems, and offer processes as well as equipment support, yet small enough to provide the platform customization needed to meet the unique needs of each manufacturer. We will explore some of these practices considering both the process equipment and factory cost of ownership.

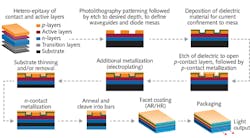

Typical process flow

Figure 1 shows an example of a laser bar manufacturing process. The diagram shows typical steps in the production flow and is not intended to be comprehensive. Many of these steps are outside the scope of this article—for example, the active light-producing layers and their surrounding contact and buffer layers require molecular beam epitaxy (MBE) or metal-organic chemical vapor deposition (MOCVD), depending on the wavelength.

Although this fabrication step requires significant development and is critical to internal device efficiency and output light properties, it does not alone determine the final laser diode performance. The design and quality of the passive thin films around the active layer stack are the essential elements determining how internal diode efficiency is converted to final external device performance.

These passive films include reflectivity coatings, metallization layers, and dielectric coatings, among others. In this article, we will explore some of the key considerations of these thin films.

Considerations for individual thin films

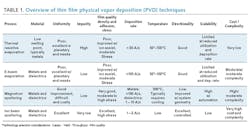

There are a number of PVD techniques available for fabrication of passive layer thin films. Table 1 illustrates some of the differences among these techniques, along with how these differences translate into technology selection considerations. It also ranks the technologies broadly from lowest cost/lowest quality to most expensive/highest quality.

In general, the deposition technology choice will always come down to a tradeoff between capital expense, yield, throughput, and film quality. The film quality requirements will dictate which technologies can be considered, and the productivity requirements (both current and future) will drive the final decision. Let us examine these requirements in more detail and go through the thought process of technology selection using a couple of application examples from Denton’s experience.

When considering thin film properties, we can generally group them into two types: intrinsic, such as physical and chemical properties of the film; and extrinsic, such as uniformity, repeatability, and throughput. Intrinsic properties primarily impact product performance and will depend on such things as material system selection and layer design, deposition technology selection, process control precision, and deposition environment integrity. Extrinsic properties will also depend on deposition technology selection, and additionally on deposition system design and deposition system quality.

Let’s look at the reflective facet coatings, the so-called antireflective (AR) and high reflectivity (HR) coatings. These coatings define the ends of the laser cavity and provide the optical feedback required to turn an optical gain medium into a laser.

AR coatings

• Decrease reflectivity of the facets through which light enters and exits laser cavity

• Single layer or alternating dual material (high/low refractive index) stacks

• Typical materials: titanium dioxide (TiO2)/silicon dioxide (SiO2), tantalum pentoxide (Ta2O5)

• Reflectivity 3–10%

HR coatings

• Stop light emission from the rear facet of the diode and reflect most of the light back into the laser cavity

• Alternating dual material (high/low n) stacks

• Typical materials: Aluminum oxide (Al2O3)/Si, zinc selenide (ZnS), TiO2, and SiO2

• Reflectivity 90–99.9%

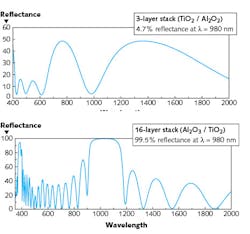

In the case of AR/HR films, the intrinsic properties include reflectivity, absorption, scattering, and laser damage threshold. Figure 2 shows typical reflectance vs. wavelength data for AR and HR coatings.

FIGURE 2. Typical reflectance vs. wavelength for AR and HR coatings for low-power laser bars (left; Example 1); and for high-power laser bars (right; Example 2).

Example 1: AR/HR films for low-power laser bars in high-volume manufacturing. For this application, the laser diodes will run at low power. As a result, film quality requirements are not particularly challenging and key coating requirements are high throughput and low cost. With this in mind, let’s go through the technology selection exercise.

First, we identify the critical intrinsic and extrinsic film characteristics. In this case, intrinsic requirements are good adhesion and minimal oxidation of the native cleaved surface. The extrinsic requirement is low cost.

Next, match the film requirements with available technology. In this case, adhesion and oxidation concerns are best addressed by utilizing an in situ ion source for pre-clean, and a flip-fixture (a special fixture that allows exposure of both sides of the substrate, one side at a time, to the evaporant plume) to prevent breaking vacuum between the AR and HR runs. Low cost is achieved by using e-beam evaporation. Note that the flip fixture will also help with productivity, as both coatings are run in one batch.

In this case, there is no reason to sacrifice capital and throughput by choosing ion beam sputtering, for example, because there is no need for very high-quality film. However, it is a good idea to invest in an in situ ion source, as that will meet the intrinsic requirements of adhesion and minimal oxidation.

Example 2: AR/HR coatings for high-power laser bars. Unlike Example 1, these devices are running at high power and a critical requirement is the ability to withstand high laser damage. The manufacturer also requires tightly controlled optical properties.

In this case, in addition to good adhesion and low surface oxidation, the required intrinsic properties are high film density, low defect density, and low refractive index shift when exposed to air. Extrinsic properties include a high-count multilayer film stack, tight uniformity, and excellent repeatability of individual layers. Even though the materials to be deposited and the basic functionality are similar to Example 1, the requirements lead to a very different choice of technologies.

For intrinsic properties, an ion source is again needed, but in this case for both pre-clean and assisted deposition. For high-count multilayer film stacks, evaporation is not suitable and sputtering is needed. Magnetron sputtering is well suited to the requirements. High uniformity is addressed by optimized throw distance and source location.

For high repeatability of individual layers, an in situ monitor is required. For high-count multi-layer film stacks, the requirements are quite stringent and a high-precision/high-cost optical monitoring system (OMS) is favored over the less expensive and complicated (but less precise) quartz crystal monitor (QCM).

This is, of course, a highly abbreviated explanation of how one would arrive at the proper tool configuration. Note that both examples could be described as "AR/HR for laser bars." By focusing on the significantly different coating requirements first, one arrives at very different configurations to satisfy two significantly different manufacturing requirements.

Process equipment

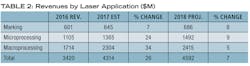

Going back to our earlier comparison between the semiconductor microelectronics market and the semiconductor laser market, let us look at some of the key differences summarized in Table 2. Given the very different characteristics outlined, it would appear at first glance that there won’t be much for the laser industry to learn. This couldn’t be more wrong!

Market size aside, the current characteristics of the laser market shown in Table 2 would have been true for the microelectronics industry 30 or 40 years ago. As the microelectronics market grew and technology advanced, it became impractically expensive to pursue independent R&D and keep all technology in-house, and the industry adopted a unified technology roadmap out of necessity.

Over the past decade, the LED industry began a similar transition. The semiconductor laser market looks to be in a similar position. Growth has been phenomenal, but to expand into large-volume applications such as automotive headlights or lidar for self-driving cars, production costs will need to drop by at least an order of magnitude.

Current laser fabs are small, and production equipment tends to be scaled up versions of R&D units. When looking to purchase equipment, engineers will often specify the hardware first, detailing the deposition technology, number of sources, tool architecture, etc. The vendor is generally viewed as an integrator, and the large number of potential vendors are played off against each other to achieve the lowest tool price.

This method works well for many simple applications or for more general-purpose R&D equipment, but is not optimum for key process steps. The method will generally result in functional hardware that may or may not meet the actual process needs.

In contrast, following the microelectronics model, some in the industry are starting to specify film requirements first, and work with vendors as collaboration partners. There are a handful of capital equipment vendors in the laser space that have experience with the same application across multiple customers. Through collaboration with vendors who focus on application-specific systems, engineers gain the benefit of a standardized product that addresses issues they may not have encountered yet—but their competitors have. In this case, the result is a working production process.

Factory costs

Finally, let us conclude with another higher-level consideration, that of the factory cost of ownership. Since unit volumes are currently relatively small, there are a small number of tools required for each process step. By working with vendors as integrators, factories tend to end up working with a large number of different vendors—perhaps a different one for each process step!

By working in this mode, there are a few obvious consequences—the customer is fully responsible for the entire manufacturing process flow, and individual vendors will not have any particular insight into how the tools need to fit together. Additionally, service can be an issue since every vendor will have only a small investment in any one customer.

By partnering with a small number of vendors, each vendor is able to gain a better understanding of factory requirements and is better able to integrate new tools into manufacturing. The tools will have a similar look and feel, so operator training is minimized. With a larger installed base, vendors can commit to faster service response as well. The outcomes are faster production qualification, better service response, and a higher factory uptime.

There are a few key points to keep in mind when selecting thin film capital equipment. Always choose the process technology that best meets your production requirements. Don’t buy more capability than you need just because it is better, and don’t buy less capability than you need because it is cheaper—evaluate the total cost of ownership and not just the capital expense.

Finally, partner with the fewest number of carefully selected vendors to improve overall factory uptime and time to market.

REFERENCE

1. G. Overton, A. Nogee, D. Belforte, and C. Holton, "Where have all the lasers gone?" Laser Focus World, 53, 1, 32–52 (Jan. 2017).

David Douglass is senior product manager at Denton Vacuum, Moorestown, NJ; e-mail: [email protected]; www.dentonvacuum.com.