Review and forecast of the laser markets Part I: Nondiode lasers

The Laser Focus World 2002 Annual Review and Forecast of the Laser Marketplace is conducted in conjunction with Strategies Unlimited, an optoelectronics market research firm based in Mountain View, CA. Part I of the review reports on the overall market and focuses on nondiode laser markets. Part II, written by Robert Steele of Strategies Unlimited, covers the diode-laser marketplace and will be published next month—Ed.

KATHY KINCADE, Contributing Editor and STEPHEN G. ANDERSON, Editor in Chief

Making predictions about the future of an industry or market is always risky, but these days it seems even more so. Added to the usual host of variables and indicators—profits, losses, margins, recessions, depressions, recoveries, overcapacity, consumer confidence, GNP, and GDP, to name just a few—is something less tangible, but no less compelling: we are waiting for the other shoe to drop.

This time last year, the future seemed infinitely bright. The laser market was in the midst of unprecedented wealth and prosperity, thanks in large part to the use of diode lasers in wavelength-division multiplexing (WDM) and other telecom applications. Telecom lasers accounted for 58% of the total laser market in 2000, which we estimated would top out at $8.8 billion ($6.6 billion for diode lasers, $2.2 billion for nondiode). In addition, according to the National Venture Capital Association (Arlington, VA), venture capitalists invested $2.6 billion in 161 optical components and systems companies in 2000 as telecom carriers began building out optical networks at breakneck speed. The semiconductor market also experienced a growth surge, which helped semiconductor equipment manufacturers—particularly those involved in excimer-laser lithography—see their sales jump in 2000.

But as everyone knows, the bottom fell out of the Internet economy and we now find ourselves in the midst of a worldwide recession, with no clear indication of its depth or when it might end. This turn of events has had a dramatic impact on the laser and optoelectronics industry, particularly those companies selling into the telecom, semiconductor, and capital-equipment markets—the very markets that one year ago helped many of these firms achieve record revenues.

In fact, the numbers for 2001 are downright depressing. Based upon the staggering growth we saw in the telecom market in late 1999, last year we revised estimates for the laser market upward for 2000, from $6.3 billion to $8.8 billion. We also said last year that, given the market’s momentum, we expected 2001 to be another banner year, with revenues gaining 30% to reach $11.5 billion.

In fact, we have now revised our numbers for 2001 down considerably, to $5.62 billion—$3.65 billion for diode lasers and $1.96 billion for nondiode lasers. This means the market actually fell 36% in 2001. Fortunately, growth is expected to return in 2002. According to our estimates, we believe the overall laser market will gain 10% over the next year, reaching $6.17 billion—$4.1 billion for diode lasers and $2 billion for nondiode lasers.

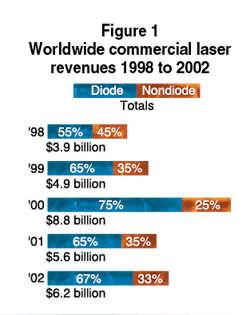

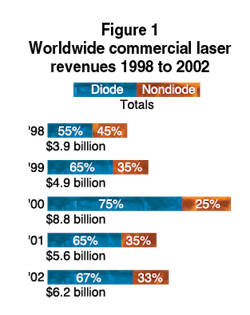

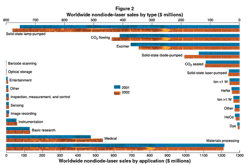

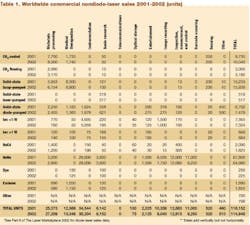

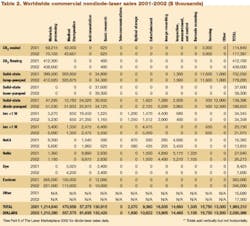

Total worldwide commercial laser revenues for 1998 to 2002 are charted in Figure 1. Nondiode-laser sales data for 2001 and 2002 are charted in detail by application and laser type in Figure 2. Tables 1 and 2 provide nondiode-laser sales data by unit shipments and dollar revenues respectively. The corresponding charts and tables for diode lasers will appear next month. See also "Where the numbers come from." Readers also should note that sales of fiber lasers and metal-vapor lasers are included in the “other” laser category, but we are unable to publish any applications-specific data for these lasers.

The data presented in the tables are available with additional commentary in the January 1 issue of Optoelectronics Report. The survey data also will be analyzed at the 16th annual Laser and Optoelectronics Marketplace Seminar on Monday, Jan. 21, which is held in conjunction with Photonics West (San Jose, CA) and is sponsored by Laser Focus World in conjunction with Strategies Unlimited. (For more information, see www.marketplaceseminar.com.)

Recession, depression, or correction?

So, what happened? A combination of factors that have pushed the United States and the other major world markets into what many believe is a true, albeit soft, recession. In the United States, the economic downturn comes on the heels of, and is fueled in good part by, the Internet “revolution,” which spurred tremendous demand for bandwidth. Business spending on new technology was the principal growth engine in the United States during the late 1990s, with information technology leading the charge. Spending on IT-related goods and services rose from $227.5 billion in 1995 to $713 billion by the end of the decade, accounting for almost 25% of all GDP for that period.

This rise in demand prompted a parallel rise in the development and manufacture of the products and services needed to support it: optical networks, data storage servers, Internet and application service providers, high-speed personal computers, wireless handheld devices, and the multitude of bits and pieces that go into them, including semiconductors, displays, optics, fiberoptics, lasers, and other optoelectronic components. But once the realities of supply and demand pulled the plug on the dot-com dream, those brick-and-mortar businesses that had supported the Internet economy lost much of their newfound momentum.

So too did the telecom industry. Over the past year, Nortel, Lucent, Marconi, and numerous other service providers have watched their financials take such serious nosedives that investors have panicked and key executives resigned. Nortel reported third-quarter 2001 losses of $3.47 billion on revenues of $3.7 billion, compared to losses of $586 million on revenues of $6.7 billion for the same quarter in 2000. Nortel’s stock fell more than 80% in 2001, pacing a decline by fiberoptics-related companies and networking stocks as demand from carriers dried up and inventories built up in warehouses.

Marconi also blames its problems on the profound downturn in telecom equipment sales. Some 25% of Marconi’s workforce has been laid off, the CEO and chairman have resigned, and the company has been slammed with shareholder lawsuits. Some analysts think the company won’t survive the telecom downturn without a cash infusion of $2 billion to $3 billion from an outside source. In November Marconi posted the largest-ever corporate loss in the U.K., announcing half-year losses of $7.3 billion.

Even JDS Uniphase saw its meteoric rise to the top of the telecom components heap come to a screeching halt in 2001, as carriers sharply reduced their capital expenditures for next-generation networking equipment. The company reported a staggering $46 million loss for FY2001, and things hadn’t improved much by the first quarter of 2002 when the company announced a loss of $1.2 billion on revenues of $329 million, compared to a loss of $1.07 billion on revenues of $786 million for the same quarter in FY2001.

And the situation is not limited to the United States. Like the U.S., the European Union has suffered a tremendous downturn in the telecom, semiconductor, and machine-tool industries, prompting slower growth, higher inflation, and an 8% unemployment rate. The situation is much worse in Japan, where analysts say the recession there could well turn into a full-on depression, if it hasn’t already. The Nikkei index plunged 25% in the latter part of 2001, falling below the 10,000 mark for the first time since 1983, and unemployment is hovering between 5% and 6%, with all of the major corporations—including Sony, Komatsu, and Kobe Steel—announcing major layoffs of 10% and even 20% of their workforce. While Japanese policy makers have been working to create a more favorable exchange rate and lowering interest rates to record levels, the cheaper yen still is not stimulating Americans, Europeans, or even Asians to buy Japanese-made goods.

World events spur defense

The world’s economic problems were made even worse by the events of September 11, which rocked Wall Street and exacerbated an already unstable economic situation. And although everyone agrees that the best course of action is to try to return to business and life “as usual” and there are some clear signs of economic stabilization, we cannot help but look over our shoulders now and then, wondering.

On the up side, the attacks on the World Trade Center and the Pentagon have prompted the U.S. government to shift its position on military spending and commit more resources in this direction, with particular emphasis on laser and optoelectronics technologies. Rather than developing primarily defensive weapons, the military is now looking to utilize and deploy advanced software and electronics technologies as part of a more targeted seek-and-destroy approach to warfare.

Similarly, while the problems in the telecom and semiconductor industries have had a negative effect on many European laser and optoelectronics providers, other markets appear more stable, particularly industrial and defense. The trade association UKLEO (Melbourn, England) and the British industrial-laser users association AILU (Abingdon, England) both report that business in areas outside telecom has been largely unaffected, and several European industrial-laser manufacturers, including Trumpf and Lambda Physik, reported decent growth in certain nontelecom businesses in 2001. Trumpf’s business was up 35% overall last year, while Lambda Physik reported revenues of $91 million for the first nine months of 2001, a 55% increase over revenues for the same period in 2000. Much of Lambda Physik’s growth came from the industrial applications division, particularly excimer lasers used in the production of flat-panel displays.

The European defense sector also appears to be doing well. Thales Optronics (Glasgow, Scotland), formerly Pilkington Optronics, announced a $330 million order from the U.K. Ministry of Defense in late 2001, the largest order the company has ever received. The contract covers vehicle optoelectronics systems on the Battle Group Thermal Imaging (BGTI) program, and the number of vehicles to be converted with BGTI equipment is around 700. Another European firm doing well in the defense sector is Sagem (Paris, France). For the first nine months of 2001, the company’s defense business was up 5% over the previous year, while its communications business was off by about 40%. In addition, in 2001 the company received more than $88 million in orders for optoelectronic sights for armored vehicles. These contracts are expected to help offset the problems the company is encountering in its telecom business.

Thus, despite all the uncertainty surrounding terrorism and the war in Afghanistan, many analysts are predicting that this recession will be one of the shortest and mildest in history. The Organization of Economic Cooperation and Development (OECD), for example, stated in November 2001 that, after slowing to a virtual standstill in 2001, the global economy will recover strongly late in 2002.

Not surprisingly, the OECD sees U.S. industry and government policy as critical to helping the rest of the world emerge from its economic doldrums. U.S. companies have responded quickly to the downturn with cutbacks and downsizing, oil prices are falling, and interest rates are at their lowest level since the early 1960s. With the shock of September 11 beginning to wear off, there is a growing sense that we are merely in the downside of a typical business/technology cycle that will allow many firms to regroup and better prepare for the next surge in demand. In fact, some say we are about to crest a new wave of technological innovation that will pull us out of the current economic slump more quickly and leave us better positioned to meet the next growth spurt in the tech sector. They are convinced that we cannot depend solely on conventional market stimulators, such as lower interest rates, to pull us out of this recession. This time, we must also invent our way out of it.

Some bright spots

What does all of this mean for the laser and optoelectronics industry and the multiple markets it serves? So much depends upon the telecommunications and semiconductor sectors, and the general consensus is that these markets will remain weak for at least another 12 to 18 months. But that does not mean the laser and optoelectronics markets will flounder for the next two years. In fact, bright spots do exist.

Foremost among these are the scientific (or what we term “basic research”), printing, defense, and emerging micromachining and biomedical markets. And while the telecom market has left many laser and components suppliers struggling in the past year, those companies that have remained diversified have taken solace in the stability of their scientific business. In fact, this market segment did better in 2001 than we predicted it would, showing 20% growth for nondiode lasers. This shift helped companies like Spectra-Physics (Mountain View, CA) and Coherent (Santa Clara, CA) increase year-over-year sales of several product lines.

Technology continues to play a significant role in creating new market opportunities as well. The shift away from lamp pumping of solid-state lasers toward diode pumping, for example, continues to gain momentum, increasing its impact on markets ranging from basic research to materials processing. Many laser suppliers believe this will be a growth opportunity for several years to come, especially with the increasing output power and reliability and falling cost of diode lasers and diode-laser production. These dynamics also are having a growing impact on the market for nondiode lasers. New wavelengths, more power, and lower cost mean diode lasers can address markets previously inaccessible to them. (Editor’s note: The diode-laser market will be discussed in greater detail in Part II of this article in the February 2002 issue.)

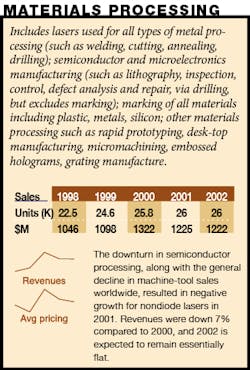

Materials processing

The economic downturn had a dramatic effect on all sectors of the materials-processing business, from semiconductor manufacturing to metal processing, marking, and micromachining. Hardest hit has been the semiconductor business, which took a major nosedive in 2001.

This turn of events had a parallel effect on sales of excimer-laser-based lithography equipment and sales of HeNe lasers for measurement applications within semiconductor manufacturing. Last year we forecast that 985 ($426 million) excimer lasers would be sold in 2001; this number has now been revised to 560 units ($250 million, down $176 million). The trend is expected to continue into 2002 with a further drop of 13% to 490 units ($210 million).

Not surprisingly, companies such as Cymer (San Diego, CA), the leading supplier of excimer-laser lithography systems, have seen their financials plunge from the profit to the loss column in the past year. Cymer reported a loss of $2.8 million on revenues of $53 million for the third quarter of FY2001 (ended Sept. 30), compared to income of $18 million on revenues of $98 million for the same quarter in FY2000. As a result, the company has cut 11% of its workforce, instituted mandatory shutdowns at Thanksgiving and Christmas, and introduced a salary-reduction plan.

But as 2001 came to a close, there were indications that the market was beginning to turn around, although semiconductor manufacturing still exhibited no real signs of life. In a statement released on Oct. 31, Gartner Dataquest (San Jose, CA) said that, after declining 35% in 2001 to $147 billion, global demand for semiconductors should begin to pick up in 2002, rising 3% to $152 billion. By 2003, this trend is expected to take on more steam, with a 30% increase in sales. According to Dataquest, demand will be driven by improvements in the overall economic environment, which should result in new demand for replacement personal computers and the anticipated rollout of third-generation mobile phone services.

In line with these predictions, the U.S. SEMIndex, a stock index of 47 North American manufacturers of semiconductor equipment and materials that is compiled by Semiconductor Equipment and Materials International (SEMI), rose 37% in October. This compares to a 17% jump in the Nasdaq Composite Index for the same period.

Also hard-hit by the telecom downturn was the fiber Bragg gratings business. Companies were gearing up at a breakneck pace to manufacture them using either excimer, metal vapor, or argon ion lasers, which resulted in enormous surplus capacity. While a few startups continue to enter the market, on a general scale the bottom dropped out of this market (for lasers) between April and June 2001. This alone accounts for an adjustment of about $35 million between the 2001 number last year and this year’s restatement. Any turnaround for the laser makers in this particular market will be slowed by the many unused but “previously owned” lasers that are reportedly now on the market at resale prices.

The near-term future does not appear that bright for metals processing either. Although this sector has not been hit quite as hard as the semiconductor manufacturing business, growth has been stymied by the overall world economic situation. Our numbers show revenues in this sector growing by only 1%, not the 11% growth we forecasted a year ago. And no real turnaround is expected until the latter part of 2002, according to David Belforte, editor of Industrial Laser Solutions.

Belforte notes that hardest hit has been the high-power carbon dioxide (CO2) laser business, which represents about 40% of worldwide industrial-laser sales. U.S. companies alone saw a 40% drop in sales of these lasers in 2001, with only 400 to 500 units sold. The marking business has also seen a downturn. Solid-state lasers, however, saw a slight upswing in sales, according to Belforte.

In addition, the landscape of the industry is changing. Corporate consolidation is on the rise, and Belforte expects there to be some serious “blood-letting” in the sheet-metal systems business this year. The sealed CO2 laser business (both high and low power) is also experiencing a surge in competition, with market leaders Synrad and Coherent no longer the only players. In the high-power sealed CO2 arena, they are being challenged by Rofin-Sinar, especially in Europe; on the low-power end, ULS and DEOS (which was acquired by Coherent in mid-2001) are both making significant inroads in the marking and engraving markets.

As in other market sectors, however, there are some bright spots. These include aerospace, power and energy (such as land-based turbines), and the manufacture of medical and dental instruments. In addition, Belforte notes that with the increasing competition for customers, the coming year should see a buyers’ market for metal processing equipment. And new sealed-CO2 laser wavelengths (9.3 µm rather than 10.6 µm) are expected to open up new opportunities in this sector, making it possible to process some nonmetal materials that previously could not be processed with a laser.

In fact, nonmetals micromachining is moving out of the process-development phase and emerging as a strong growth market. In addition to the new CO2 wavelengths, the increasing viability of certain ultraviolet lasers is making it possible to machine parts with feature sizes in the 10 to 100 µm range with micron or submicron accuracy: these items include ink-jet printer heads, fuel injectors, PCB boards, and disk-drive microwells.

Military/aerospace

With so many laser companies that once relied upon the military for the bulk of their business having shifted their focus to the commercial sector in the last decade, there has been little new to report in the defense-laser business, aside from the occasional big project awarded to consortia of major aerospace vendors and the occasional small laser supplier. But the September 11 attack has changed all that. While most laser firms are reluctant to discuss the defense sector and our numbers actually reflect a downturn in the past year, one thing appears certain: sensors, lasers, optical scanners, infrared cameras, thermal imagers, and other optoelectronics-based devices will play an unprecedented role in the new war on terrorism.

High-power laser-based weapons are already part of the military’s missile-defense program, and last July the Bush Administration pledged continued support for the development of a number of weapons that would seek to destroy ballistic missiles. Ongoing projects include the Airborne Laser, a laser-equipped Boeing 747 being designed and built by a team of contractors that includes TRW, Boeing, and Lockheed Martin (see Laser Focus World, September 2001, p. 58); the Tactical High-Energy Laser, which has received more than $250 million in funding from the United States and Israel since 1996; the Advanced Tactical Laser, which aims to mount a 300-kW oxygen-iodine laser on a helicopter or small plane to fire on ground-based targets; and a $100 million effort set to begin in 2003 that could solve the fueling problem for these weapons by replacing the chemically fueled lasers with high-power Nd:YAG lasers.

These projects have found strong support in the U.S. Congress, which passed a $360 billion defense budget for fiscal 2002. This is a 16% increase over the 2001 budget, and some analysts predict that the defense budget will reach $500 billion by 2005. The expected surge in spending will differ in many ways from traditional military buildups and boost employment for software and electronic engineers and other high-tech workers, with more resources going toward the development of weapons systems that employ sensors, low-power lasers, and optical scanners.

While the general consensus is that primarily small companies in the laser and optoelectronics industry will benefit the most from this shift, at least one major player is also expected to see a positive impact on its bottom line: TRW. Under the leadership of new CEO David Cote, the company is working to transform its image from that of an auto components supplier to a high-end technology company. Currently, TRW’s auto parts operations account for 64% of its $17 billion annual sales but only 38% of its pretax profit, while its space and technology divisions contribute 62% of the company’s profit on 36% of its revenue.

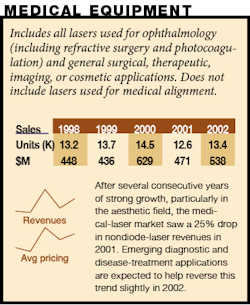

Medical equipment

After several consecutive years of strong growth, particularly in the aesthetic field, the medical-laser-systems market has matured to single-digit revenue growth, creating an increasingly competitive climate. Following the phenomenal successes of skin resurfacing, hair removal, and vision correction, the medical-laser industry as a whole is struggling to find the next large-scale application. Each of these consumer markets has reached a certain level of maturity and, in some cases, saturation, leaving many companies—especially those with limited product portfolios—wondering where their next bankable revenue stream will come from.

As a result, our numbers for the medical-laser components business show a parallel decline—the first time in nearly a decade that this market sector has decreased. Actual nondiode unit sales in 2001 were 12,568, 18% lower than the 15,268 we had forecast. Likewise, revenues were 30% lower than we had forecast; a year ago we said nondiode revenues in this sector would reach$670 million, but our revised numbers show actual revenues were only $471 million.

According to Irving Arons, an independent consultant and contributing editor to Medical Laser Report who supplies our medical market numbers, a few positive moves occurred during 2001. The dental market appears to be embracing laser systems with renewed vigor, which bodes well for erbium and diode lasers used in hard- and soft-tissue applications. Photodynamic therapy also seems to be making commercial progress, especially for the treatment of certain skin and eye diseases. In fact, although the refractive surgery market has experienced a significant downturn in the last 12 months, the disease segment of the ophthalmic market is growing.

Looking ahead, laser-based devices for the diagnosis and treatment of age-related macular degeneration, glaucoma, cancer, chronic skin conditions, dentistry, and other large-scale consumer applications hold the strongest near-term promise. But with so many companies vying for market share, each piece of the pie inevitably ends up smaller than is needed for most of these firms to survive. We anticipate nondiode laser revenues will increase 14% in 2002 to $538 million.

As is typical of a maturing industry, corporate consolidation continues in this market, widening the gap between the “haves” and “have nots.” The number of mid-sized companies continues to decline; instead, the medical-laser market is increasingly dominated by a few major players, with some startups and small technology-development companies keeping the fires of innovation burning.

Foremost among the major players is Lumenis, the company created from the mid-2001 merger of ESC Medical and Coherent Medical (see Medical Laser Report, March 2001). Lumenis is already considered the global leader in this market; combined sales for ESC and Coherent in 2000 totaled $360 million; this compares to $69 million for Candela, the companies’ closest competitor in the aesthetic and surgical markets.

Readers should note that many medical-systems manufacturers do not participate in our survey. To derive the laser-source revenues reported here, we rely on Arons, who tracks medical-system end-user sales within this market sector. Revenue projections by Arons are based on medical-system sales to medical end-users—the laser is only one component of these sales. The numbers in our tables, however, are based on revenue estimates of the laser source itself. For more specific discussion of the medical market by laser type, see the January 2002 issue of Medical Laser Report.

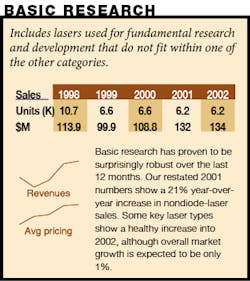

Basic research

While the more glamorous telecom and semiconductor market sectors have hit hard times, basic research has proven to be surprisingly robust over the last 12 months. Our restated 2001 numbers show a 21% increase in sales compared to 2000 and several laser companies report that their scientific business has actually helped them stay afloat during the high-tech downturn. Most of this increase for 2001 comes from product-mix changes involving solid-state and ion lasers, with a resulting increase in average sales price.

Last year we highlighted two trends that were evident within this market segment: the increasing importance of diode lasers, and how diode-pumped lasers continue to gain ground as turnkey research-grade systems are continually improved. Although diode-laser revenues this year are significantly lower than last, the trend is still in that direction. And although revenue growth of diode-pumped systems is not up significantly over 2000, key laser types such as ultrafast systems show a healthy 15% increase into 2002. However, the overall forecast for this segment into 2002 is more in keeping with the general economic outlook: revenue growth of only 1% over 2001.

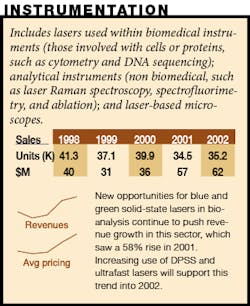

Instrumentation

Like most other technology sectors, instrumentation experienced a downturn in 2001—at least in unit sales. Our numbers show unit sales fell from 39,900 in 2000 to 34,500 in 2001. At the same time, however, revenues jumped from $35.7 million in 2000 to $57.3 million in 2001—even higher than the $43.2 million we had forecast. Sales of diode-pumped lasers, both continuous wave and ultrafast, apparently were higher than expected last year.

Much of the growth in this sector is being driven by new opportunities in biomedical instrumentation. As has been the case in recent years, companies offering laser-based instrumentation are turning to the life-sciences market, according to Philip Greenfield, managing editor of Instrumenta (formerly Analytical Instrument Industry Report) and Genomika (Surrey, England). Virtek Vision created Virtek Biotech after buying FONA; Axon/Zyomyx (among others) are collaborating in the development of protein-chip scanners, in addition to the numerous DNA chip scanners now available for sequence information acquisition; and laser-induced fluorescence detection (LIF) is increasing in popularity, with Picometrics (Ramonville, France) signing a U.S. distributor, ESA (Chelmsford, MA), to market its ZETALIF detectors to customers in pharmacology, neuroscience, molecular biology, toxicology, and trace analysis.

These and other applications are creating new growth opportunities for bioanalytical instrumentation, such as the increasing use of blue- (488 nm) and green-output solid-state lasers instead of low-power ion lasers and an increase in the use of diode-pumped and ultrafast lasers. In fact, this subcategory saw an 82% jump in unit sales in 2001, four times the 24% growth we had forecast. We expect this trend to continue into 2002, although at a much more modest pace.

The analytical category also saw an increase, although not nearly on the scale of the biomed market—12%. Key events in this segment in the past year include Siemens’ (Erlangen, Germany) purchase of AltOptronic (Goteborg, Sweden), a producer of laser diode-based spectrometers and fiberoptic sensors for applications in hostile environments; Photoelectron’s (Lexington, MA) move into the industrial sector with its miniature x-ray fluorescence measurement device, Laser-X; and the formation of Tiger Optics by Meeco (both Warrington, PA) to commercialize cavity ring-down spectroscopy for moisture and contaminant analysis in semiconductor manufacture.

Other emerging technologies and applications in the instrumentation category include laser-induced breakdown spectroscopy, with the first commercial products now appearing on the market from Pharmalaser (Boucherville, QC, Canada) and a handful of other firms; TSI’s (Shoreview, MN) aerosol time-of-flight mass spectrometer; and the trend toward laser-based portable tools, such as the 20-lb InPhotote Raman spectrometer from Inphotonics, to replace conventional bulky instrumentation in such applications as onsite forensic and environmental analysis.

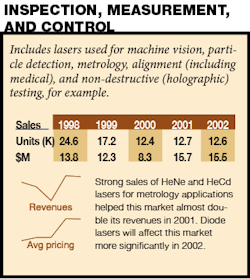

Inspection, measurement, and control

The decline in the semiconductor and telecom businesses has had a parallel effect on the test-and-measurement market. Some industry observers note that many customers who bought test equipment in 2000 to characterize components are sitting on those instruments and in some cases looking to resell them.

Still, several survey respondents noted that the scientific-measurement market has held steady over the past year. As a result, the restated nondiode laser revenues in 2001 are up significantly (about double) from last year's number, primarily because of sales adjustments of HeCd and HeNe lasers. The higher HeNe revenues result from increased average prices, reflecting an increasing market for non-red devices. Much of the increase in the nondiode arena was offset by an almost $5 million downward adjustment for diode lasers, which accounted for $0.8 million of revenues in 2001.

Once the semiconductor and telecom markets recover, which is expected to happen by the end of 2002, the trend identified last year—that these markets are easy targets for diode-laser test instrumentation—seems unchanged. Nondiode sales are projected to fall 1%, while diode-laser sales show an increase of more than 85%.

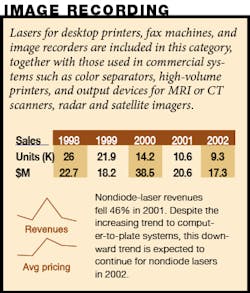

Image recording

While image recording saw a huge downturn in 2000 and early 2001, most of the major systems players in the market are re-engineering and retooling their print heads in favor of lasers, particular high-power infrared diode lasers and low-power violet-output diode lasers. Computer to plate (CTP) is starting to take over from conventional platemaking, which means more CTP systems in print shops and fewer color-separation systems in specialist trade shops. Market penetration is still fairly low, but growing rapidly. Digital workflows and the cost of plate materials are increasingly key factors in the market growth.

“Commercial printing has been a big market for lasers since the early 1980s,” says Ron Gibbs, an independent consultant and founder of Ron Gibbs Associates (Dunstable, England). “Much of the recent excitement among laser manufacturers is caused by the shift to different lasers.” For example, the number of argon-ion lasers supplied to the industry is decreasing while the number of laser diodes is increasing.

Our findings reflect this shift. While many laser firms see this market as a strong growth area in the coming year, our numbers reflect a decline in sales of nondiode-laser systems for these applications. The revised numbers for 2001 show a drop in nondiode unit sales, from 14,200 in 2000 to 11,600 in 2001. Revenues have also dropped off considerably, likely reflecting price-cutting in the face of increasing competition from diode-laser products.

This trend is expected to continue, Gibbs says, as digital printing threatens to replace offset litho and other conventional print presses. Some of these systems use lasers, while others use LED arrays. This technology is becoming more attractive as the print industry increasingly offers print on demand instead of large print runs, decreasing the number of print runs overall. We are forecasting unit sales of nondiode-laser systems to fall to just under 10,000 in 2002.

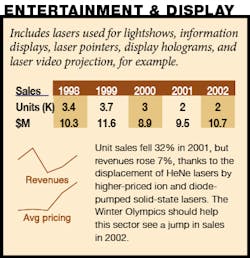

Entertainment and display

The economic downturn and the resulting decrease in disposable income have had a parallel effect on the travel and entertainment industries. Thus attendance at theme parks, casinos, museums, movies, sporting events, and other venues that typically feature laser light shows and displays has dropped dramatically—which has resulted in a tough year for the laser display business, according to David Lytle, editor of the Laserist, a monthly publication produced by the International Laser Display Association (Bradenton, FL).

Our numbers reflect this downturn, with unit sales dropping from 3000 in 2000 to 2000 in 2001. At the same time, revenues are on the rise. While sales of HeNe lasers have fallen off in this sector, the average selling price of other lasers in this market (primarily ion and diode-pumped solid-state lasers) has gone up.

Looking ahead, the entertainment market is expected to return slightly in 2002, thanks in part to the Winter Olympics in Salt Lake City and the many ancillary corporate events expected to be held there, according to Lytle. Our numbers show unit sales rising to 2100 in 2002, with a parallel increase in revenues to $11 million.

Lytle also points to some important technology trends that should further stimulate this market in the next year but will likely have a negative impact on the ion-laser market. A German company, Schneider Laser Technologies, has introduced the first high-power white-light solid-state laser system that simplifies the ability to do full-color laser displays and improves color balance. The solid-state design eliminates the need for large-frame ion lasers, replaces water-cooling with air-cooling, and plugs into a standard power outlet. Other companies are expected to follow Schneider’s lead and introduce their own white-light laser systems this year.

New software tools for creating laser animation are also expected to boost business in this market, along with a trend that is already a hit in European discos: audience scanning. Some U.S. companies are currently working to gain FDA clearance to overcome fears of eye safety and open up this market in the USA as well. Lytle sees these efforts coming to fruition in late 2002.

Other markets

Two of the largest laser markets, telecommunications and optical data storage, are primarily diode-laser applications and will be discussed in detail next month. Overall telecom laser revenues were projected to be almost $7 billion in 2001 last year, but are now at a mere shadow of that number ($2.5 billion), with 15% growth expected in 2002.

In optical memories, new formats continue to proliferate. Recordable DVDs have now made their debut, although they are still too expensive for most consumers and the choice of recorder is complicated by competing formats. The number of lasers involved was adjusted down for 2001 from 392 billion units to 356 billion and is projected to drop further into 2002; revenues however, are expected to grow about 6%.

While the downward trend for nondiode-laser sales in barcode scanning continues, diode-laser sales are remarkably resilient—revenues for 2001 were adjusted up 74% and are expected to gain another 29% in 2002. In the sensing market, nondiode-laser revenues remain fairly constant at about $15 million, but diode-laser sales were adjusted up by about $3.1 million for 2001 and are expected to gain a very healthy 92% in 2002.

Where the numbers come from

The Laser Focus World Annual Review and Forecast of the Laser Marketplace is based on a worldwide survey of laser producers and covers 27 types of lasers and 20 applications. Information about diode-laser markets is provided by Strategies Unlimited (Mountain View, CA). The review is the only major survey of its kind in this industry whose results are made public.

For many, both inside and outside the industry, from private-sector investors to foreign and US government bodies, this report is the only objective summary of major trends in our industry that is readily available. Part I takes a look at the overall market trends with more detail on nondiode lasers. Part II will be published in February and will cover the diode-laser marketplace.

Readers interested in the detailed results of both surveys will find them in the January 1 and February 1 editions of the Optoelectronics Report newsletter, published by Laser Focus World. A more extensive review of the data, with supporting commentary from market analysts, will be available to attendees at the Laser and Optoelectronics Marketplace seminar, held in conjunction with Photonics West (San Jose, CA) on January 21. For more information, see www.marketplaceseminar.com.

Collecting the data

We conducted our research and analysis for the Review and Forecast during October and November 2001. We asked manufacturers to provide an estimate of total worldwide market size (dollars and units) for 2001, based on year-to-date actual data, and a forecast for 2002. In addition to the information provided by the manufacturers, we also used data from other more narrowly focused market surveys, and we incorporated commentary provided by industry analysts who added insight into some of the markets.

Comparison with last year’s numbers

Readers who compare last year's 2001 estimates with this year's restated 2001 numbers will note differences and occasional discontinuities in the numbers reported as compared to last year. In general, no attempt has been made to explain these differences in detail. We request "bottom-up" market estimates, and the respondents to our survey do vary from year to year—both in terms of the companies involved and the individuals—so variations in the results are inevitable. In addition, changes in market visibility occur as market shares change. Differences in the overall numbers for 2001 last year and for 2001 this year may also reflect whatever degree of optimism or pessimism was inherent in last year's forecast (see Laser Focus World, January 2001, p. 88).—SGA