Laser Marketplace 2015: Lasers surround us in the Year of Light

International initiatives like IYL 2015, NPI, Horizon 2020, the BRAIN, and IP-IMI can only help reinforce what our industry already knows: Lasers play a significant role in our daily lives and will only become more prevalent as future applications emerge.

In our 2014 Annual Laser Market Review & Forecast, Laser Focus World and the photonics community overwhelmingly sang the praises of laser technology as an enabling medium that will “forge 21st century innovations” in materials processing, 3D printing, flow cytometry, smart sensing, display and cinema, molecular research, and biophotonics.

And while laser manufacturers may be happy with the mid-single-digit growth sales performance of the past few years, there is more cause for celebration. Lasers—once an inside secret (or more tritely, a solution looking for a problem)—literally surround us in our everyday lives and are finally being recognized globally and politically: first through the 50th Anniversary of the Laser events in 2010 and now through numerous global initiatives such as the United-Nations-decreed International Year of Light and Light-Based Technologies (IYL) in 2015.

"While many players in our industry may not appreciate the significance of IYL, this celebration is just one of many initiatives formulated in the past few years including the National Photonics Initiative [NPI], Photonics21, the BRAIN Initiative, and the Integrated Photonics Institute for Manufacturing Innovation [IP-IMI] that will raise critical awareness regarding the importance and relevance of photonics and lasers in our everyday society," says SPIE CEO and member of the IYL Steering Committee Eugene Arthurs.

"Once government officials, corporate leaders and the financial community begin to understand what photonics and lasers are and realize both the substantial direct economic impact and the leverage they bring, a 'laser-like stimulation' with 'amplification' of public and private funding opportunities will result," says Arthurs. "Increased awareness will reduce some of the mystique—and Star Wars mentality—and replace it with factual information about how laser technology can improve a company's bottom line."

"Over the past 25 years, I believed in and strongly promoted the benefits of laser welding for body-in-white and stamping assembly applications, to the point of 'nagging' high-level executives whenever I found an opportunity," says Mariana Forrest, founder and consultant at LasAp (Troy, MI) and previously senior manager of the Advanced Joining Technologies Development group at DaimlerChrysler (Auburn Hills, MI). "Fortunately, that uphill battle is over, and growing industry awareness of lasers and photonics in general, coupled with the decrease in laser source prices and increase in their reliability, changed the mentality of 'not on my watch,' leading to a rapid increase in various applications."

"Today, thanks to increased user confidence and proven economic feasibility, lasers are widely accepted as industrial 'tools of the trade' in high-volume automotive sheet metal applications and are now spreading out to other transportation sectors," adds Forrest. "I believe that if laser manufacturers continue to expend energy in growing social, industrial, and governmental awareness of laser technology, they will continue to grow and prosper."

The bottom line

Most of the major laser manufacturing companies are definitely experiencing prosperity, with laser sales certainly exceeding low-single-digit, gross-domestic-product (GDP) growth rates. TRUMPF (Ditzingen, Germany) revenues in the 2013/2014 fiscal year ending June 30, 2014 were up 10.4% to $3.42 billion from the previous year's $2.93 billion; of that total, the TRUMPF laser technology/electronics business division achieved sales of $1.05 billion—representing an approximate 30% of total sales—with 2588 employees.

"At nearly 11%, TRUMPF's growth rate was above the roughly 5–7% average for the laser industry," says Peter Leibinger, vice chairman of TRUMPF and president of its Laser Technology and Electronics Division. "There was notable development in products related to the automotive and machine tool industries, high demand for cutting hot formed parts, and an increase in laser welding applications in the automotive industry with the best performers being our TruDisk lasers and the TruLaser Cell 8030—a multi-axis laser system specifically designed for cutting hot-formed steel."

Han's Laser Technology's (Shenzhen, China) revenues rose markedly from nearly $480 million in 2010 to just more than $675 million in 2012. However, revenues flattened out in 2013 at $667 million and net income shrank due to a cost-of-goods-sold increase.

Newport Spectra-Physics (Irvine, CA) saw sales increase 5.2% over the nine-month period ended September 27, 2014 compared to the same period last year due to growth in the scientific research (10.6%), microelectronics (7%), life sciences (6.5%), and industrial manufacturing (7.7%) markets that buoyed a 15.9% decrease in the defense and security sector.

And then there was IPG Photonics (Oxford, MA), for which revenue grew 17% to $562.4 million for the nine months ended September 30, 2014 compared to the same period in 2013 with "strong sales across IPG's entire fiber laser portfolio."

While IPG's continued success is a testament to its ability to sell the value proposition behind fiber lasers, numerous other companies are benefiting from the fiber laser boom. But could the boom lead to a bust? "Our 2014 revenue will increase 30%, and we will ship two megawatts of pump diodes to the fiber laser market," says Louisa Chen, marketing director at BWT Beijing (China). "It seems everybody is jumping into the fiber laser market or building pump lasers by themselves without regard to cost structure or bottom-line financials. Just like fiber-laser-price pressures, our pump diodes are also facing significant price pressure over the past few years, and we are worried that the increasing entry of new fiber-laser-related suppliers for materials processing will eventually lead to a fiber laser bubble."

"While overall sales grew 30% in 2014 on strong direct-diode cladding and laser surface treatment as well as medical and aesthetic applications, our diode laser pump source sales for SSLs and fiber lasers actually declined a little due to strong price competition," says Focuslight Technologies (Xi'an, China) president Xingsheng (Victor) Liu.

Other winners in the pump laser market in 2014 include DILAS (Mainz, Germany). "Our 600 W/200 μm and 250 W/200 μm modules for fiber laser pumping, as well as pump laser diodes from 25 W to 2 kW—and especially narrow linewidth and wavelength-locked devices—are in high demand for disk laser and end-pumped lasers, in addition to high demand for our laser systems for direct-diode materials processing applications," says Joerg Neukum, DILAS sales and marketing director. "We also started shipping our fiber-coupled 25 W, 450 nm blue diodes for applications in phosphor excitation, cinema projectors, and photodynamic therapy applications."

Fiber laser boom/bust possibilities aside, did any of the major players in the laser industry have a down year? ROFIN-SINAR (Plymouth, MI) saw a 5% revenue decrease from $560 million in the 12 months ended September 30, 2013 to $530 million for the same period in 2014. "Compared to FY 2013, weaker business levels during the first half of the year—in single industries and specific regions such as China—were not fully compensated in the second half," says Gunther Braun, CEO and president at ROFIN-SINAR. "However, our business in China recovered well in the latter part of the year, Europe is on a solid level, and North American shipments have improved quarter by quarter. We are excited about the headway we have made in high-power fiber lasers and ultrashort pulse lasers as well as with the expansion of our applications portfolio through innovative processes like our new SmartCleave technology for the cutting of brittle materials."

Coherent's fiscal Q4 and year ended September 27, 2014 saw net sales of $794.6 million compared to $810.1 million for the same period in 2013, attributing the sales decrease to delays in the release of certain consumer electronics requiring sapphire materials processing as well as "shifting fortunes within the mobile display market."

Indeed, signals are mixed within the semiconductor/display industry about 2015 prospects. Despite IC Insights' 2014 microcontroller forecast for 5% growth after a flat 2013, Microchip (Chandler, AZ), a provider of microcontroller and analog semiconductors, predicts a semiconductor slowdown based on inventory buildups and weakness in China, calling itself a canary-in-the-coal-mine predictor based on its broad selling base of 80,000 customers. And the SEMI (San Jose, CA) Silicon Manufacturers Group (SMG) said that silicon wafer volume shipment growth, which reached a record level of more than 7.5 million inches in Q1-Q3 2014 (and 11% higher than the same period in 2013), plateaued in Q3 2014.

And yet, "We see semiconductor equipment billings growing globally about 19% for 2014 and we are looking at 15% for 2015," says Dan Tracy, senior market analyst at SEMI. "Despite the Microchip news, Intel had a record third quarter and Qualcomm reported that FY 2014 revenues were 7% higher than the previous year. A number of other industry analysts are discussing 8-10% revenue growth in 2014 and a similar range for 2015."

Strength in diversity

Those smaller and mid-sized companies that saw robust laser sales in 2014 share a common denominator: they have a diverse portfolio of cutting-edge-performance laser products and play in numerous industry sectors.

"For 2013 and 2014, we've seen overall growth of 15% each year, although we are planning for a more moderate growth scenario in 2015 due to political uncertainties," says Wilhelm Kaenders, president of ultrafast fiber and diode laser manufacturer TOPTICA Photonics (Munich, Germany and Rochester, NY). Kaenders notes a few recent breakthroughs: "Two cascaded second-harmonic-generation [SHG] stages convert our near-infrared diodes to deep-ultraviolet [DUV] 193 nm sources for semiconductor lithography applications that continue to demand shorter wavelengths with improved spectral and intensity stability, while our femtosecond "cold processing" fiber lasers continue to make gains against nanosecond lasers in microprocessing applications." He adds, "Our easy-to-operate multicolor solutions for biomedical instrumentation applications are a favorite among system integrators."

Kaenders says deployment of its 20+2 W guide star lasers confirms TOPTICA's commitment to the astronomical instrumentation community. He is also proud of the 90 dB signal-to-noise ratio of the company's terahertz radiation sources that extend layer thickness inspection parameters down to 20 μm in various materials science applications.

Laser diode and semiconductor optical amplifier (SOA) manufacturer Innolume (Dortmund, Germany) forecasts 2015 sales growth of between 25 to 30%, leveraging its product expertise in communications and medical markets. "Our biggest contributor to sales growth has been in medical applications, specifically, 1064 nm multimode laser chips for physiotherapy and a new biophotonic application for 2015 using tunable chips," says Innolume CEO Guido Vogel. "Having control over a vertically integrated laser diode manufacturing line from epitaxial growth to fiber coupling and supplying both quantum-dot and conventional quantum-well semiconductor laser chips and complete modules from 780–1320 nm positions us well for future growth. Our intense focus on sampling/prototyping activities with our customers over the past few years should bear fruit in 2015 and beyond."

In addition to biomedical instrumentation demand for chips and packaged devices, Vogel adds that data communications is an important future market for Innolume. "Our comb laser is a single-cavity DWDM [dense-wavelength division multiplexing] engine at 1310 nm able to power 8–16 channels of a datacom DWDM system and perfectly matches developments going on in the silicon photonics arena."

Gas lasers—in it for the long run?

One of the most popular articles on the Industrial Laser Solutions website in 2013 and 2014 was "Fiber versus CO2 laser cutting," wherein Bystronic (Coventry, England) GM David Larcombe explains the pros and cons of each type of laser—both of which are manufactured by Bystronic.

For typical 2 to 4 kW cutting applications, Larcombe showcased real-world cutting examples from subcontractor FC Laser (Ilkeston, England), thin-material (up to 2 mm) cutter Brattansound Engineering (Sutton, England), electrical-enclosure maker ICEE (Waterlooville, England), and 1.5–4.0 mm sheet-steel cutter WEC (Lancashire, England). The article concluded that fiber lasers—a better choice for subcontractors that cannot anticipate the material needs of their next customer-cut thin and reflective metal materials up to 4 mm typically 50% faster and with half the power consumption of CO2 lasers, which continue to excel in cut quality and speed for nonreflective, thick metals.

"It is the 50th anniversary of the CO2 laser and yet, surprisingly, sales continue to be strong even for U.S. manufacturers," says Ron Schaeffer, CEO of PhotoMachining (Pelham, NH). "Ironically, the fiber laser was invented at about the same time as the CO2 laser, yet it took many decades for the fiber laser to make its way into industry. However, despite the huge growth of the fiber laser market, the CO2 laser market still seems to be quite robust."

The Laser Product segment of GSI Group (GSIG; Bedford, MA)—the largest of its three segments—grew Q1 revenues 10% versus a year ago. "Our sealed CO2 laser product line had strong demand during the quarter, with sales increasing 15% versus Q1 a year ago," said GSIG CEO John Roush. "CO2 customers showed strong interest in some of our new products, including our mid-power pulsed P250 laser and our Flyer 3D marking head, which can be paired with our CO2 lasers ranging from 10 to 400 W."

"With emission in the 9 to 11 μm range, CO2 laser pulses are 10 times longer than visible-to near-IR fiber laser pulses," says Yong Zhang, CEO of Access Laser (Everett, WA). "Radiation from a CO2 laser is better absorbed by a different group of materials, including almost everything that looks transparent to the eye, white or near-white, and organic materials—a fundamental reason why the CO2 laser is not easily replaced in the market. While ultraviolet lasers can process many of these same materials, they are orders of magnitude more expensive than the CO2 laser."

Zhang also points out that the good old 10.6 μm standard is no longer enough and that commercial CO2 laser manufacturers now offer 9.3, 9.6, and 10.3 μm wavelengths that provide unique capabilities for different materials—enabling applications that give the CO2 laser new life for years to come.

Melles Griot (Carlsbad, CA), a unit of IDEX Corporation (Lake Forest, IL), says that He-Ne and Ar/Kr gas laser sales continue to decline in favor of diode-pumped solid-state [DPSS] laser options, but are stable for applications with critical performance parameters such as long coherence length and single-mode operation. "Gas laser products and the important customers that utilize them are critical to Melles Griot's future success and we will continue to over-serve them," says Rob Beeson, GM of the IOP Life Sciences and Medical Optics Business Unit of Melles Griot. For calendar Q3 2014, IDEX sales were up 9% (7% organically, 1% from acquisitions, and 1% from foreign currency translation) to $533 million, although sales in the laser segment were essentially flat.

The New Economy

First coined in a 1983 Time Magazine cover story, the phrase "The New Economy" describes the transition from a manufacturing-based society to a technology-driven, service-based economy. The story predicted very well how online retailing and advertising, crowdfunding/crowdsourcing, globalized/accessible medicine, sustainability and sharing/re-use services (car sharing/Netflix) would dramatically change the definition of "durable" goods (and logically pump up the associated laser sales for high-speed optical fiber communications networks).

While initially envisioned for the U.S. only, this New Economy now extends—in large part due to globalization and the Internet—to a worldwide stage. Fortunately, the New Economy is good for lasers: An article in the aptly named The New Economy magazine entitled, "JenLab's nanotechnology solutions speed up skin cancer detection," describes how the company JenLab (Jena, Germany) is using its femtosecond laser multiphoton tomograph technology to end the labor-intensive, time-consuming process of medical biopsy and replace it with rapid, real-time early skin cancer detection more accessible to the masses.

JenLab's patented 12 fs ultrashort-pulse lasers can also drill sub-100-nm-diameter holes in the surface of cells, allowing nanosurgical insertion of molecules into a cell's cytoplasm in a process called cell transfection. This process has immense implications for stem cell therapy and correspondingly high potential impact on the economy as these therapies could eliminate the high medical costs associated with many common, widespread diseases like diabetes—bringing disease prevention and cure to a higher percentage of the population.

According to the World Bank, health expenditures represented 17.9% of the U.S. GDP in 2012 compared to typical 10 to 11% figures in Europe and 4 to 5% figures in developing countries like China and India. And although projections that per-capita health expenditures are expected to outpace per-capita income globally well into 2050 are bad news for individual consumers, the news is good for laser manufacturers playing in the biophotonics sector.

So, besides the boost in medical and communications laser sales, how else might laser manufacturers benefit from the New Economy? In his book New Rules for the New Economy, Kevin Kelly describes how technology is transforming society. "The creations most in demand from the U.S. (those exported) lost 50% of their physical weight per dollar of value in only six years," says Kelly. "The disembodied world of computers, entertainment, and telecommunications is now an industry larger than any of the old giants of yore, such as construction, food products, or automobile manufacturing. This new information-based sector already occupies 15% of the total U.S. economy." As Kelly concludes, "The geography of wealth is being reshaped by our tools. We now live in a new economy created by shrinking computers and expanding communications."

Kelly's description of the modern farmer harkens back to the statements made in last year's laser market review by Karlheinz Gulden of II-VI (Saxonburg, PA) on the ubiquitous use of smart gadgets. Kelly alludes to the use of lasers in communications, sensing, and transportation applications when he writes: "A farmer in America—the hero of the agricultural economy—rides in a portable office on his tractor. It's air conditioned, has a phone, a satellite-driven GPS location device, and sophisticated sensors near the ground. At home, his computer is connected to the never-ending stream of weather data, the worldwide grain markets, his bank, moisture detectors in the soil, digitized maps, and his own spreadsheets of cash flow. Yes, he gets dirt under his fingernails, but his manual labor takes place in the context of a network economy."

Despite the fact that the Conference Board (New York, NY) Global Economic Outlook 2014 predicts that global economic growth in 2015 will hold at a rate of 3.4%, here's hoping that laser-based technologies will continue to command a larger and larger share of the New Economy as one of the key network "tools" that will reshape the aforementioned "geography of wealth" in favor of the laser manufacturer.

Why optimism?

According to an article in Quartz, which is "a digitally native news outlet, born in 2012, for business people in the new global economy," 2014 will see a surge in laser 3D printing system sales since certain key patents from 3D Systems (Rock Hill, SC) for laser sintering and stereolithography will expire, opening the market to new system players—especially Chinese companies. In May 2014, it was reported that the China 3D Printing Technology Industry Alliance will invest $33 million in 10 innovation centers for 3D printing technology in 10 different cities in China.

3D printing revenues continue to rise across the industry: 3D Systems' revenue was $466 million for the nine-month period ended September 30, 2014, compared to $358 million for the same period last year—a 30% increase. Voxeljet's (Friedberg, Germany) Q3 2014 3D printer systems' sales revenue grew 23.3%; and Optomec (Albuquerque, NM), a supplier of additive manufacturing systems for 3D printed metals and printed electronics (PE)—an emerging technology being fostered by organizations like the PE Test Center Network—more than doubled its order bookings through the first three quarters of 2014. Clearly, laser 3D printing is meeting the high expectations we set in our Laser Marketplace 2014 report.

And as if 3D Systems' own 3D printing systems' revenues weren't exciting enough, the company also acquired LayerWise (Leuven, Belgium) and its proprietary line of direct metal laser additive manufacturing (LAM) printers for aerospace, other high-precision metal components, and medical and dental customers. 3D Systems even expanded into 3D healthcare and personalized medical solutions capabilities with the August 2014 acquisition of Simbionix (Cleveland, OH), which specializes in FDA-cleared, 3D virtual-reality surgical simulation and training solutions.

Besides the 3D laser printing boom, if you believe that strength in mergers and acquisitions (M&A) activity is an economic indicator of future growth, take comfort in announcements by Mike Simon at OEM Capital (New York, NY) over the past year that show a steady increase in technology M&A activity: as of May 2014, technology M&A was up 10% over the prior year's period and more recently, as of October 2014, was up 19%.

In the laser sector, Oplink was acquired by Koch Industries in November 2014 for more than $400 million and will now be managed by Koch-acquired Molex (Lisle, IL) in a move that raises speculation about more optical communications component consolidation by traditional photonic and not-so-traditional investor groups and mega-sized private companies (like Koch) over the next few years.

Also in 2014, Laserage (Waukegan, IL) acquired the laser contract manufacturing business of Directed Light (San Jose, CA); ESI (Portland, OR) acquired Wuhan Topwin OE (Wuhan, China) to improve laser system sales locally within China; the Zemax division of Radiant Zemax (Redmond, WA) was acquired by Arlington Capital Partners (Washington, DC) in October 2014; Thorlabs (Newton, NJ) acquired the quantum cascade laser business of Corning (Corning, NY); NeoPhotonics (San Jose, CA) acquired the tunable laser product line of EMCORE (Albuquerque, NM) to expand its photonic integrated circuit (PIC) capabilities; and M/A-COM (Lowell, MA) acquired indium phosphide laser and silicon photonics solutions company BinOptics for $230 million.

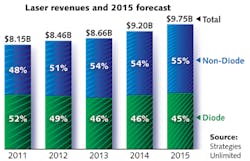

Compared to 2013, 2014 worldwide laser sales grew around 6% to $9.203 billion. Even with falling inflation leaving many economies in a holding pattern and continued weakness in the optical storage, military, and scientific R&D sectors, growing awareness of the laser industry and the bold future of emerging applications like 3D printing, smart gadgets in the New Economy, and improving M&A activity skew our laser forecast in the positive direction. For 2015, we forecast laser sales to grow 6% to $9.754 billion.

The Market Segments

The communications and optical storage segment remains the largest in the laser industry, followed by materials processing and lithography lasers. And for 2014, medical and aesthetic laser sales totals continued to be larger than the instrumentation and sensors category, followed by the scientific research and military category.

Communications and optical storage

Optical storage weakness continues to damper overall laser sales in the communications and optical storage sector; however, communications laser sales are vigorous. PIC-based communications network system provider Infinera calls it the "Terabit Era" and reported sales growth to $174 million in Q3 2014 compared to $142 million in the same quarter last year. And LightCounting (Eugene, OR) said that global sales of optical transceivers reached $1.1 billion in Q2 2014, the fifth consecutive quarter of growth.

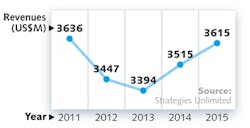

Communications and optical storage laser revenues reached $3.515 billion in 2014 and are forecast to grow around 2.8% to $3.615 billion in 2015. Despite glowing financials from most telecom laser providers in 2014, the Dell'Oro Group (Redwood City, CA) projects a telecom capital equipment expenditure drop in 2015, citing high mobile device penetration, slower mobile data growth, lack of new revenue streams, and increased competition from developed and undeveloped markets. This forecast, however, is quite perplexing considering how the optical communications industry is promoting the "Internet of Things" (IoT): the connection of equipment and devices to the cloud for the purpose of remote monitoring, diagnostics, and a whole host of yet-to-be-named "smart" applications.

"From networked systems utilized in railways and electric power grids to edge switches and client devices that connect assets like laptops, field devices and wireless access points, Cisco and Intel enable Predix [software] to be distributed to the edge, even in some of the most severe conditions," said Bill Ruh, VP of GE Software (San Ramon, CA), in a press release that describes how hardware and software mesh in an IoT world.

Cisco Systems (San Jose, CA) chairman and CEO John Chambers, in a keynote at the 2014 International Consumer Electronics Show (CES) in Las Vegas, reportedly "pegged the value of the evolving IoT" at $19 trillion, describing how IoT-based smart cities, for example, could see a direct return on investment through a smarter infrastructure. For quantitative backing, keynote guest speaker Antoni Vives, deputy mayor of Barcelona, Spain, said the city has saved $58 million a year using a smart water system, $37.5 million on smart lighting, and has increased parking revenue by one third through the use of smart parking meters.

Whether you call it the IoT or simply a world of "smart gadgets" that will convert the driver's seat of an automobile (or a farmer's tractor in the New Economy) into an Internet-connected data hub, it's fortunate that photonics—and yes, lasers—are the "fuel" for this information engine. Can you imagine how much faster the Internet will need to operate in order to seamlessly manage the 4.9 billion connected devices that Gartner (Stamford, CT) says will be in use in 2015—up 30% from 2014—and forecast to reach 25 billion devices by 2020?

Materials processing and lithography

Industrial laser systems in 2014 represented about 14% of global machine tool sales, so there is no question that the health of the world's manufacturing sector implies overall health for the industrial laser industry. Projections for 2014 machine tool consumption were in the 5–7% range, and the industrial laser systems market is expected to follow.

In the markets of interest to the industrial laser community, China's priority was to remake their economy with more domestic demand, less reliance on exports, and investments in capital-intensive state-owned companies. European manufacturing, in recession territory even with modest growth in Germany, started showing the first signs of recovery mid-year with slightly positive indications as the year ended. In North America, the U.S. was one of the "bright lights" with the economy on the mend, housing and non-residential strength growing into 2015, and an energy boom for at least the next three years. The BRIC nations that were projected to drive the 2014 industrial laser market underperformed with Russia and Brazil stagnant and China and India slowing down to 5–7% growth. And for 2015, the International Monetary Fund spotlighted the U.S., India, and the UK as the most likely positive growth regions, but cautioned about global capital investment increases.

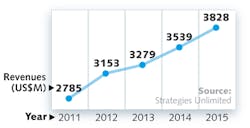

As 2014 ended, the total market for the industrial lasers that power the systems used in manufacturing operations exceeded $2.6 billion, a 6% increase over 2013 revenues (see table). In 2014, fiber lasers used in materials processing applications comprised 29% of the total revenues in the global laser market, trailing only lasers used in communications applications (32%). The vagaries of the world's manufacturing industries are thus closely followed by those who track lasers in photonics.

Clearly evident is the influence of the continued strong growth of fiber lasers, which increased their share of the total industrial laser market to 36% at the expense of solid-state and CO2 lasers. As the largest revenue-producing category, the fiber lasers sector is the most watched in the Industrial Laser Solutions annual market survey.

Fiber lasers used as the power source in metal cutting applications—especially sheet metal cutting, where systems are priced in excess of $650,000—will generate more than $1.3 billion of revenue in 2014. Adding in the revenue from high-power CO2 lasers in that same application (but rapidly losing market share to high-power fiber lasers) results in a capital equipment investment of almost $4 billion—about a third of all industrial laser systems sold in 2014.

Also notable in 2014 is the 13% share of the total market held mostly by high-power direct diodes. This relatively new-to-the market product is being used in on-line applications such as brazing the roofs and other sheet metal components on automobiles. Quietly, this highly efficient laser is carving out a niche in the market.

Not so quietly making a market entrance in 2014 is the high-brightness, high-power direct diode lasers that are being offered as an alternative to fiber lasers in sheet metal fabrication, with cutting results equal in quality and speed to equivalent-power fiber and disk lasers. Sales were miniscule, but interest was high at the fabricating shows in 2014.

As fiber lasers continue their relentless penetration into established markets such as marking, revenues from solid-state laser sales are decreasing. The $750+ million marking/engraving systems market is dominated by low-power fiber lasers in marking and sealed-off CO2 lasers in engraving. The latter employed in non-metal engraving are relatively secure from fiber laser penetration due to wavelength compatibility issues. Sustaining solid-state revenues is the rapid acceptance of ultrafast (or ultrashort-pulse) lasers operating in the megawatt-peak-power regime at pico- and femtosecond pulse widths focused on applications in micromaterials processing, for example, in processing components of smart phones and tablets—a market sector that seems to have an insatiable demand for high-selling-price precision equipment. Fiber lasers operating at very short pulse widths are competing for a share of this market, and some analysts speculate that microprocessing may be the next growth opportunity for these lasers. Some studies place the near-term ultrafast pulse laser market at as much as $450 million.

While on the subject of micromaterials processing, strong growth in the field of laser additive manufacturing (AM) has sparked increasing revenues for solid-state and fiber lasers. Wohlers Associates (Fort Collins, CO) says AM grew by more than 63% in 2013 with 37% of the revenues related to 3D and AM parts for final products rather than prototyping. In a survey of the aerospace supply industry regarding AM, 27% of the companies are already using it; 10% expect to use it next year; and 37% predict use in the next five years. As companies 'push the limits' of AM, laser-based processing will ride the growth wave.

Macromaterials processing applications other than laser cutting represent about 25% of the revenues for high-power lasers. Leading revenue growth at 10% were fiber and CO2 lasers used in welding applications, mainly in the automotive sector, and increasingly by Chinese auto makers. Fiber laser suppliers expect welding to be an expanding market for spot and remote operations in the coming years.

Summing up the 2014 markets for industrial lasers, marking grew 4%; micromaterials processing increased 14%; and macromaterials processing expanded 8%. Overall laser sales for materials processing grew 6%.

As cited earlier, the forecast for industrial lasers will follow the same modest growth trend as the global machine tool industry. After the G-20 Summit in Australia in November 2014, British Prime Minister David Cameron said, "Red lights are flashing for the world economy." The general consensus of industrial laser and systems suppliers interviewed is that 2015 will be a repeat of 2014 in terms of market growth, which is reflected in our projection of a 5% increase over 2014 revenues. This is consistent with many expert economic analysts' forecasts for a slowing international economy with lowering GDP for most of the advanced, expanding, and newly industrialized economies.

This growth will be led, again, by fiber lasers, but at a slightly lower rate than that of 2014. Fiber lasers are expected to continue eroding the market share of all CO2 and long-pulse solid-state lasers. Ultrafast pulse solid-state lasers should experience significant sales increases led by micromachining applications including AM. High-power laser applications in metal cutting will settle at a more consistent single-digit growth rate, but those lasers used for welding are expected to see double-digit growth beyond 2015.

Medical and aesthetic

Medical laser volume applications of significance are indicated by the following 2014 announcements: a milestone shipment of 2000 MxL series lasers (with wavelengths from 405 to 671 nm) by Changchun New Industries (CNI Laser; Changchun, China) for optogenetics applications; Coherent shipped its 2000th Chameleon-series laser for multiphoton microscopy applications; and Fianium (Southampton, England) shipped its 1000th supercontinuum laser with continually improving specifications optimized for use in ultrafast spectroscopy, near-field imaging, and microscopy.

"We will finish our fiscal year with 30% revenue growth in medical laser systems now that biomedical system integrators and pharmaceutical companies are looking for complete laser solutions rather than designing and building up from the component level," says Petteri Uusimaa, president and CEO of Modulight (Tampere, Finland). "By offering an end-to-end solution, we have signed several multiyear contracts and doubled our life science business in 2014."

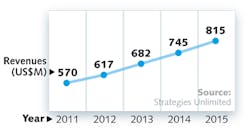

In 2014, surgical, ophthalmic, and cosmetic laser sales surged 13%, 9%, and 8%, respectively, bringing medical and aesthetic laser sales in 2014 to $745 million and are forecast to increase more than 9% to $815 million by 2015.

And although dental laser sales only increased 1% in 2014, ultrafast lasers could change that equation. "Energies are too high and laser-tissue interaction times are too long for today's Er:YAG and CO2 microsecond and short nanosecond pulsed dental lasers to provide both the thermal and stress confinement necessary to prevent microcracks, pre- and post-operative pain, and/or induction of cancer by ionization of water molecules in dental applications," says Anton Kasenbacher, a practicing dentist in Traunstein, Germany. "Ultrashort pulsed picosecond lasers achieve high ablation rates at high scan speeds with autofocus feedback, reducing the need, as an example, for intraoral suction and allowing therapy and diagnostic applications-theranostics-using a single system that delivers controlled biosafe nonlinear absorption of photons."

Kasenbacher says that the future sales potential for dental lasers is significant, considering that in 2011 there were an estimated 154,000 dental practices in the U.S. alone, generating nearly $108 billion in revenue.

In the laser aesthetics segment, Cynosure's (Westford, MA) Q3 2014 revenue was up 18% year-over-year to $71.5 million. While European revenue was up just 17% and U.S. revenue increased 17%, the largest increase came in at 46% from the Asia-Pacific region. The sales boost was primarily attributed to FDA and other governments' approval of Cynosure's PicoSure product for benign lesion, acne scarring, tattoo, and wrinkle removal.

Cutera's (Brisbane, CA) Q3 2014 revenue increased 11% to $18.7 million; Lumenis (Yokneam, Israel) reached Q3 2014 revenue of $74.2 million—9.4% higher than the same period last year; and Syneron-Candela's (Yokneam, Israel) Q3 2014 revenues were up 8.3% to $60.3 million. In all cases, the companies attributed the increases to FDA approval and strong market acceptance of laser-based therapies across the board. Beyond 2014, many of the companies are adding fat-removal laser technologies to their arsenal—a smart move that should solidify profitability in the laser aesthetics sector for years to come considering that an ABC News report estimates that the 108 million dieters in the U.S. alone are spending about $20 billion per year on weight-loss efforts.

Instrumentation and sensors

"Currently, super-resolution microscopy is the most vibrant sector in the laser instrumentation market," says Mike Tice, VP of consulting services at Strategic Directions International (SDi; Los Angeles, CA). "While laser scanning confocal microscopy has existed for decades, newer techniques invented over the past 10 to 15 years are now being vigorously commercialized, and the innovators of two particular techniques—stimulated emission depletion or STED and single-molecule microscopy—were recently awarded the Nobel Prize in Chemistry. Breaking the diffraction limit for optical microscopy, these and other super-resolution techniques known by a bevy of acronyms such as STORM, PALM, and SIM are furthering life science research." Tice adds, "The long-established LIBS [laser-induced breakdown spectroscopy] technique is also experiencing a renaissance, as next-generation systems provide better performance and a few vendors have configured LIBS into handheld instrumentation for wider applicability."

Besides microscopy and spectroscopy instrumentation, optical coherence tomography (OCT) systems continue to shrink in size as the applications base grows; in this case, OCT is moving beyond its roots in ophthalmology. In February 2014, Axsun Technologies (Billerica, MA), a wholly owned subsidiary of Volcano Corporation (San Diego, CA), received a volume purchase order for swept laser optical coherence tomography (OCT) engines from Michelson Diagnostics (Orpington, England) that will power Michelson's Vivosight Multi-Beam OCT system. Michelson says that Vivosight is the first OCT scanner to receive FDA 510(k) clearance for high-definition skin imaging that can reveal sub-surface tissue structure in the diagnosis, for example, of non-melanoma skin cancer.

In the sensing arena, IoT applications and smart gadgets should keep laser manufacturers busy for decades to come. In addition, laser sales are benefiting directly from the U.S. oil and gas boom. Of the $585 million spent on distributed fiber-optic sensors in 2013 (and forecast to reach $1.46 billion in 2018), 70% of the sales are associated with the oil and gas market segments, according to the July 2014 Photonic Sensor Consortium survey published by Information Gatekeepers (Boston, MA). In our forecast, the analytical, sensor, and life science instrumentation markets are expected to grow 7.5% to $662 million in 2015, easily surpassing the total laser sales for the combined scientific research and military market segments.

Scientific research and military

"Although a fragile global economic environment and an exchange-rate depreciation slowed growth from last year, we still saw a 30% increase in the sales of our DPSS and diode lasers for R&D applications including LIBS, Raman-based detection, spectroscopy, and particle image velocimetry [PIV] applications," says Tianhong Liu, sales manager at CNI Laser. "Established in 1996, our first lasers were used for low-end applications. Now, integrated pulse modulation and customized fiber-optic delivery options allow us to deliver lasers that meet the needs of the scientific and research community."

AdValue Photonics (Tucson, AZ) also sells primarily into scientific R& D markets and plans to grow its revenues by 30–50% in 2015. "While our continuous-wave fiber laser products are facing increased competition in this market, our pulsed 2 μm fiber laser offering was well received for applications in nonlinear optics and materials studies," says Katherine Liu, AdValue business development director.

Laser-matter interaction studies continue to drive numerous R&D laser sales. In February 2013, Lasertel (Tucson, AZ) was awarded a $5 million contract by Lawrence Livermore National Laboratory (Livermore, CA) to supply megawatt-class pump laser modules for the Extreme Light Infrastructure (ELI) Beamlines facility.

An analysis of U.S. federal procurement data by the 50-year-old Center for Strategic and International Studies (CSIS; Washington, DC) said that sequestration caused a 16% drop in Department of Defense (DoD) contracts during 2013 compared to 2012 and that of the contract spending categories, R&D took the biggest hit—falling 21%—with 2014 seeing a continuation in this decline.

Globally, however, the IHS Jane's Annual Defence Budgets Review says defense spending (heading upward for Russia, China, and India) in 2014 will grow 0.6% to $1.547 trillion and "drive the recovery projected from 2016 onward."

Of the $572 million that Strategies Unlimited has forecast for scientific R&D and military laser sales in 2015, Frost & Sullivan (San Antonio, TX) aerospace and defense senior industry analyst Brad Curran estimates a market value of ~$150 million each year for laser targeting designators and another $50 million or so for directed-energy weapons (DEWs), with Raytheon (Waltham, MA), Lockheed Martin (Bethesda, MD), and Boeing (Chicago, IL) leading this space.

Raytheon recently won an $11 million contract for a Humvee-mounted DEW and Boeing's thin-disk laser technology has officially achieved DEW status with its 30 kW output. Curran says that although the current market outlook is flat as the number of weapons platforms has been reduced, he sees great long-term potential for DEWs as military spending rises.

Entertainment and displays

In late 2013, Christie (Cypress, CA) was chosen to supply and install the world's first commercial digital laser projector at the Seattle Cinerama Theatre (although Moody Gardens in Galveston, TX said it was the first to install a Christie 6P laser projector for its D3D audience). Cinerama moviegoers attending the November 20, 2014 screening of "The Hunger Games: Mockingjay - Part I" were illuminated by the 4K, 60,000 lumen, 6P dual-head projector and tweeted various accolades, although most of them commented on the beer and chocolate popcorn rather than picture quality. Nonetheless, sessions such as "The Digital Cinema Laser Battle" at InfoComm 2014 saw nothing but future growth in this lumen-rich, high-reliability, low-consumable-cost, and energy efficient laser entertainment industry.

"This was a very exciting year for lasers," says Greg Niven, Necsel (Milpitas, CA) VP of sales and marketing and chair of the Laser Illuminated Projector Association (LIPA; San Jose, CA). "It's not often that we get to witness the launch of a completely new market segment that will literally get millions of eyeballs seeing high-power visible lasers via both large-venue cinema projectors and low-lumen office data projectors. This is just the beginning of a variety of new laser-based lighting applications."

So after you leave your laser cinema experience, how about heading south to Shoreline, WA to the headquarters of Laser Tag Live, or "paintball without the projectile"? This company brings the laser game to your location for $15 per gamer per hour and $1.12 per mile from their location to yours. Their metal laser guns—with "sound effects that are so realistic you will hear the shells hitting the floor"—use infrared lasers and sensors to indicate when a player has been "tagged," and some use visible lasers (limited to low-power CW typically red or green visible laser pointers used in indoor forums only) for the visual/firing effect.

As laser cinema continues its penetration and laser tag arenas multiply, laser light show revenues continue their solid growth. In fact, many municipalities are considering "snuffing out" their polluting, solid-waste-generating fireworks displays in favor of laser light shows. With all the laser fun to be had, we forecast laser sales for entertainment and display applications to grow nearly 11% to $197 million in 2015.

Image recording

From 2013 to 2018, CCS Insight (Slough, England) says printer shipments will increase from 106 million to 124 million units (compound annual growth rate of 3.1%), with 50% of those printers being multifunction inkjet varieties. The fastest-growing printer type is laser multifunction units, rising to 30 million (comprising nearly 25% of all printer units shipped) by 2018.

Despite the increase in shipments, printer values continue to decline, and stiff price competition erodes the enthusiasm. For 2015, we forecast lasers used for image recording applications to drop slightly from $67 million in 2014 to $66 million.

Communications & optical storage

Includes all laser diodes used in telecommunications, data communications, and optical storage applications, including pumps for optical amplifiers.

While 2013 and 2014 were relatively strong in the communications sector, there are signs that 2015 may be a bit slower. 100G has been the jumping point these last two years, driven in large part by wireless operators building up their backbones. Driving this on the device side, LTE and Wi-Fi networks continue to be deployed, and data traffic continues to grow.

Prospects remain dim for optical storage. Streamed movies and music continues to grow in popularity, and solid-state memory prices continue to drop. Heat-assisted magnetic recording ("HAMR") or using lasers to increase storage capacity of magnetic media may have some commercial products by 2016 or 2017, but with the growing use of Cloud services by consumers, it is likely HAMR will only find use in some very specific niche server farm applications.

Materials processing & lithography

Includes lasers used for all types of metal processing (welding, cutting, annealing, drilling); semiconductor and microelectronics manufacturing (lithography, scribing, defect repair, via drilling); marking of all materials; and other materials processing (such as cutting and welding organics, rapid prototyping, micromachining, and grating manufacture). Also includes lasers for lithography.

Lasers for industrial use had a strong year in 2014, helped both by an improving economy in most regions of the world, especially in Europe, and increased adoption of laser technology in more manufacturing processes, including additive manufacturing. While metal welding and cutting were strong, some segments like solar were particularly weak, while smartphones and flat panel displays—large contributors to lasers in past years—have become close to flat.

Demand for semiconductors was strong in 2014, with the SIA reporting that worldwide semiconductor sales were up around 7% over 2013. This increased demand for semiconductors has increased demand for excimer lasers and supplies. Extreme UV photolithography continues to evolve and improve, but is nowhere near the point where it is taking away any demand for deep-UV excimer lasers.

Medical & aesthetic

Includes all lasers used for ophthalmology (including refractive surgery and photocoagulation), surgical, dental, therapeutic, skin, hair, and other cosmetic applications.

The pressure on the medical profession to cut costs and improve outcomes will benefit the use of lasers in the long term, but the high costs of lasers have posed a short-term problem. Still, 2014 was a strong year for most medical lasers, with the exception of lasers used for dental applications. Ophthalmic and cosmetic lasers make up the majority of the medical laser revenue, and both grew in revenue in excess of 8% in 2014.

While medical lasers have long played an important role in the developed world, a fast-growing middle class in the developing world accounts for a large and growing portion of total medical laser revenues. In fact, in some areas, medical lasers in developing countries are used for a wider range of medical applications than in developed countries due to the peculiarly long and expensive approval process (and export limitations) that developed countries place on laser technology.

Instrumentation & sensors

Includes lasers used within biomedical instruments; analytical instruments (such as spectroscopy); wafer and mask inspection, metrology, levelers, optical mice, gesture recognition, LIDAR, barcode readers, and other sensors.

Laser instruments and sensors include a variety of applications that have become increasingly important in recent years. From lasers used in LIDAR for self-driving cars, to lasers for flow cytometry and ultrafast spectroscopy for medical applications, the increasing processing power of today's microprocessors increasingly needs better sensors to supply data to be processed. When considering that laser revenue in this segment grew more than 12% in 2014, consider also that lasers used in this segment are also dropping fairly rapidly in price, which masks some of the real segment growth.

While some applications within this segment are flat or dropping in demand, such as lasers for barcode readers and laser PC mice, many others, such as gesture recognition for smartphones, are only in their infancy and could eventually amount to applications consuming millions of dollars of lasers. Overall, this is the segment to watch for some of the newest and most innovative laser applications.

Scientific research and military

Includes lasers used for fundamental research and development, such as by universities and national laboratories, and new and existing military applications, such as rangefinders, illuminators, infrared countermeasures, and directed-energy weapons research.

Spending on lasers for scientific research has recovered somewhat as compared to a disastrous 2013, when the U.S. government's closing in addition to the Sequester sharply decreased new laser sales. Since then, conditions are returning to the "new normal" in the U.S., while research spending continues to grow in many countries, especially in Asia and including China.

Military spending in the U.S. has been dropping since it peaked at around $851 billion in 2010. The good news for lasers is that they have been grabbing an increasing slice, albeit small, of the military budget pie. This is true in other regions as well, including Asia and Europe. Lasers, which require no ammunition to be restocked, are seen as a good solution to the growing problem of drones, pirates, and other smaller targets that have increasingly appeared in the last few years.

Entertainment & displays

Includes lasers used for light shows, games, digital cinema, front and rear projectors, picoprojectors, and laser pointers.

The majority of laser revenue in this segment is for laser light shows, and this business has been booming the last few years. Faster galvanometers, lower-cost diode lasers in a multitude of colors, and better safety measures have made laser light show hardware available to more applications at much lower costs.

Outside of light shows, a few other laser display applications are just in their infancy. Laser light sources for movie projection are just now becoming commercially available, and many laser-powered theaters are set to open this year. For business projectors and even some residential high-end projection TVs, lasers have been used for several years now. Although small, laser usage is growing.

Image recording & printing

This category includes lasers for commercial pre-press systems and photofinishing, as well as conventional laser printers for consumer and commercial applications.

Sales of diode lasers used in commercial printing are in decline. The creation of application stores and audio and video streaming to the Cloud have largely reduced the need for physical image storage. Printing for consumer packaging requirements continues to keep this segment afloat, although not thriving.

For more in-depth analysis

Much more detail on the laser markets is available from Strategies Unlimited in its report, "Worldwide Market for Lasers 2014" (www.strategies-u.com). Details include forecasts to 2017 of laser units, average prices, and revenues by segment, estimates of market share, and discussion of the dynamics within each laser segment. The report is the only comprehensive report on the laser market and the 12th in a series that includes fiber lasers and industrial lasers. Special topics reports in the series cover mid-infrared lasers and ultrafast lasers.

Strategies Unlimited specializes in photonics markets, including lasers, LEDs and lighting, and imaging. It was founded in 1979 and is located in Mountain View, CA. Strategies Unlimited is one of PennWell's many brands, which also include Laser Focus World, Industrial Laser Solutions, BioOptics World, Vision Systems Design, LEDs Magazine, and Lightwave.

About the numbers

The estimates and forecasts of laser shipments were based on both supply and demand side analyses by Strategies Unlimited, a PennWell business. Strategies Unlimited has been conducting market research in photonics products for more than 30 years, with specialties in lasers and high-brightness LEDs. The effort considered both quarterly trends and long-term historical trends; results were then compared and adjusted to correct for known errors. More information will be available from Strategies Unlimited and at the Lasers & Photonics Marketplace Seminar held in conjunction with SPIE Photonics West in San Francisco on Monday, February 9, 2015.

About the Author

Gail Overton

Senior Editor (2004-2020)

Gail has more than 30 years of engineering, marketing, product management, and editorial experience in the photonics and optical communications industry. Before joining the staff at Laser Focus World in 2004, she held many product management and product marketing roles in the fiber-optics industry, most notably at Hughes (El Segundo, CA), GTE Labs (Waltham, MA), Corning (Corning, NY), Photon Kinetics (Beaverton, OR), and Newport Corporation (Irvine, CA). During her marketing career, Gail published articles in WDM Solutions and Sensors magazine and traveled internationally to conduct product and sales training. Gail received her BS degree in physics, with an emphasis in optics, from San Diego State University in San Diego, CA in May 1986.

Allen Nogee

President, Laser Markets Research

Allen Nogee has over 30 years' experience in the electronics and technology industry including almost 20 years in technology market research. He has held design-engineering positions at MCI Communications, GTE, and General Electric, and senior research positions at In-Stat, NPD Group, and Strategies Unlimited.

Nogee has become a well-known and respected analyst in the area of lasers and laser applications, with his research and forecasts appearing in publications such as Laser Focus World, Industrial Laser Solutions, Optics.org, and Laser Institute of America. He has also been invited to speak at conferences such as the Conference on Lasers and Electro-Optics (CLEO), Laser Focus World's Lasers & Photonics Marketplace Seminar, the European Photonics Industry Consortium Executive Laser Meeting, and SPIE Photonics West.

Nogee has a Bachelor's degree in Electrical Engineering Technology from the Rochester Institute of Technology, and a Master's of Business Administration from Arizona State University.

Conard Holton

Conard Holton has 25 years of science and technology editing and writing experience. He was formerly a staff member and consultant for government agencies such as the New York State Energy Research and Development Authority and the International Atomic Energy Agency, and engineering companies such as Bechtel. He joined Laser Focus World in 1997 as senior editor, becoming editor in chief of WDM Solutions, which he founded in 1999. In 2003 he joined Vision Systems Design as editor in chief, while continuing as contributing editor at Laser Focus World. Conard became editor in chief of Laser Focus World in August 2011, a role in which he served through August 2018. He then served as Editor at Large for Laser Focus World and Co-Chair of the Lasers & Photonics Marketplace Seminar from August 2018 through January 2022. He received his B.A. from the University of Pennsylvania, with additional studies at the Colorado School of Mines and Medill School of Journalism at Northwestern University.

David Belforte

Contributing Editor

David Belforte (1932-2023) was an internationally recognized authority on industrial laser materials processing and had been actively involved in this technology for more than 50 years. His consulting business, Belforte Associates, served clients interested in advanced manufacturing applications. David held degrees in Chemistry and Production Technology from Northeastern University (Boston, MA). As a researcher, he conducted basic studies in material synthesis for high-temperature applications and held increasingly important positions with companies involved with high-technology materials processing. He co-founded a company that introduced several firsts in advanced welding technology and equipment. David's career in lasers started with the commercialization of the first industrial solid-state laser and a compact CO2 laser for sheet-metal cutting. For several years, he led the development of very high power CO2 lasers for welding and surface treating applications. In addition to consulting, David was the Founder and Editor-in-Chief of Industrial Laser Solutions magazine (1986-2022) and contributed to other laser publications, including Laser Focus World. He retired from Laser Focus World in late June 2022.