LASER MARKETPLACE 2006: Diode doldrums

Robert V. Steele

Although several segments posted gains, particularly telecom and high-power applications, price erosion restrained revenue growth for the optical-storage segment.

The Laser Focus World 2006 Annual Review and Forecast of the Laser Marketplace is conducted in conjunction with Strategies Unlimited, (SU; Mountain View, CA; a Pennwell Company). Part II covers the diode-laser marketplace. Part I, which reported on nondiode-laser markets, appeared last month.

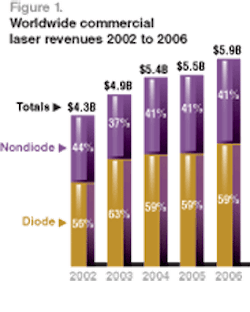

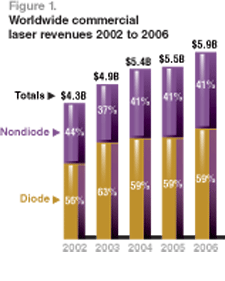

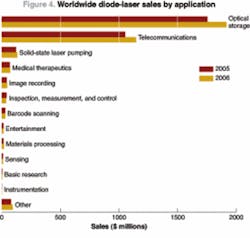

After two years of growth ranging from robust to modest, the diode-laser market was basically flat in 2005. Sales revenue for diode lasers was $3.23 billion compared to $3.20 billion in 2004, and continues to represent 59% of total commercial laser revenues (see Fig. 1). Although revenue growth was realized in several segments, such as telecom and various high-power applications, revenue declined in the optical-storage segment, which accounts for 54% of the diode-laser market. The decline in revenue was due to an across-the-board decrease in average selling prices, which offset an increase in unit shipments. The value of the Japanese yen, which has a significant impact on dollar-denominated revenue figures (due to the high percentage of optical storage lasers produced in Japan), was relatively stable at 110 yen per U.S. dollar in 2005 compared to 108 in 2004.

For the past several years, a persistent limiting factor in revenue growth has been the decline in prices, which may be moderating somewhat, at least for telecom lasers as discussed below. For optical-storage lasers, many of which have become commodity products, price erosion is likely to continue to restrain revenue growth until the next generation of optical-storage drives (such as HD-DVD and Blu-ray Disc) begin to have an impact on the market.

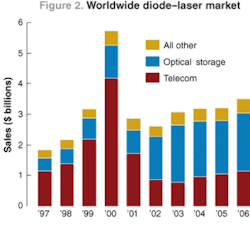

Since the bottoming of the diode-laser market in 2002, growth has been driven primarily by optical storage. However, in 2004 the telecom laser market started to recover, which contributed to the modest growth of the overall market in the past two years, and prevented the market in 2005 from declining. The average market growth rate from 1996 to 2005 was approximately 8.1% per year (see Fig. 2).

For 2006, moderate growth is projected for all applications, including telecom. All segments are forecast to grow in a relatively narrow range, from 7.8% to 9.3%. Overall, the diode-laser market is forecast to grow 9% to $3.52 billion in 2006.

Optical storage

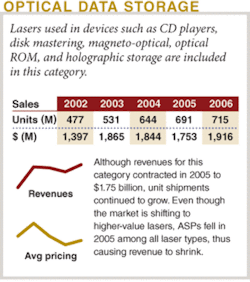

The market for diode lasers used in optical storage continued to grow on a unit basis, but the market for the current generation of CD- and DVD-based technologies is becoming rather mature. Unit shipments of diode lasers in 2005 were 691 million, a modest 7.3% increase over the 644 million units shipped in 2004. Because of the declines in average selling prices (ASPs) noted above revenue declined from $1.84 billion to $1.75 billion. As in the past few years, most of the growth came from DVD-based drives. Unit shipments of visible diode lasers (650-660 nm) for DVD players, DVD-ROM drives and the several varieties of recordable DVD drives increased from 275 million to 311 million. Revenues for these products increased from $927 million to $1.02 billion. On the other hand, 780-nm lasers for CD players, CD-ROMs, and recordable CD drives only showed a slight increase, from 369 million to 380 million. Declining ASPs for these products resulted in a revenue decrease to $739 million from $917 million.

The diode-laser market for optical storage is quite complicated, involving a mix of 780-nm and 650-660-nm lasers for read-only and recordable applications involving CD-type media and DVD-type media, respectively. Each DVD-type player or drive includes a 780-nm laser as well as a 650-660-nm laser to allow it to be back-compatible with CD-type media. Some lasers are sold on a stand-alone basis, while others are sold as integrated pick-ups that include detectors and optics. In recent years dual-wavelength lasers (produced by Matsushita, Toshiba, Rohm, Sharp, and Sony) have become increasingly important in DVD read-only drives. Each dual-wavelength laser replaces a 780‑nm laser plus a 650-nm laser, thus reducing overall unit growth for 780‑nm lasers. Over time, the market is gradually shifting to higher-value products, including the lasers for recordable drives and dual-wavelength lasers. This shift contributes to revenue growth, and explains why the market did not shrink further in 2005 as prices dropped across all categories.

As the market for CD- and DVD-based optical-storage products matures, the industry is actively promoting the next generation of high-density optical drives using blue-violet (405‑nm) diode lasers. These drives will have storage capacity of up to 27 Gbytes per disk, compared to 4.7 Gbytes for DVD. Most of the major optical-storage-drive manufacturers are developing next-generation DVD products, and several have already introduced products to the market, including Sony in April 2003, and Matsushita later in 2003. These products, which are recordable drives, have been available only in Japan, and because of their high prices (around $3000 to $4000) sales to date have been modest, on the order of thousands. In addition, several companies have shown prototypes of high-density recorders at various electronics trade shows such as CEATEC in Japan and the Consumer Electronics Show in the U.S.A. Companies that have shown prototypes include Hitachi, JVC, Mitsubishi, Panasonic (Matsushita), Philips, Pioneer, Samsung, Sharp, Sony, and Zenith.

Complicating the picture for the development of the next-generation optical-storage market is the existence of two competing formats. One format, supported by Sony and an alliance of consumer electronics and media companies (including Dell, Hewlett-Packard, Hitachi, LG Electronics, Matsushita Electric, Mitsubishi Electric, Pioneer, Royal Philips Electronics, Samsung Electronics, Sharp, TDK, Thomson, and 20th Century Fox), is known as the Blu-ray Disc format. The other format, developed by Toshiba and NEC, and supported by Sanyo, Universal Studios, Warner Brothers, New Line Cinema, and Paramount, is known as HD-DVD (for high-density DVD). While both formats make use of a 405-nm diode laser to read and write data, the disc structures are completely different, and thus the formats are incompatible. This development is reminiscent of the VHS-Betamax “wars” associated with the introduction of the VCR in the early 1980s, and the competing DVD formats of the late 1990s. While a compromise was reached eventually regarding the DVD read-only format, multiple versions of the DVD recordable format still exist (DVD-RAM, DVD+RW, DVD-RW, and so on).

Throughout 2005 there were discussions between Sony and Toshiba to try to strike a compromise between the competing HD-DVD and Blu-ray Disc formats. These discussions were ultimately unsuccessful, so entering 2006 both companies plan to move into the market with competing technologies. Major rollouts are expected for both camps’ next-generation DVD players in early-to-mid 2006, and Sony plans to introduce the PlayStation 3, based on its Blu-ray Disc technology, in the same time frame. Based on the most recent developments in entertainment and computer industry support, most industry observers believe Blu-ray Disc technology, with its higher storage capacity, will be the market leader.

Because general commercial release of Blu-ray Disc or HD-DVD drives has been delayed until 2006, 405-nm diode lasers have had relatively little impact on the optical-storage market through 2005. In 2005, several tens of thousands of 405-nm diode lasers were sold for optical-storage applications, resulting in revenue of just over $5 million. Many of these were for development, test, and demonstration, with a fraction used in the very limited commercial market. In 2006, when the first significant commercial shipments of next-generation optical-storage drives are expected, shipments of more than 100,000 units are expected, with a market size of approximately $17 million, still just a small percentage of the projected $1.92 billion total market for optical-storage lasers.

Telecommunications

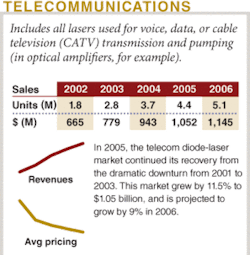

Revenues for lasers used in telecommunications grew for a second year, reaching $1.05 billion in 2005, compared to $0.94 billion in 2004. Despite this growth, many leading suppliers are still operating with net losses. There is still excessive manufacturing capacity worldwide, even with the downsizing that has already occurred within companies, and few companies have left the market or merged. Prices continue to fall, although the decline slowed in 2005. If 2006 turns out to be the year that a major supplier withdraws from the market, prices could stabilize and this sector would see stronger revenue growth. All of the major suppliers expect to be making a net profit in 2006, as more functions are moved offshore and redundant operations are closed. Continuing moderate growth is forecast, with revenue of $1.14 billion projected for 2006, an increase of 8.9% over 2005.

The strongest growth was in tunable lasers, pump lasers for optical amplifiers, and fiber-to-the-home (FTTH) modules. Long-haul customers are now adopting tunable lasers that operate over the entire DWDM band because of the advantages they offer for inventory control. Santur now remains the only independent tunable-laser supplier, with the others having their own capability, or buying parts from Santur.

Pump and amplifier sales surged in 2005, with unit sales resembling that of the peak of the boom, but there is little visibility in this area. Sales in 2006 may continue to be greater than 2004, but without repeating the volume of 2005. Pump prices are a fraction of the boom years, but have stabilized now that there are just three main suppliers: Bookham and JDS Uniphase in 980-nm pumps, and Furukawa Electric in 14xx-nm-range pumps. The undersea market is still slow, but some new builds are expected, providing some opportunity for the suppliers that are qualified to supply into that market.

Fiber to the home (FTTH) continues to draw the most attention. The lasers are used in two-wavelength and three-wavelength diplexers and triplexers, depending on the architecture. The unit price of these lasers is very low, but the volumes are ramping up as carriers finally follow through on years of expectations.

High-power diode-laser applications

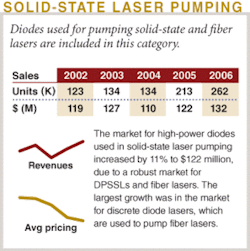

The overall market for high-power diode lasers (comprising 750-980 nm, 100 mW-10 W; 750-980 nm, >10 W; and Stacks categories in Tables 1 and 2), excluding telecom pump lasers, experienced reasonably good growth (12.7%) in 2005, reaching $249 million. Generally speaking, growth was across the board, encompassing all the major high-power diode applications. The largest application continued to be pumps for solid-state and fiber lasers, which accounted for 49% of the total, or $122 million. This category benefited from the robust markets for diode-pumped solid-state lasers and fiber lasers, as noted last month (see www.laserfocusworld.com/articles/245112). The market for discrete diode lasers (100 mW-10 W), which are the principal pump sources for fiber lasers, grew by 16.1% to $36.1 million. The market for diode-laser “bars” (>10 W) used primarily for pumping solid-state lasers, grew just slightly less, increasing by 13.3% to $40.5 million.

The medical market for high-power diode lasers continued to benefit from the popularity of handheld hair-removal products. While the market for diode-laser stacks used in large, stationary diode-based hair removal systems declined slightly, diodes for handheld products were the largest growth category, increasing by 30% to $42.7 million. Other medical applications, such as surgical and ophthalmic were relatively flat. The total medical market for high-power diodes was $68 million, an increase of about 10% over 2004.

An application that has traditionally been small in size showed outstanding growth in 2005-the market for high-power diode lasers used in materials processing applications nearly doubled to $14.3 million. The reasons for this growth are not totally clear. The reported market size for this application has varied widely from year to year, as is often the case for smaller applications to which many survey respondents have little exposure. Nevertheless, the magnitude of this increase may well mean that diode lasers are finally getting traction in an application area that has long held out promise for a substantial market, but for which the market reality has always been disappointing. Growth was observed for diode “bars” as well as stacks. The former are used in lower-power applications such as brazing, microwelding, and plastics welding, while the latter are used in kilowatt-scale applications such as welding and heat-treating.

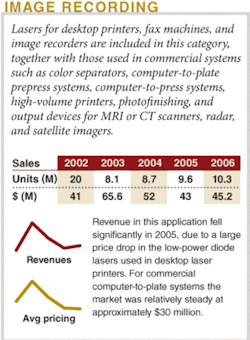

The overall commercial printing and graphic arts (image recording) market was flat in 2005 at about $29 million, as predicted in last year’s forecast for 2005. There are two elements of this market-high-power discrete diodes and “bars,” and visible (<700 nm) diodes. The former are used in computer-to-plate (CTP) applications, while the latter are used in CTP (violet lasers), as well as in various other applications such as photofinishing and digital film writing (red lasers). High-power diodes continue to make up the bulk of the market (85%); however, the market for these devices decreased slightly in 2005, while the visible-diode market increased slightly. Violet diodes are continuing to make some inroads into CTP applications, taking market share from high-power diodes, especially in the smaller-format presses, because violet-diode-based CTP systems have a lower first cost, even though substantial post-processing of the photosensitive plates is required.Other applications

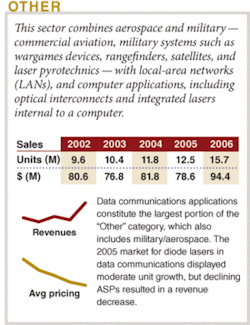

The applications discussed above account for the vast majority (95%) of the diode-laser market, with a variety of smaller applications making up the remaining 5%. These include applications such as local-area networks, or LANs (includes storage-area networks, or SANs), military/aerospace, sensing, entertainment, and inspection, measurement, and control. Of these, the largest market is LANs and SANs (with is included within the “Other” category in Tables 1 and 2) at $64 million in 2005. This application uses both 850-nm VCSELs and 1300-nm Fabry-Perot lasers in short-to-medium-range fiberoptic transceivers. After bottoming out during the technology recession of 2001, the LAN/SAN market has made a consistent recovery as companies have increased investments in their computing and network infrastructures. However, even though the use of VCSELs and 1300-nm lasers in this application increased modestly (nearly 7%) in unit terms in 2005, revenues fell slightly due to price erosion.❏

ROBERT V. STEELE is director of optoelectronics at Strategies Unlimited, 201 San Antonio Circle, Suite 205, Mountain View, CA 94040; e-mail: [email protected].

Presenting the data

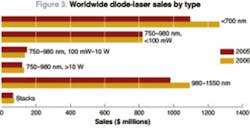

Diode-lasers sales data for 2005 and forecast for 2006 are charted in detail by type and by application in Figures 3 and 4, respectively. Diode-laser sales data by unit shipment and dollar revenues are shown in Tables 1 and 2. For an explanation of our methods, see “Where the numbers come from” on p. 77.

The data presented in the tables here are available with additional commentary in the Feb. 1 issue of Optoelectronics Report (see www.optoelectronicsreport.com)

Diode-laser products and configurations

The diode-laser revenue figures shown in Table 2 are based on the unit sales figures in Table 1 and average selling prices (ASPs) for each type of diode laser. Average selling process for diode lasers vary widely and are a function of wavelength, power output, and package type. The revenue figures are for packaged devices as they are sold by diode-laser suppliers to the merchant market or transferred internally to other company divisions to be used in system-level products. Diode-laser packaging is subject to a wide range of configurations according to the device type and application requirements, and includes variations such as thermal control and fiber coupling. Short-wavelength (<1000 nm) diode lasers at power levels less than 200 mW are almost always single-lateral-mode, single-stripe devices that are sold commercially in hermetically sealed TO-type packages. The lasers are typically mounted on a heat sink, and the complete package includes a back facet photodetector for monitoring the laser output level. The selling prices of such devices range from well under $1 for a high-volume CD-type laser to around $1.10 for a low-power visible (650 nm) laser to around $5 for a 50-100 mW, 660-nm laser used in rewritable DVD applications. Some low-volume specialty devices can be priced much higher.

An increasingly important packaging concept in the low-power diode-laser market, originating in audio CD and CD-ROM applications that use 780-nm laser diodes, but now used widely in DVD applications that use 650-nm laser diodes, is to carry out hybrid integration of the diode-laser chip, detector chips, and optical elements in a single package. These integrated optical pickups are lower in cost than pickups fabricated from discrete components, and result in easier assembly for the optical-disk-drive manufacturer. This concept was introduced by Sony in 1991 for its very thin (15 mm) Walkman CD player. Such pickups are now manufactured in volume by Sony, Sharp, and Matsushita, with prices around $1.50 (780 nm) to $2.50 (650 nm), compared to much less than $1 to $1.10 for discrete packaged diode lasers. The value of such pickups is included in the diode-laser market units and revenues in Tables 1 and 2. The concept of integration has also extended to combining 780- and 650-nm lasers in a single package. These are used in DVD players and DVD-ROM drives so that CD-type media can be read in the same drives. This type of integrated package, which is priced at around $3, is included in the statistics on lasers in the <700-nm category in Tables 1 and 2.

For high-power diode lasers (>1 W) there is a wide range of power levels and configurations. Up to 5-W CW, a wide (up to 500 µm) single-stripe, multimode device is the norm. These devices are usually supplied in TO-type packages that can include Peltier coolers for temperature control. Beyond about 5 W, the only commonly used approach is a multistripe, multimode array. The standard product at these power levels is a 1-cm-wide diode-laser bar, which consists of a single multistripe array or a grouping of several arrays to build up higher power levels. Pricing for high-power diode lasers ranges from under $200 for a 1-W discrete device in quantity up to $2000 for a 50-W bar. Single laser bars are now available at power outputs up to 60-W CW, although 50 W is still the most common configuration. Increasingly, these high-power devices are sold with fiber coupling to provide a more usable output beam for the end user. Higher-power arrays are typically available on a heatsink submount that can be attached to a water-cooled heat-removal system. For applications requiring high peak power, these arrays can be operated in the pulsed (quasi-CW, or QCW) mode at peak powers up to 100 W.

For power levels above 60-W CW, high-power diode-laser bars can be stacked in the vertical dimension (these products are included in the Stacks category in Tables 1 and 2). Because of the difficulty in removing heat from such a configuration, these stacks are typically operated in the QCW mode. Peak output power approaching 5 kW can be achieved from such a stack. The packages for these devices typically include water cooling, although conduction cooling can be used in lower-duty-cycle devices. With the development of more efficient heat-removal techniques (such as microchannel coolers), CW stacks have become available.

The packages for long-wavelength (>1000 nm) diode lasers used in telecommunications applications include special adaptations for coupling the laser output to single mode (approximately 9-µm core diameter) optical fiber with tolerances on the order of ±1 µm. These are in the form of fiber pigtails or single-mode connectors. Telecommunication laser packages can also include other elements such as thermoelectric coolers for temperature control and optical isolators to reduce the amount of light reflected from the fiber back into the laser. All laser packages include back-facet monitor photodiodes. Because of the expense of fiber coupling and other package features, telecommunications diode lasers typically have high ASPs. Prices range from less than $50 for the lowest performance 1310-nm Fabry-Perot devices in a connectorized coaxial package to $500 to $1000 for a high-performance distributed-feedback (DFB) laser in a cooled butterfly package with fiber pigtail. Diode lasers used in short-distance data-communications applications with multimode fiber have much lower prices. For example, 850-nm VCSELs packaged in several different configurations are priced at less than $5.

INSIDE THE MARKETS

null

null

null

null

null

null

null

Where the numbers come from

The Laser Focus World Annual Review and Forecast of the Laser Marketplace is based on a worldwide survey of laser producers and covers 27 types of lasers and 20 applications. Diode-laser market information is provided by Strategies Unlimited (Mountain View, CA). Industrial-laser market information is provided by Industrial Laser Solutions, and the Medical Laser Report newsletter provides the medical market analysis. This review is the only major survey of its kind in this industry whose results are made public.

For many, both inside and outside the industry, from private-sector investors to foreign and U.S. government bodies, this report is the only objective summary of major trends in our industry that is readily available. Part I published in January examined the overall market trends with more detail on nondiode lasers. Part II covers the diode-laser marketplace.

Readers interested in the detailed results of both surveys will find them in the January 1 and February 1 editions of the Optoelectronics Report newsletter, published by Laser Focus World. A more extensive review of the data, with supporting commentary from market analysts, was presented at the Lasers and Photonics Marketplace Seminar, held in conjunction with Photonics West (San Jose, CA) on January 23. For more information see www.marketplaceseminar.com.

Collecting the data

We conducted our research and analysis for the Review and Forecast during October and November 2005. We asked manufacturers to provide a confidential estimate of total worldwide market size (dollars and units) for 2005, based on year-to-date actual data, and a forecast for 2006. In addition to the information provided by the manufacturers, we also used data from other more narrowly focused market surveys, and we incorporated commentary provided by industry analysts who added market insight for specific segments.

Changes from last year

A comparison of last year’s 2005 estimates with this year’s restated 2005 numbers will show differences and occasional discontinuities in the numbers. In general, no attempt has been made to explain these differences in detail. We request “bottom-up” market estimates, and the respondents to our survey do vary from year to year-both in terms of the companies involved and the individuals-so variations in the results are inevitable. In addition, changes in market visibility occur as market shares change. Differences in the overall numbers for 2005 last year and for 2005 this year may also reflect whatever degree of optimism or pessimism was inherent in last year’s forecast (see www.laserfocusworld.com/articles/219847).-SGA