Market pressures dampen 2019 results

The total 2019 global manufacturing sector economy gave analysts a first-half high, riding on equipment suppliers’ residual order book strength from a fairly strong close in 2018, followed by a second-half turnaround dip caused, in part, by political economic manipulations in Europe (Brexit) and China (the tariff battle fallout with the U.S.). Throughout the year, Industrial Laser Solutions received a mixed bag of market economic reviews, which tended from flat to slow growth—a repeat of 2018. For example, the OIDA reported global machine tool revenues to decline 10% to 2017 levels. J. P. Morgan’s Global Manufacturing Purchasing Managers’ Index (PMI) dropped to its weakest (49.25 in July) since December 2017 and climbed back up to 49.8, sending signs of economic stabilization. Contradicting this, the Institute for Supply Management’s PMI dropped for the first time in three years to 49.1%, its lowest reading since 2016 as U.S. manufacturing business confidence declined and demand dried up with the effect of the U.S. presidential tariff squabble with China finally hitting home.

At the beginning of 2019, very few global economic reviews were optimistic. As the year progressed, unplanned negative news from China (according to the International Monetary Fund), now the world’s largest economy from a Purchasing Power Parity perspective, missed a government growth target for the first time in years, exacerbated by a stubborn U.S. president who was chaffing at China’s history of procrastination in making deals and who kept upping the tariff goals in a one-upmanship duel in which neither party won, leaving other global economies experiencing economic fallout that looked to be defined by the dreaded ‘R’ word.

Germany, a case in point with more than 50% of its exports headed to China, was seemingly exasperated at midyear as noted by a headline in The Diplomat (May 2019), a leading monthly current-affairs magazine for the Asia-Pacific region, that introduced a lengthy essay with “Are the Gloves Coming Off in China-Germany Economic Relations?” Forbes Magazine posited in Breaking News (October 28, 2019) that Germany was set to slide into recession due to a continuing decline in the manufacturing sector and low global auto sales. The German government managed to quench this problem temporarily.

Elsewhere in the world: UK (Brexit woes), Italy (machine tool orders down 19%), Hong Kong (citizen protests), and stressed economies in Turkey (long recession predicted), Mexico (NAFTA renegotiation), and Brazil (growth at lowest level ever) caused Forbes to state that the world’s economies were experiencing the slowest rate of expansion since the financial crisis of 2008. In the U.S., the July 2019 Fabrinomics newsletters asked, “Is Manufacturing Entering a Slump?” and in November, “Is a Global Recession Looming?” The answers—it depends on what happens around the globe. In an October 2019 posting, the IMF raised the specter of a Synchronized World Economy Slowdown at the slowest pace of growth since the 2008 recession.

However, as the year closed, Forbes’ Randy Brown, noting some economic problems (November 12, 2019), stated “…it’s hard to make a strong case for an imminent recession.” In this, he had concurrence from others: J. P. Morgan analyst Ong Sin Beng was quoted in SGSME News (November 21, 2019) saying “Outside of tech and biomedical output, the overall production index has been stabilizing, with a solid rise in precision engineering output,” and Bloomberg (November 8, 2019) affirmed that “The worst may be over for the world economy’s deepest slowdown in a decade.”

Stéphne Monier, CIO at Lombard Oder Private Bank, summed up the current situation in the November 11, 2019 issue of Investment Insights, a UBS newsletter, that “The puzzle of a recession-less slowdown may keep investors scratching their heads for a few more quarters. Still, the end of the economic cycle is not close.” Bloomberg Businessweek summed up the recession question in their November 25th issue: “Looser monetary policy in the U.S., Europe, and Japan has been instrumental in beating back expectations of a more pronounced economic slowdown.”

Industrial laser specifics

Now, the industrial laser material processing sector, at a nominal $20+ billon revenue level, is a full-fledged member of the global machine tool market, so one would expect it to follow the same trends. So, this mixed-bag economic news precipitated usage, by the largest industrial laser product manufacturers, of a new financial term ‘headwinds’—a more-palatable alternative to ‘problems,’ used when reporting to their shareholders. These companies, TRUMPF, IPG Photonics, Coherent, and Han’s Laser Technology, dominate the industrial laser products market with estimated combined 2019 sales approaching $9 billion. Other companies in Industrial Laser Solutions’ basket of public companies—for example, II-VI Incorporated and the Amada Group, are bidding for membership in the exclusive Industrial Laser Solutions Billion-Dollar Club.

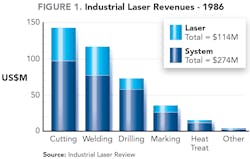

Thirty-three years ago, Industrial Laser Solutions (then known as Industrial Laser Review) published the first industrial laser market report (FIGURE 1) under the heading “A Snapshot of the Industry,” in which I wrote that “…as a controlled source of heating, laser processing is the only commercial processing technique that is completely decoupled from the material it processes. Among all of the unique aspects of laser processing, it is this decoupling aspect that sets the laser apart from its competition.” Three decades later, that remains a truism, as in that period, industrial laser revenues for material processing experienced a 26.8% compound annual growth rate (CAGR) vs. a 3.49% CAGR for global machine tool revenues. A possible reason could be that in 2019, laser revenues are growing through decoupled additive manufacturing, while machine tools remain focused on legacy subtractive processing. Maybe a stretch, but it serves to make a point.

For most of the three decades, Industrial Laser Solutions has taken the position that swings in laser revenue growth are primarily a function of trends in global manufacturing economies. Commencing in 2009, the beginning of the ‘great’ machine tool recession, laser revenues also took a hit as sales dropped 30%. However, 58% growth brought lasers back to prerecession levels within two years, as new products (high-power fiber lasers) and processes (more productive sheet metal cutting) developed during the recession were in place as the built-up buying demand took effect. Since the start of that recession, laser revenues have, through 2018, increased at a 13.7% CAGR.

A new factor is the fact that manufacturing demand from China arose as that country enjoyed government-sanctioned support for exporting products that were in part laser-processed—no longer low-added value products, but also high-value added products that were being outsourced from Western nations. Sales grew in China, first with imported equipment and in the more recent years domestically manufactured systems with imported high-power fiber lasers.

Industrial laser revenues

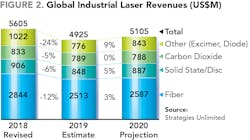

For the record, data for the following tables is based primarily on the most recent public companies’ quarterly reports up to November 30, 2019, including their guidance for the last quarter of the calendar year. Final 2019 revenue numbers will not be confirmed until early in 2020, as shown in the revised 2018 and estimated 2019 numbers in FIGURES 2 and 3.

In 2019, the industrial laser revenue picture changed with the economy in China challenged by a manufacturing slump, as well as results from quarrelling with the U.S. over tariff policy. The rest of the world’s manufacturing economies reacted to the fallout from this. In this atmosphere of global turmoil and uncertainty, 2019 revenues—following the trend set in machine tool revenues—experienced their first decline since the recession of 2009 (at that time, an Industrial Laser Solutions projected total laser revenue drop of -6% actually turned out to be a record 30%).

FIGURE 2 shows a 12.1% decline in 2019 revenues compared to the previous year. Most of this can be attributed to a slump in fiber and excimer laser revenues, the latter expected and the former a bit of a surprise: low-power fiber laser revenues, for the first time reacting to pricing competition, and at the high-power level, decreasing activity in the sheet metal cutting sector, where the high-power, high-selling-price fiber lasers had been experiencing rapid acceptance. It appears that competition at all power levels is driving down the average selling process of fiber lasers while the volume of units sold increases, a trend that also has implications for the near-term. Excimer laser sales into the handheld display sector were, in 2019, on the planned downside of a major investment in that one application.

It is important to note that fiber laser revenues (51%) represented about half the total industrial laser revenues in 2019, down slightly from the 2018 share (53%). The decline in fiber laser revenues is 49% of the total revenue decline in 2020—that’s the power of industrial fiber lasers today. The decline in high-power, high-selling-price fiber laser revenues for sheet metal cutting systems had the largest impact on total revenues. Actually, high-power laser unit sales were up, but as Chinese fiber laser companies entered that market sector, aggressively cutting selling prices, revenues were down. Fiber laser revenues for cutting are expected to bounce back 5% in 2020, boosting total fiber laser revenues for 2020 by a projected 3%. In 2020, fiber lasers should represent 51% of total laser revenues for this year.

Carbon-dioxide (CO2) lasers continued the pattern of revenue declines due to competitive domestic pricing decreases at the lower power level. The increased losses of CO2 lasers to fiber lasers for metal cutting at higher power levels has become a trend. The cost-effectiveness of new, very high-power fiber laser cutting at 10 to 12 kW is now more common, and with more 15 kW fiber power suppliers entering the material processing market in 2019, has reduced the last advantage CO2 had over the market.

Solid-state lasers, including the disk laser, for cutting/welding experienced the same declines in 2019 as the machine tool sector and are projected to return close to 2018 levels in 2020. Low-power lasers for micromachining, including the high-peak-power ultrashort-pulse (USP) lasers, had only a small decline in 2019 and may surpass 2018 revenues in 2020.

Excimer lasers for microprocessing took a big hit (-24%) in 2019, mainly due to an expected decline in applications for handheld device processing (slower sales of smartphones due to market saturation was also an unexpected contributor). A forecasted double-digit growth resulting from applications in new display technology (organic light-emitting diode, or OLED) in 2020 should correct this.

Regarding projected 2020 laser revenues, as this review was prepared, the entire global manufacturing sector was not issuing any encouraging growth signs and, regardless of an easing in the U.S./China tariff squabbles, the industrial laser market will likely respond accordingly with only a 3.7% growth. This plus other vagaries, and their fallout, of campaigns to elect a President in the U.S. will possibly be a factor in 2020 laser revenues. However, the major cause (fiber laser revenues) is a result of laser materials processing unit sales and average selling prices being down in China while the number of domestic suppliers continues to rise, flooding the market. Consequently, laser revenues may continue to decline as average selling prices continue to decline. And this dichotomy may spread globally as these many Chinese laser and system suppliers look to world markets, encouraged by their governments urging them to become global competitors.

Revenues by applications

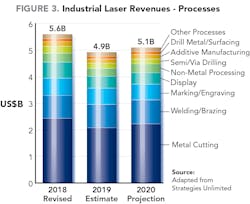

In FIGURE 3, we break out applications somewhat differently than in the past. Gone is the topic Fine Metal Processing and its components are now in other related topics, mainly in metal cutting. And we have separated Display as a category; changed PC Board to Via Drilling (with more input into that sector); blended Solar into the Other category, as this market is static; and combined both low- and high-power lasers used in Additive Manufacturing. Why, you may ask? It’s because, in the past, Industrial Laser Solutions’ market reports have been used without attribution in countless ‘for-profit’ industrial laser market reports offered on the web.

What is clear in FIGURE 3 is the impact that laser metal cutting has on total industrial laser revenues, 42% in 2019, and by association fiber laser revenues, as the majority of high-power/high-selling-price units are used for cutting. That application experienced a general decline in unit sales as the 2019 market reacted to reduced investment and a saturated market in China (the single largest laser cutting system market) retrenched under government pressure. The overall laser revenue reduction (12%), while in line with equivalent cutbacks in the machine tool market, would have been larger except for the rapid rise of high-power (6 kW) and very high-power (10–15 kW) laser cutting systems sales, which feature a higher unit selling price fiber laser.

The other dominant 2019 revenue number is Displays, where unit sales of smartphones with excimer laser-processed displays dropped precipitously due to market saturation and a major order for these excimer laser-based flat panel displays was in its planned phaseout.

Welding/Brazing unit sales were the only 2019 positive-growth application, prompted by increased demand from the auto industry’s use of high-strength steels for weight reduction, railroad car applications, and pipeline joining. Increased fiber laser output power up to 50 kW and higher and flexibility in the work environment make laser welding an attractive alternative.

Included with high-power fiber lasers in the welding category in FIGURE 3 are medium-power fiber, solid-state, disk, and direct-diode lasers. Suppliers of high-power lasers for welding acknowledge that this application, like all joining applications, is very much part-specific and consequently, the time from establishing feasibility to purchase to installation to acceptance can be quite long. That is why the successes in 2019 may have been started more than a year ago. Laser equipment suppliers expect the increase in 2020 very high-power revenues may offset, going forward, any moderation unit average selling prices in laser cutting revenues.

Laser revenues from Additive Manufacturing declined in 2019, consistent with the slowdown of system sales as the industry worked off excess capacity from previously installed equipment. The transition from a prototyping application to serial production slowed as potential users recognized the cost of post-laser part forming to finish the product. This situation is being investigated by myriad organizations and several cost-effective solutions show promise to expand the user base for direct-metal deposition serial laser processing.

A new category, Metal Drilling/Surfacing, which used to reside in Fine Metal Processing, will track the other precision laser applications. Centered in industries that for the most part experienced low to no growth in 2019, laser revenues declined. Surfacing, partially represented as laser texturing, is beginning to find expanded applications in the automotive industry. One example, USP laser processing of engine cylinder walls, improves performance, contributing to more effective corporate average fuel economy (CAFE) results.

High-power laser precision-drilling applications will benefit from the massive backlogs in turbine engines for delivery in the next five years, as new engines work into the airline fleets for more-efficient and longer-haul performance. On the high-peak/low-average-power side, a continuous growth in medical device drilling, with a concurrent demand for even smaller precision holes, is sparking some of the expanding market for USP lasers that utilizes their ‘cold processing’ effect to produce a non-heat-affected hole.

Non-metal processing is a catchall category for the laser applications such as slitting, trimming, perforating, and other operations performed in a wide variety of industries working with plastics, paper, and ceramic materials that are primarily served by CO2 lasers with output powers of less than 1 kW. This laser wavelength is efficiently absorbed by these materials. A modest number of applications responding to the ultraviolet (UV) laser output of some solid-state and fiber lasers are indicative of anticipated future growth in the medical device market, contributing to a projected strong double-digit rise in 2020 revenues.

The Laser Marking/Engraving sector has been, until 2019, a solid, if not spectacular, market delivering low single-digit growth for years. Non-contact laser processing of almost all materials has occurred as advances have been made in UV and other wavelengths in fiber and USP lasers. Materials previously unmarkable are now being marked with a new generation of cost-effective lasers.

Even so, it is not clear why the use of lasers to permanently mark materials on demand with a precise, readable, non-consumables process has not gained market share at the expense of other making technology. Take the marking of produce as an example—originally developed to mark eggs, the most delicate of food products, laser marking technology proved cost-effective for marking fresh produce at the packing site. Improvements in marking system scanning ability, productivity, and system reliability, plus reductions in unit selling price, have expanded the market. But as in other market sectors, marking now is heavily dominated by Chinese companies with dropping selling prices that have impacted the competitive landscape. Perhaps the spreading governmental product coding and identification requirements will cause a spurt in unit sales to offset another year of relatively flat revenues in this laser market.

The future

Looking ahead to 2020, expectations based on guidance statements by industry leaders suggest that the industrial laser market will return to a positive position in 2020—how positive is the question. FIGURE 4 plots Industrial Laser Solutions data for 2016-2020, with 2020 a projected value, and shows a modest 6% year/year gain that could get the industry back on a trend line after the 2019 downturn. We should not overlook the impact of very high growth in 2017. Now, here’s the rub—if it wasn’t for a spectacular 2018, when there was a booming market in China and the peak of excimer laser system deliveries for handheld display processing pushing revenues to a record high, the actual revenue curve would more closely match the trend line. All things considered, growth from 2016 to 2020 could be 53%.

However, as we preach yearly in this review, revenue has to match the prior year before growth occurs. And in the anticipated climate, this will not be a given. The Gardner Intelligence 2020 Capital Spending Survey (December 2019) projects the U.S. market for machine tools will fall by 5% compared to 2019. And the Fabricators & Manufacturers Association 2020 Capital Spending Forecast expects 2020 to be flat in the fabrication sector compared to 2019. While both surveys are for the U.S. market, they echo global trends—also recall that laser cutting, which is expected to grow 5% in 2020, is 40% of total laser revenues contributing to the projected overall 3.7%.

Remember that the U.S. is still the still the world’s largest economy (by GDP). The turmoil that a U.S. presidential election raises will, in a sharply divided nation, be of even greater magnitude and political savants seem to be shying away from speculating on whether the economy has the strength to withstand that and the fallout from a presidential impeachment.

Political turmoil is also a factor in the number-two economy China, but a forecast prepared by Dr. Bo Gu in the November/December 2019 issue reflects on the country’s ever-optimistic strong growth from its unit sales driven by battery welding, but mild growth in revenues due to severe selling price erosion as domestic suppliers ramp up competition to global imports.

It would appear that 2020 may also be a soft year in the manufacturing sector, with a consequent effect on industrial laser revenues. Therefore, Industrial Laser Solutions is anticipating a return to strong single-digit growth in the metal cutting and welding markets, enough to turn total red numbers to black. Not quite enough to return revenues to 2018 levels, but as stated earlier, that was a banner year, setting the bar at a challenging height. It looks like, except for CO2 and excimer lasers, 2020 will be a positive year in all laser and application sectors. It won’t be easy, but a host of new and expanding applications accomplished by new-model lasers begin a return to 2018 levels.

About the Author

David Belforte

Contributing Editor

David Belforte (1932-2023) was an internationally recognized authority on industrial laser materials processing and had been actively involved in this technology for more than 50 years. His consulting business, Belforte Associates, served clients interested in advanced manufacturing applications. David held degrees in Chemistry and Production Technology from Northeastern University (Boston, MA). As a researcher, he conducted basic studies in material synthesis for high-temperature applications and held increasingly important positions with companies involved with high-technology materials processing. He co-founded a company that introduced several firsts in advanced welding technology and equipment. David's career in lasers started with the commercialization of the first industrial solid-state laser and a compact CO2 laser for sheet-metal cutting. For several years, he led the development of very high power CO2 lasers for welding and surface treating applications. In addition to consulting, David was the Founder and Editor-in-Chief of Industrial Laser Solutions magazine (1986-2022) and contributed to other laser publications, including Laser Focus World. He retired from Laser Focus World in late June 2022.