Market’s messages mixed in 2005

Review and forecast, Part I: Nondiode lasers

Kathy Kincade and Stephen G. Anderson

NASHUA, NH - The good news is that, after more than 40 years, the laser industry is beginning to mature-or at least parts of it are. This is good news for several reasons, not least of which is the overall stability that comes with an increasingly diverse technology and applications base. Maturity also brings a more mainstream profile: photonics has entered the mass-market arena and is much less likely today to inspire the “gee whiz” reaction that it has garnered for so long. The bad news is that company sales and earnings grow more slowly in a mature industry, and growth opportunities are harder to come by. In addition, many of the markets served by laser manufacturers are also maturing, which means their investment in this industry may have peaked.

So calling the laser industry “mature” may actually be a bit, well, premature. Truth is, growth opportunities for lasers and optoelectronics-especially in applications in which they function as enabling technologies (see “‘New’ UV lasers resolve material and cost issues,” Laser Focus World, June 2005)-appear to be wide open. In addition, innovation is by no means on the decline. In fact, despite its decades-long history, the laser and optoelectronics industry is still considered “early stage” in many circles-which is very good news, according to Samuel Kahan, senior economist at the Federal Reserve Bank of Chicago.

“While this industry is at the moment relatively small, it is on the cutting edge of many things,” he said. “Think of automobiles and airplanes in their infancy.”

Equating lasers and optoelectronics with automobiles and airplanes? That’s heady stuff for an industry that has long depended on the research community for its bread and butter. But looking at recent application trends, Kahan may be right. As has been the case for the last few years, the biggest market driver continues to be the consumer. Computers, cell phones, cameras, fiber-to-the-home, vision correction, wrinkle removal, engraving, automobiles, home entertainment, laser light shows . . . whether directly or indirectly, it is sometimes hard to comprehend how pervasive lasers and optoelectronics have become in the consumer world.1 In fact, Michael Lebby, executive director of the Optoelectronics Industry Development Association (OIDA; Washington, D.C.) told attendees at the CS-MAX 2005 conference in Palm Springs last fall that some of the strongest potential growth markets for optoelectronics are in consumer electronics: displays for handheld products, image sensors for camera phones, and optical storage. Lebby also noted that the optoelectronics market offers many opportunities for startups to succeed by leveraging technologies originally developed for the communications market and applying them to emerging applications.

“There is no question that the issue is about serving the consumer,” said Fred Leonberger, an industry consultant and senior advisor at the MIT Center for Integrated Photonics Systems (Cambridge, MA). “In photonics, there are a lot of consumer applications, and the biggest ones are associated with displays. In fiberoptics, the drivers right now are associated with providing broadband access to the end user, which in turn is driving innovation at the photonics level. A lot of the progress made in the telecom area is helping to enable progress in other areas, such as high-power fiber lasers for marking and machining; in large part that has been driven by the progress in pump lasers. These advances are enabling other markets to adopt a good supply of products at a price-performance point that makes sense.”

Growing pains

While this all paints an optimistic picture going forward, there are some downsides. Or maybe call them growing pains. For example: the bigger and more global this industry becomes, and the more its products are deployed in consumer electronics, the more the laser business is affected by (and sometimes even dependent on) macroeconomic factors such as interest rates, foreign exchange rates, trade imbalances, oil prices, and consumer spending/saving (see “U.S. dollar continues to guide world economies,” p. 9). In addition, as the big public companies get bigger through mergers and acquisitions and gain the very spotlight they desire to further grow their businesses, the pressure to satisfy stockholders also increases.

“In the past decade, growth has occurred from expanding applications, not just selling more lasers into the same markets,” said John Ambroseo, president and CEO of Coherent (Santa Clara, CA). “But 2005 was disappointing from a growth perspective compared to 2004, especially for public companies. No one wants to be caught with overcapacities like they were in 1999 and 2000. Is this restricting growth? I think so.”

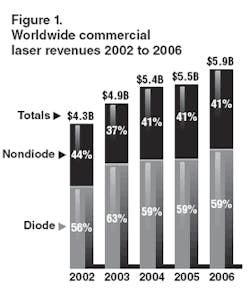

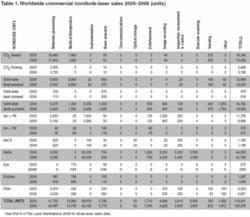

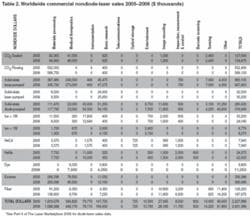

As if to underscore Ambroseo’s sentiments regarding 2005, the global-laser markets apparently remained basically flat last year, gaining only about 1% overall to reach almost $5.5 billion in 2005. And the performance was equally lackluster in both primary segments-nondiode and diode lasers (see Fig. 1). Among the many factors underpinning these numbers were a stalled semiconductor equipment market, “better than expected” industrial market performance, continuing growth in the defense/security sector, an uptick in optical communications, and a modest reduction in revenues for optical data storage (more information about diode-laser applications will be available in Part II of this report next month). The global market is expected to reach $5.9 billion in 2006-an 8% gain over 2005-which is where last year’s forecast pegged it for 2005.

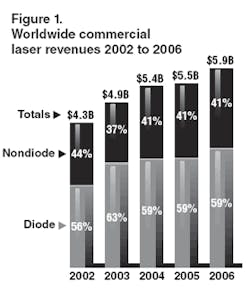

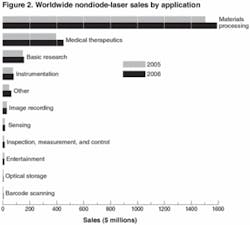

(Nondiode-laser sales data for 2005 and 2006 are charted in detail by application and by type in Figures 2 and 3, respectively. Nondiode-laser sales data by unit shipment and dollar revenues are shown in Tables 1 and 2, respectively, while Table 3 shows the average selling price. Corresponding charts and tables for diode lasers will appear in the February 1, 2006 Optoelectronics Report. For an explanation of our data-gathering and analysis methods, see “Where the numbers come from” on p. 11.)

Many photonics firms privately confirm moderate-to-high single-digit growth in sales during 2005. And results from some of the major public players are rather mixed, in line with a somewhat sluggish global market. Coherent, still the largest laser manufacturer worldwide, reported sales of $516 million in FY2005 (ending Oct. 1, 2005), up 4% from $495 million the previous year. Newport (Irvine, CA) reported a net sales gain of 10.5% in the first nine months of 2005 compared to the same period of 2004 (this number does not include Spectra-Physics revenues); while sales of the GSI Group (Billerica, MA) actually fell 22% to $194 million for the nine months ended Sept. 30, 2005, compared to the prior year period.

On the systems side, Rofin-Sinar (Hamburg, Germany) and Trumpf (Ditzingen, Germany) both had record years reflecting the performance of the industrial sector. Rofin reported revenues of $375 million for FY2005 (ended Sept. 30, 2005), a 16% increase over FY2004 (a 54% increase in North America), while Trumpf reported sales of $1.6 billion for FY2005, a 14% increase over FY2004.

The stalled semiconductor equipment market drove year-over-year revenues for lithography source manufacturer Cymer (San Diego, CA) down slightly (3%) to $281 million in the first nine months of 2005, compared to the first nine months of 2004. However, like many companies in this business, Cymer is bullish about emerging opportunities in consumer entertainment.

“We are particularly encouraged by the flash [memory] production opportunity, as it enables the expansion of the market for a growing generation of newer portable products capable of storing and quickly retrieving immense amounts of data, and the impact that is just beginning to have on the consumer video entertainment marketplace-the newly announced video iPod, games, camcorder phones, and a variety of other digital consumer products,” said Bob Akins, Cymer CEO. “More specific to our own industry, increasing fab utilization especially at foundries, growing demand for more capable flash memory, and tight capacity for critical and mid-critical layers all support our view that 2006 should be positive for equipment suppliers well-positioned to participate in these growth segments.”

Several of these companies have also been playing the consolidation game in the past year. Besides the Newport/Spectra-Physics merger of 2004, Coherent made two key acquisitions in 2005-TuiLaser and Iolon, while JDSU beefed up its commercial and telecom businesses in 2005 with the purchase of Lightwave Electronics, Acterna, and Agility. There were a dozen or more other mergers and acquisitions worldwide and even some IPOs, including Andor Technology (Belfast, Ireland) and SPI Lasers (Southampton, England).

This kind of deal-making is yet another indication of an industry moving forward. But the reviews remain mixed; some think consolidation is impeding expansion by making it increasingly difficult for startups to start up, let alone stay in business. But others think it is the only way for the industry to keep momentum going and for smaller companies to find and keep their footing.

“We have been seeing a lot of consolidation in lasers and optoelectronics, which is basically a good thing for a number of reasons,” said Steve Eglash of Worldview Technology Partners (Palo Alto, CA), a venture capital firm with a history of investing in photonics companies. “Sometimes the consolidation is two startups getting together-which means investors are more likely to invest-or a large company that absorbs a smaller company. Either way, it helps give smaller companies enough size and scale to survive and then to do R&D and new-product development. We are also seeing U.S. companies (such as Neophotonics) merge with Asian companies (such as Photon) to bring low-cost, high-volume manufacturing to the table, which enables them to enter some markets they might not have been able to otherwise.”

Eglash acknowledges that there is some commoditization occurring, most notably in optical components for communications. At the same time, however, both innovation and investment are on the rise in other markets.

“In terms of venture capital, we are seeing more money becoming available again, particularly in displays and imaging, lighting and illumination, and, photovoltaics,” he said. “There is a lot of renewed investor interest and increased investment going on, even in optical communications for applications such as fiber-to-the-premises, especially in Korea and Japan.”

The markets, and the numbers

Aside from the various forces at play in the markets, important shifts are also occurring in the technologies-most notably the continued displacement of nondiode lasers by diode lasers for many applications, from medical -therapy to the graphic arts. The rise of diode-pumped solid-state (DPSS) lasers continues, driven in part by the ongoing improvements in lifetime and reliability of the semiconductor pump lasers. And fiber lasers are rapidly grabbing a significant piece of the pie, especially for industrial applications. Hence sales of fiber lasers in 2005 were up 53% over 2004 and are projected to grow yet another 47% this year.

As we noted last year, the application groupings or market segments we use are intended to make manageable a complex and interlocking picture of laser technologies and applications. Because of the complexity, the following discussion presents a necessarily brief look at a few of the key segments from this year’s market review.

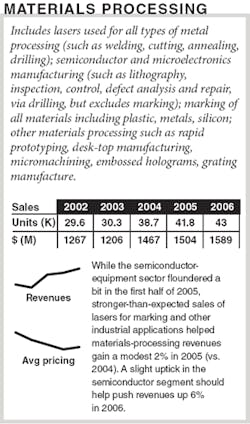

Materials processing

Weak performance in the semiconductor equipment business overshadowed better performance in other materials-processing segments to produce a net gain of only 3% in revenues for 2005 over 2004, though unit growth did fare a little better. Total materials-processing sales in 2005 were $1.5 billion and are projected to grow another 6% in 2006 to reach $1.6 billion (for more on the industrial materials processing market, see “Fiber-laser marking fuels growth in industrial market,” p. 13).

Despite its best efforts, the North American semiconductor equipment industry appears to be stalled as we near the end of 2005. After several months of improvement, the industry’s book-to-bill ratio apparently peaked in August when it reached 1.05, going above parity for the first time in a year-although at $1.1 billion, equipment orders (bookings) were still 26% below those of the previous year. Then in September orders fell back slightly to $1.09 billion and the book-to-bill ratio fell to 1.02. [The book-to-bill ratio is a comparison (based on a three-month rolling average) of orders received versus product billings for the period: a book-to-bill ratio of 1.0 (parity) means that $100 worth of orders was received for every $100 of product billed.]

Referring to the September numbers, Stanley Myers, president and CEO of the Semiconductor Equipment and Materials International (SEMI; San Jose, CA) trade group noted that the book-to-bill ratio was essentially unchanged from the prior three-month-average period. “Chipmakers are currently maintaining conservative spending patterns although we see indications of improving capacity utilization levels,” he said. Meanwhile another industry group, the Semiconductor Industry Association (SIA; San Jose, CA) in November forecast a tepid 6.8% (to $227.6 billion) growth in chip sales for 2005.

Not surprisingly, sales of lasers and related equipment for semiconductor and microelectronics processing reflect the uncertainty in the industry, and the Laser Focus World survey shows a 3% drop in net sales of lasers to this sector. Other examples include Cymer (San Diego, CA), which reported orders off about 6% compared to the prior year period in the quarter ended Sept. 30, 2005; equipment manufacturer KLA Tencor (San Jose, CA), whose orders for the same period were down 17% compared to the prior year; and Electro Scientific Industries (ESI; Portland, OR), which saw its orders fall 49% for the quarter ended Aug. 27, 2005, compared to the prior year period.

The complexity of the microelectronics arena leaves plenty of wiggle room for analysts trying to predict what 2006 and beyond will bring, and opinions do vary. Nonetheless, as far as chip sales are concerned two forecasts are actually in fairly good agreement: World Semiconductor Trade Statistics (WSTS; San Jose, CA) projects that after achieving 6.6% growth in 2005, the worldwide chip market is set to grow 8% in 2006 and 10.6% in 2007. And the SIA expects moderate growth of 7.9% in 2006 chip sales followed by 10.5% in 2007.

Notes SIA President George Scalise, “While information-technology products will continue to be the largest market sectors for semiconductors, consumer products will be the major growth-drivers in the years ahead.”

Increasing demand-albeit in single digits-for devices along with higher capacity utilization in fabs would appear to bode well for the equipment industry. Although some analysts are suggesting that capital expenditure will be moderated both by ongoing caution among device makers and by macro-economic factors, our survey suggests that revenues in the semiconductor and microelectronics segment will grow 9% in 2006. Some of this gain is driven by the increasing average sales price of lithography systems emitting in the deep UV.

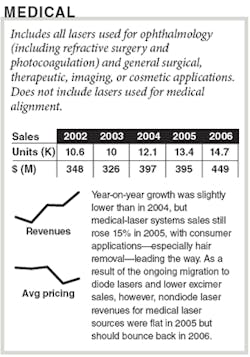

Medical therapy

As a result of the ongoing migration to diode lasers and lower excimer sales, nondiode laser revenues for medical laser sources were flat in 2005, at almost $395 million. Sales of nondiode lasers in 2006 are expected to rise 14% to $449 million (for more discussion of the medical-laser market, see “Medical market: Consumers still rule,” p. 14). Readers should note that the laser source revenues reported in the medical section of the Laser Focus World Market Review and Forecast are compiled by tracking medical-system end-user sales within this market sector. Revenue projections are based on medical-laser system sales to end users, and the laser is only one component of these system sales. The numbers in the Laser Focus World tables, however, are based on revenue estimates for the laser source itself.

null

Basic research

Over the years, sales of lasers and other optoelectronic components for fundamental research-much of it government funded-have been the “bread and butter” business of many photonics-component companies. In fact this market segment holds a place in the top three laser applications by revenues and has done so for years. While individual laser sales can be quite competitive, this marketplace has provided the industry with a mostly profitable foundation of advanced technologies that ultimately can find their way into the commercial marketplace. Although annual revenue growth rates for this sector are generally in the single digits, growth was flat for 2005 compared to 2004. Nonetheless, Newport/Spectra-Physics reported 8% growth in sales to this market for the first half of FY2005, and Coherent claims double-digit growth in the research and scientific market in 2004-2005, driven largely by emerging biomedical research. For 2006, according to our survey, the overall outlook is a more-typical 6% gain over 2005.

null

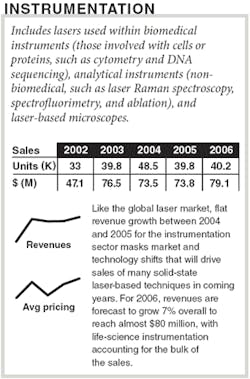

Instrumentation

Like the global laser market, flat revenue growth between 2004 and 2005 for the instrumentation sector masks market and technology shifts that will drive sales of the most favorable laser-based techniques in coming years. For 2006, revenues are forecast to grow 7% overall to reach $80 million, with life-science instrumentation accounting for the bulk of the sales.

Since the completion of the Human Genome Project in 2003, there has been an accelerating shift from the study of DNA (genomics) to the study of proteins (proteomics), notes Michael Tice, vice president of Strategic Directions International (Los Angeles, CA) and contributing editor of Instrument Business Outlook, published by Strategic Directions International. Although both disciplines are very active, proteomics is in clear ascendance. Proteomics research involves the use of a wide array of tools, many of which utilize lasers for fluorescence stimulation and/or imaging. For some of these applications, blue 488-nm lasers are de rigueur, and the market has grown more competitive as laser suppliers continue to introduce novel solid-state laser solutions to a problem that was once solely the province of ion laser technology. Another goal of proteomics research, protein microarrays with laser-based scanning systems, is continuing to develop. Many believe that, like the DNA microarray market in the 1990’s, protein microarrays will experience meteoric growth once the technology becomes practical. When this happens, it will provide an exciting new market for lasers in the laboratory.

A technique that is better established in the marketplace is matrix-assisted laser desorption ionization (MALDI) mass spectrometry, which is currently undergoing a small burst of interest that may well flower into an important new market. Although MALDI mass spectrometry can be used in non-life-science applications such as polymer analysis, much of its current growth stems from biological applications. One new development is the use of MALDI mass spectrometry for chemical imaging of a surface. Although applications are still developing, MALDI imaging could become a new standard tool in pharmaceutical drug discovery, replacing or augmenting the current laborious (and mostly non-laser-based) techniques. Unfortunately, the lasers used in conventional MALDI (nitrogen and Nd:YAG) are not ideal for imaging applications, but this has provided a spur to innovation. In February last year Bruker Biosciences (Billerica, MA) announced a proprietary solid-state laser that offers a number of features better suited for MALDI imaging and other MALDI mass-spectrometry applications.

Raman spectroscopy remains an active and growing market in both life-science and industrial laboratories. Most lasers in Raman spectrometers emit in the IR, but some applications use visible and UV devices. Instrument manufacturers have used various methods to overcome the limitations of Raman spectroscopy, and these improvements are helping to fuel the current growth of the technique. One such development is the exploitation of surface-enhanced Raman spectroscopy (SERS), an effect that increases the Raman signal by up to a millionfold when a sample is in contact with specially prepared surfaces. The increased sensitivity of SERS may affect the laser market in two ways. Not only will this advance help increase the overall Raman market by enabling new applications, but there is also the possibility that the increased sensitivity could permit the use of much less powerful lasers in Raman spectrometers.

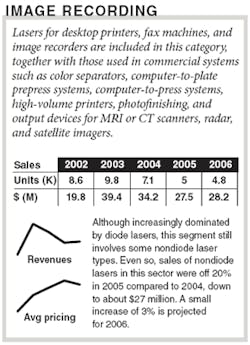

Image recording

The graphics arts market is going gangbusters as far as lasers are concerned and aggressively continuing its transition to diode lasers. Coherent, for example, reported 353% increase in orders in the graphic arts and display market in the fourth quarter of FY2005 compared to the same quarter of FY2004-due in large part to an annual purchase of a recently released product platform: a multi-element diode laser that facilitates rapid exposure of high-volume printing plates.

And therein lies the rub: the bulk of the applications (and thus, sales) for lasers in the graphic arts involve diode lasers-red diode lasers for thermal platesetters and violet diodes for computer-to-plate (CTP) applications. It’s no surprise then to find that sales of nondiode lasers in this sector were off 20% in 2005 from 2004 to about $27 million. A small increase of 3% is projected for 2006.

Diode-pumped solid-state green lasers are still used for imaging photopolymer plates and also in some niche applications such as holographic printing and film writing, but overall “no one is buying Nd:YAG lasers for prepress applications,” according to Dan Gelbart, CTO at CREO (Burnaby, BC), now part of Kodak. Hence, sales of DPSS lasers in this segment are essentially flat. And after a 32% drop in 2005 over 2004, fiber lasers-which displace DPSS lasers in some flexo CTP applications-are showing 10% sales growth for both 2006. On a much smaller scale, CO2 lasers (200 to 300 W) are still used for engraving flexo plates and for direct imaging on the copper cylinders used in gravure printing. In addition, UV lasers are finding application in printed-circuit-board imaging.

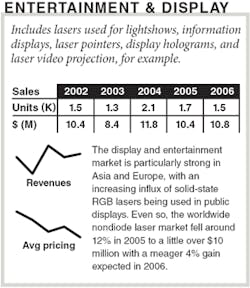

Entertainment & display

Diode-pumped solid-state lasers continue to supplant ion lasers for large-scale displays, and are poised to do the same in home-entertainment systems such as rear-projection TVs (see “Laser-based projectors near commercial reality,” Laser Focus World, December 2005). However, the general consensus is that affordable laser-based rear-projection TVs are still two to three years away from commercial reality. In the mean time, those companies building solid-state lasers for this application are under the gun to make them more affordable and easier to manufacture in large volumes.

As has been the case for the past few years, the traditional entertainment and display market has experienced much consolidation, leaving a handful of systems companies, primarily in Europe and Asia, providing the bulk of the equipment. At the same time, the number of companies offering solid-state RGB lasers for this market continues to grow, creating an increasingly competitive environment. In addition, regulations governing the use of laser systems in public continue to curtail their use in the United States; the International Laser Display Association (ILDA; Portland, OR) is currently lobbying the U.S. government to ease some of these regulations and perhaps stimulate the U.S. market. The worldwide nondiode laser market fell around 12% in 2005 to a little over $10 million with a meager 4% gain expected in 2006.

“We are still seeing new solid-state products coming out from Europe and Asia for entertainment,” said David Lytle, executive director of ILDA. “And they are doing a lot of engineering for products specifically geared to the entertainment market. The real hot spot is in Asia, where there is a lot of manufacturing and purchasing. But we are hoping that if we can get the variance procedure (in the United States) relaxed and streamlined, it would really help this market in the United States.”

Military/aerospace

Anecdotal reports suggest that the military/defense/security market is strong and growing, from laser weapons to missile detection and biosensing systems. The U.S. military in particular is investing in many laser-based projects for defensive and offensive purposes: the Airborne Laser, the Joint High Power Solid-State Laser, High Energy Liquid Laser Area Defense Systems, Robot-Enhanced Detection Outpost with Lasers, Personnel Halting and Stimulation Response, Paveway II Dual Mode Laser-Guided Bomb, Aircraft Countermeasures, Architecture for Diode High Energy Laser Systems . . . the list goes on and on, and so, apparently, does the depth of the Department of Defense’s pocketbook.2 And that doesn’t even cover the number of projects involving imaging, displays, and sensing systems.

As has historically been the case, however, getting an accurate read on what the military is spending on -lasers and related components is difficult at best. Some projects are announced, such as the $50 million contract Lockheed Martin (Archbald, PA) received last September to deliver laser-guided bomb kits to the U.S. Air Force in 2006-a contract that represents more than half of the U.S. Air Force’s requirements for the current fiscal year-and the $124.5 million contract awarded by the U.S. Navy to Northrop Grumman (Melbourne, FL) to built production units of the Airborne Laser Mine Detection System, a lidar-based large-area-coverage system designed to detect, classify, and localize floating and near-surface moored sea mines. But overall, our survey numbers for military and aerospace reflect the lack of transparency in this sector and are certainly incomplete; even so, an upward trend is evident-overall unit sales for 2005 were up 35% from 2004 to reach $63 million. In 2006 another 31% gain is anticipated.

Other markets

Market segments not specifically discussed above but that are listed in our data include inspection and measurement, optical communications, barcode scanning, and data storage. Most of these are either segments that have moved solidly into the diode-laser camp or they involve a mixture of many smaller applications that do not lend themselves to a detailed discussion in the space available. Diode-laser markets will be addressed in detail next month.

REFERENCES

- “Best Inventions of 2005: Fruit tattoos,” Time, Nov. 21, 2005.

- J. McHale, “Chasing the goal of an efficient battlefield laser,” Military & Aerospace Electronics (Oct. 1, 2005).

The Laser Focus World 2006 annual review and forecast of the laser markets is conducted in conjunction with Strategies Unlimited (Mountain View, CA; a PennWell company). Part I of the review reports on overall market and focuses on nondiode laser applications. Part II, written by Robert Steele of Strategies Unlimited, covers the diode-laser marketplace and will be published in the Feb. 1 issue of Optoelectronics Report.-Ed.