Photonics M&A activity is off to a slow start in Q1 2024

The Photonics M&A Quarterly, a new laserfocusworld.com series, analyzes the merger and acquisition activity within the photonics technology marketplace for scientists, engineers, entrepreneurs, and business leaders.

Though the overall merger and acquisition (M&A) market during the first quarter of 2024 saw positive growth globally, M&A activity with targets employing photonics technologies is off to a slow start.

The total value and volume of transactions with photonics targets were $39 billion and 125, respectively. Excluding Synopsys’s $33 billion acquisition of Ansys, a supplier of engineering simulation software and services, the total value is $5 billion, tracking less than the 2023 record low of $33 billion. Meanwhile, the volume in the first quarter of 2024 is tracking in line with 2023’s record low.

Transaction details

What types of transactions are getting done? Strategic buyers are acquiring lower middle market companies with core photonics technology that address their challenges of growth, scarce R&D resources, and shortages of skilled workers and technical talent. M&A remains a key means for strategic buyers to enhance capabilities and open new markets. Strategic buyers account for 90% of the transactions.

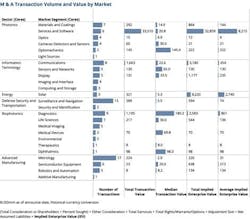

Consistent with 2023, metrology (advanced manufacturing) and surveillance and navigation (defense, security, and transportation) saw the most activity this quarter. The high activity level and relatively low total value in these markets are evidence of a continued high concentration of capabilities deals.

Inconsistent with previous years, Biophotonics did not see the most activity and highest total value of all photonics-enabled sectors this quarter. This result is consistent with today’s medical devices and diagnostics market conditions.

Leading the pack in Metrology are:

- Private equity firm Middleground Management’s acquisition of The L.S. Starrett Company, a provider of traditional optical metrology tools

- Bruker’s acquisition of Nion Company, a manufacturer of scanning transmission electron microscopes

- inTEST Italy’s, acquisition of Alfamation, a provider of test systems for micro-optics and optoelectronics manufacturing

The top three deals in Defense Security and Transportation are:

- Lockheed Martin’s acquisition of Terran Orbital Corporation, a manufacturer of satellites for aerospace and US defense

- Honeywell International’s acquisition of Civitanavi Systems, a vertically integrated supplier of ITAR-free fiber-optic gyroscopes.

Geographically, in line with 2023, the first quarter saw target M&A activity in the Asia and Pacific region outpacing the United States/Canada and Europe: 34% and 14% of buyer headquarters are in the United States and China, respectively.

Valuation highlights

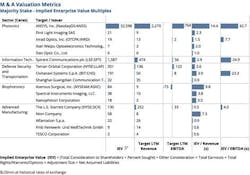

In the overall M&A market, strategic deals traded at the highest multiples in history across the board in 2021, with the decreasing valuations in 2023 continuing into the first quarter of 2024. Many generalist analysts predict valuations to stabilize here with the new normal of higher interest rates, shortage of skilled labor, and geopolitical instability. Based on researched transactions for targets with photonics technology, 2021 was also a banner year. However, in contrast with the M&A market as a whole, strategic deals continue to trade high for photonics targets.

Very few transactions report target financials. Among the researched transactions for a majority stake, 17 buyers report Implied Enterprise Value (IEV) multiples.

Spirent Communications, a provider of automated test solutions for communications, satellite, and autonomous vehicle networks, passed on a $1.3B offer (IEV/EBITDA, 21.6x) from Viavi Solutions to pursue a $1.5 billion offer (IEV/EBITDA, 24.9x) from Keysight Technologies.

The strategic buyers

In line with history, the most active buyer is Bruker, which acquired four biophotonics companies:

- Nanophoton, a provider of laser microscopes (3.50x $5 million revenue)

- Spectral Instruments Imaging, a provider of preclinical optical systems for bioluminescent, fluorescent, and x-ray imaging (3.75x $10 million revenue)

- Tornado Medical Systems, a provider of optical spectrometers for Raman spectroscopy and spectral-domain optical coherence tomography

- ELITech Group, a manufacturer of in vitro diagnostic equipment and reagents for $943 million.

Bruker also acquired Nion Company, a supplier of electron-optical instruments (7.25x $8 million revenue). In addition, ABB acquired Real Tech, a provider of real-time water quality monitoring solutions, and the remaining majority share of Sevensense Robotics, a supplier of robot-enabling software and multi-camera sensors for autonomously navigating dynamic spaces shared with humans.

Meanwhile, pure-play Photonics market leaders were not acquisitive in 2023 and, so far, in 2024. Except for Ansys’s transaction, total and average value and the number of transactions are down substantially from 2021 highs. Still, there continues to be a high concentration of strategic acquisitions of capabilities, product lines, and technical talent. The first quarter of 2024 uniquely sees a high concentration of financial and strategic buyers owned by private equity firms. Luxium Solutions, owned by Edgewater Capital Management, LLC, acquired PLX, a manufacturer of retroflectors, and Inrad Optics, an optical components supplier (announced Q2 2024, not included in analysis).

The 2024 photonics M&A outlook

Inflation, higher interest rates, geopolitical instability in the Middle East, Europe, and China, and shortages of skilled labor and technical talent will continue into 2024. While financial indicators improve, this could be the best time for well-capitalized strategic and growth-oriented financial buyers to do deals.

The lower concentration of mega-mergers and deals substantially scaling existing core businesses and the continued higher concentration of lower middle market transactions and corporate carve-outs are expected to continue.

With private equity leveraged buyouts scarce in the overall M&A market due to high interest rates and uncertainty around valuations with market volatility, financial buyers of companies with core photonics technology apply their playbooks from other industries. These tactics include cutting expenses to improve profitability, divesting non-core business units and product lines to beef up balance sheets, and acquiring smaller add-ons for existing portfolio companies.

Proactive buyers may continue to take some risk in the near term and engage with sellers’ new mindsets around valuation. Less aggressive buyers may wait on the sidelines until clarity on where inflation, interest rates, and unemployment will land.

CERES sources transaction data from public sources. CERES analysis and data are subject to errors and omissions. The accuracy of information is the responsibility of the user.

About the Author

Linda Smith

President, Ceres Technology Advisors

Linda Smith is a recognized leader in M&A advisory. Spanning the spectrum of photonics-enabled markets, she advised on acquisitions and financings valued at more than $1.5 billion. She founded CERES in 2005 to serve photonics companies underserved by generalist investment bankers. Prior, she held product management, engineering, and sales positions at public and private equity-financed photonics companies.