Record global M&As boost photonics

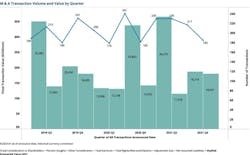

2021 marks the highest total transaction value in history for mergers and acquisitions (M&A). Year to date, global aggregate M&A transaction value is up 40% over 2019. However, the total transaction value for targets employing photonics technologies is still shy of its 2019 high of $87 billion.

This difference may be due to an inherently high concentration of strategic deals. According to Bain & Company, “while strategic M&A is on track to reach its highest value in six years, it also accounted for the lowest portion of deal value yet; sponsor, SPAC [special-purpose acquisition companies], and VC deals grew two to five times faster.” Since 2018, approximately 80% of acquisitions of photonics-enabled targets involve strategic buyers.

Strategic buyers address the challenges of slower growth, an abundance of investment capital, advances in digital and mobile technologies, and government intervention with M&A. They acquire companies to open new markets, enhance capabilities, and implement new business models. We also see more strategic buyers executing vertical integration plays, bringing critical capabilities in-house. In 2021, however, M&A appears to have shifted back from capability deals to scale deals as companies seek to strengthen their core business (see Fig. 1).

While the overwhelming majority of pure-play photonics market leaders executed one single transaction, the deals were large and scaled existing businesses. For example, Teledyne Technologies (NYSE:TDY) acquired FLIR Systems (NasdaqGS:FLIR), a provider of thermal and visible light imaging systems for $7.5 billion on $1.9 billion revenue. Coherent (NasdaqGS:COHR), a laser supplier, received proposal from II-VI Incorporated (NasdaqGS:IIVI), a supplier of engineered materials and optoelectronic components, for total consideration of $7.0 billion on $1.9 billion in revenue. Viavi Solutions (NasdaqGS:VIAV), a provider of optical networking test equipment, acquired EXFO, a provider of optical networking test equipment, for $478 million on $284 million revenue. Lumentum Holdings (NasdaqGS:LITE), a provider of photonic products for communications, acquired NeoPhotonics (NYSE:NPTN), a provider of optical transceivers/receivers for hyperscale datacenters, for $979 million on $278 million revenue. And Jenoptik (XTRA:JEN) acquired BG Medical Applications/SwissOptic AG/SwissOptic (Wuhan), an OEM supplier of medical optics for $349 million.

Across all photonics markets served, no single buyer was very acquisitive in 2021. The most active buyer was Thermo Fisher Scientific (NYSE:TMO), which acquired four life sciences instrumentation companies and a PCR-based rapid point-of-care testing platform for detecting infectious diseases; and Amphenol (NYSE:APH), which acquired four communications connectivity components suppliers. Halo Technology Group also acquired communications connectivity components suppliers. In addition, BICO Group (OM:BICO) acquired life science instrumentation companies; Desktop Metal (NYSE:DM) acquired materials, machines, and processes for additive manufacturing; Salvo Technologies acquired thin film coating, optical component, and spectroscopy instrumentation capabilities; Snap (NYSE:SNAP) acquired augmented reality (AR) technology; and The Carlyle Group (NasdaqGS:CG) acquired providers and a contract manufacturer of life science tools and analytical instrumentation.

Consistent with previous years, the biophotonics sector saw the most activity and highest total value of all photonics-enabled sectors. The largest transactions were the Quoin Pharmaceuticals' (NasdaqCM:QNRX) acquisition of Cellect Biotechnology, a developer of a 3D time-sequenced microscopy platform that functionally selects stem cells to enhance the safety of regenerative medicine ($9.4 billion); Quidel's (NasdaqGS:QDEL) acquisition of Ortho Clinical Diagnostics Holdings (NasdaqGS:OCDX), an in vitro diagnostics market leader ($8.4 billion); the DiaSorin (BIT:DIA) acquisition of Luminex, a supplier of biological testing technologies that integrate microfluidics, optics, and digital signal processing ($2.1 billion); the GE Healthcare acquisition of BK Medical Holding Company, an intraoperative ultrasound imaging equipment provider ($1.5 billion); and the Boston Scientific (NYSE:BSX) acquisition of Lumenis’s urology and otolaryngology laser and fiber-optic systems manufacturing business ($1.1 billion).

Also in the biophotonics sector, Rockley Photonics Holdings (NYSE:RKLY), a provider of a mobile health monitoring platform based on silicon photonics, and Quantum-Si (NasdaqGM:QSI), a developer of a protein and genomics sequencing platform, rode the wave of SPAC mergers. It is an attractive go-to-market strategy given the ability to quickly go to market at high valuations with lower levels of scrutiny relative to traditional IPOs.

Rockley and Quantum-Si started publicly trading following the completion of business combinations with SC Health and HighCape Capital Acquisition. As of December 14, 2021, their market capitalizations of $0.7 billion and $0.8 billion are less than half of their summer peaks of $2.0 billion and $1.9 billion, respectively. Quantum-Si puts its publicly raised capital to work to secure its supply chain and support scaling commercialization efforts by acquiring Majelac Technologies, a supplier of semiconductor and optoelectronic assembly services.

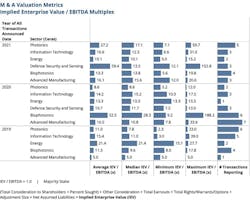

In 2021, strategic deals traded at the highest multiples in history across the board. With the exception of the biophotonics sector, which historically sees very high multiples, this was uniquely true of strategic deals involving photonics technology targets.

Few transactions reported financials because regulations do not require them when a transaction does not have material near-term impact on financial statements. Of the researched transactions for majority stake, 20 buyers reported implied enterprise value (IEV)/EBITDA. Values are in $US millions at historical rates of exchange. In 2021, valuations of pure-play photonics companies no longer lag valuations of companies in the vertical markets they serve (see Fig. 2).

Geographically, the most significant trend prior to 2018 was an acceleration of cross-regional acquisitions. That trend loses its momentum and falls off a cliff in 2019, with increased government intervention on cross-border deals and trade tensions between the U.S. and China. In 2021, this downward trend was accelerated by supply chain concerns exposed by the COVID-19 crisis and government scrutiny expanding beyond sensitive defense and technology industries.

In conclusion, photonics technology deals did not keep pace with the M&A market as a whole. Strategic buyers had the advantage over financial sponsors such as private equity, in that they could create proprietary deal flow. However, most M&A deals today are auction processes with stiff competition from financial sponsors, who have more deal-making capability and capacity than strategic buyers—as well as $2.8 trillion of “dry powder.” If financial sponsors are more attracted to photonics deals in the future, the photonics M&A deal pace will likely increase in line with the market as a whole. To compete, successful strategic buyers will have to expand their M&A capabilities and/or instead consider partnerships such as joint ventures or corporate venture capital to expand capabilities and address challenges in talent retention and supply chain.

Ceres Technology Advisors sources transaction data from public sources. Ceres analysis and data are subject to errors and omissions. Accuracy of information is responsibility of user.

* Definitive agreement, March 25, 2021; LTM financial information as of February 10, 2021

About the Author

Linda Smith

President, Ceres Technology Advisors

Linda Smith is a recognized leader in M&A advisory. Spanning the spectrum of photonics-enabled markets, she advised on acquisitions and financings valued at more than $1.5 billion. She founded CERES in 2005 to serve photonics companies underserved by generalist investment bankers. Prior, she held product management, engineering, and sales positions at public and private equity-financed photonics companies.